[DEBRIEFING] A critical test for Korea’s social safety net

![People line up in front of a drug store in Jongno District, central Seoul, to receive publicly-distributed masks on March 21. The national health insurance database was used in limiting the masks to two per person every week as there was a surge in demand after the number of coronavirus cases shot up after many Shincheonji members especially in Daegu contracted the virus, forcing the city to lock down. [YONHAP]](https://koreajoongangdaily.joins.com/data/photo/2020/06/22/f4478e5a-cbd1-410a-a373-d2379f1b134b.jpg)

People line up in front of a drug store in Jongno District, central Seoul, to receive publicly-distributed masks on March 21. The national health insurance database was used in limiting the masks to two per person every week as there was a surge in demand after the number of coronavirus cases shot up after many Shincheonji members especially in Daegu contracted the virus, forcing the city to lock down. [YONHAP]

In Debriefings, the Korea JoongAng Daily discusses a topical issue in-depth in a Q&A format. In this Debriefing, we examine the history of the four social securities and look at the finances underlying each of them.

With the economic fallout of the coronavirus continuing to reverberate through Korea’s economy, companies are being pushed to the brink of bankruptcy as thousands of workers are thrown out of work.

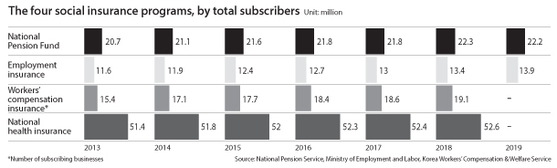

But despite the grim global economic outlook, Korea is in some ways well positioned to weather the storm, with a relatively robust social safety net, referred to as the “four social insurances” — the National Pension Service, the Employment Insurance System, the Korea Workers’ Compensation Insurance and the National Health Insurance Service.

The health insurance program, which provides health coverage to Korean citizens and long-term residents, has played a critical role during the outbreak, fully covering the costs of medical treatment for people that have contracted the virus.

Meanwhile, employment insurance has been increasingly supporting those that have lost their jobs due to the pandemic outbreak. And the National Pension Service, which provides many retired Koreans with living expenses, faces challenges as the country’s largest institutional investor during a period of extreme financial uncertainty.

In this debriefing, we examine the history the four social securities, as well as the finances underlying each of them.

When, and why, did the four social insurances begin?

Korea’s modern-day social safety net began with the creation of the workers’ compensation insurance, enacted on Jan. 1, 1964.

Shortly thereafter, the national health insurance program was implemented in 1964, although only on a limited scale. The program has existed in its current form since 1977.

The national pension fund was created in 1988, and employment insurance was adopted last, in 1995.

In its current form, the aim of the four-program safety net is to provide the public with a basic level of income, insulating them from external crises like the ongoing pandemic, as well as individual circumstances from illnesses to lost jobs or the unexpected death of a family’s breadwinner.

Individuals and businesses are required by law to pay into the four programs, although employees that work less than 15 hours per week are exempt. Businesses, including self-employed workers, must foot the full bill for workers’ compensation, while the other three programs are split between the worker and their employer.

Let’s focus on the National Health Insurance Service: How does it work, and who pays for it?

The total rate applied is 6.67 percent, 3.335 percent for employer and 3.335 percent for employee, on their monthly paycheck. The government also contributes to the solvency of the fund and by law is allowed to provide up to 20 percent of the projected reserve.

For regional subscribers, the insurance payment is calculated based on income, including pension payments, financial investment profits and the value of their property.

The minimum payment is 13,980 won ($11.5), while the maximum is 3.3 million won.

The national health insurance program debuted in 1964 under President Park Chung Hee after medical insurance legislation was first created.

At the time, national health insurance was created to compete with North Korea’s free medical services, although the program was not initially mandatory for South Korean residents.

But by the late 1970s, Korea’s labor movement was growing, fueled by anger against conglomerates’ low wages while workers were stuck with expensive medical bills. In 1977, the insurance payment was split between the employers and employees, a system that continues to this day. However, the program was still only mandatory for conglomerates with more than 500 employees.

Gradually, it expanded to include government employees, soldiers and teachers by 1979.

In July 1988, during the administration of President Roh Tae-woo, the program became mandatory for all businesses with employees of five or more. Over the next two years, community health insurance, also known as “regional subscriptions,” expanded to farmers, fishermen and self-employed workers.

While the program expanding to cover all Koreans was during the Roh administration, the idea was first raised by President Chung Doo Hwan’s administration, as he faced mounting public anger toward his military regime. Chung promised to expand national health insurance to every Korean, as many lower-paid workers at the time still had no access to medical insurance coverage. During that time, Chung had also promised of introducing the minimum wage system.

In 1988, Korea became the second country in Asia after Japan to provide nationwide health insurance coverage.

But despite the universal coverage, the program was still unwieldy, with insurance plans under the national health insurance service being run individually by 366 unions as of 2000. That year, the Kim Dae-jung administration finally unified the plans into its current form.

The latest major change to the insurance program took place last year, when President Moon Jae-in’s government enacted a change to the insurance program in July that requires all foreigners staying in the country for more than three months to also pay in to the program. The change came in response to foreigners frequently visiting Korea for medical reasons and getting national insurance coverage without paying into the system.

Foreigners employed by Korean companies were already treated the same as citizens under the national insurance system, but the new rule requires other longer-term foreigners to pay into the system as regional subscribers.

GRAPH

Is Korea’s employment insurance system set up to handle the number of new jobless claims?

Unemployment insurance has played a critical role in helping those who are out of work, providing unemployment checks, helping workers find new jobs through state-funded vocational training and covering the payments for employees taking pregnancy leave or raising children.

Employers and employees each cover half of the combined 1.6 percent rate applied to the employees’ paychecks to fund the program. This was raised from 1.3 percent last October.

However, the fund is also supported by tax dollars when it falls short of demand. Last year, the government increased its budget for the employment insurance fund from 7.18 trillion won to 8.34 trillion won, an increase of 16.2 percent.

The insurance program however, does not apply to new employees aged 65 or older.

Government employees, private school teachers, workers in the culture and arts industries, employees of religious organizations and those who work less than 60 hours per month, or 15 hours each week, are also excluded from the requirement.

However, pressure has been mounting on the program recently, as the number of people applying for unemployment benefits has surged amid the coronavirus outbreak.

After hitting an all-time record of 10.1 trillion won in 2017, the fund has shrank every year since, falling to 9.35 trillion won in 2018. Last year, the program’s total funding amounted to 7.83 trillion won.

The fund’s investments yielded a 7.06 percent net profit yield last year, a turnaround from its 2.22 percent loss in 2018 and higher than the 6.4 percent profit in 2017. Despite the financial upswing, however, the program still ran an overall deficit of 2.2 trillion won in 2019, nearly triple the deficit from the year before.

The growing deficit has been frequently blamed on the Moon administration’s minimum wage hike in 2017, along with changes to unemployment benefits in recent years.

During the past four years, the minimum wage has risen 42 percent, from 6,030 won per hour to 8,590 won this year. Starting in October 2019, unemployment paychecks have risen from 50 percent of the employee’s average wage to 60 percent, while the government has also expanded the amount of time recipients can qualify for unemployment.

The burden is expected to increase further, with last month already recording a record-high number of people receiving unemployment benefits.

As of March, the number of people that received unemployment benefits had reached 608,000, up 20 percent from a year ago, according to the Ministry of Employment and Labor’s latest report. Total benefits paid out also hit a record high of 898.2 billion won, up 40 percent on year.

Facing the prospect of even deeper cuts to the nation’s employment, the government created a 40 trillion won fund to inject liquidity into major industries, from automakers to airlines and shipbuilders, under the condition that they not further lay off workers.

How does work-related injury insurance work?

The workers’ compensation insurance covers medical and related treatment if an employee is injured or killed while working.

Unlike employment insurance, the program is mandatory for all employees, including foreigners, and is paid entirely by the employer.

The rate at which employers contribute varies according to the type of business, based on the likelihood of serious injuries to workers.

Currently, the average rate is 1.56 percent, a 0.09 percentage point decline from 1.65 percent in 2019. Payment rates range from 0.6 to 18.5 percent, the latter being applied to the mining and quarrying industry.

Employees receive 70 percent of their average daily earnings if they are kept off the job for a work-related medical reason, whether due to an injury or after contracting a disease.

If an injury or illness sustained at work fails to improve after two years, the employee continues to receive the 70 percent payments, with additional payments based on the level of injury or illness.

If the injury results in permanent physical or mental disabilities, the program pays accordingly to the severity of the disability. The payment either comes in a single payment, in case of less extensive disabilities, or in the form of a pension in more serious cases.

If the worker continues to need medical assistance after treatment, they receive between 27,450 won and 41,170 won per day for caregiver expenses.

For workers killed on the job, their families receive 52 to 67 percent of the employee’s average pay every month. The program also provides 11 million to 15.5 million won in funeral expenses.

Given the current financial climate, what’s the state of the National Pension Service?

Created to protect the livelihoods of workers after retirement, the National Pension System operates the largest pot of money out of the four insurance programs and is Korea’s largest institutional investor.

As with the health insurance, payments into the fund are split evenly between employers and employees, with each chipping in 4.5 percent of the employee’s paycheck. Business owners and self-employed workers have to pay the full 9 percent.

Foreign workers are also required to pay into the pension fund, with the exception of more than a dozen countries, mostly in Africa and the Middle East.

Government employees, soldiers and private school teachers, all of whom pay into separate pension systems, are also not required to pay into the national fund.

Currently, 22 million people pay into the fund, which as of the end of January operated a total reserve of 743 trillion won.

According to the National Pension Service, 99.8 percent of that is invested in the financial market. Domestic investments account for 64.5 percent, while the remainder is invested globally.

Nearly 42 percent is invested in domestic fixed income. Another 22.3 percent is invested in global equity and 17.3 percent is in domestic equity.

As of end of 2020, the pension fund accounts for 7 percent of the stock market’s total capitalization.

Additionally, there are 313 companies listed on the Korean stock market in which the pension fund holds at least has a 5 percent stake — up 7 percent from the end of 2018.

The pension fund had a more than 10 percent stake in 96 companies by the end of 2019, a 22.5 percent on-year increase. Those companies include major conglomerates such as Samsung Electronics (10.69 percent), SK hynix (10.17 percent) and Hyundai Motor (10.46 percent).

The national pension fund is also the largest stakeholder of nine major companies, including KT, Shinhan Group, Hana Financial Group and the country’s largest steelmaker, Posco.

The pension fund’s annual yield by the end of 2019 was at 11.31 percent.

The pension fund made 73.4 trillion won in its investment profit. This is outstanding considering that it collected 47.8 trillion won from the 22 million subscribers on their pension payment.

Global equities accounted for most of those yields, with those investments returning 30.63 percent last year. Investments in local equity reported a profit of 12.58 percent while overseas bonds reported an 11.85 percent return. Domestic bonds’ yield was 3.61 percent.

However, last year’s profits could easily be erased depending on how deeply the coronavirus pandemic affects global finance. As of January, the investment yield had dropped to 0.6 percent.

Korean equities returned a 2.92 percent loss, while overseas equity investments returned a 2.13 percent yield and overseas bonds returned a 4.04 percent profit.

What does the recent turbulence in global markets mean for the future of the country’s insurance funds?

Among the four social security insurance funds, the National Pension Service has been the most aggressive investor in the Korean stock market.

Employment insurance also has significant exposure to domestic finance, with 22.3 percent of its reserves invested in the local market. However, the largest investment is made in Korean bonds at 47 percent. Global investment accounts for 7.5 percent.

The national health insurance fund, on the other hand, has been more conservative, with 28.3 percent invested in long-term bank deposits, 21.3 percent invested in financial bonds and 20.6 percent in financial trusts.

Workers’ compensation insurance invests most heavily in domestic bonds, which account for 52 percent of its reserves. The second-largest investment is in local equities, at 22.7 percent, while 11 percent is in global stocks.

One of the biggest changes in recent years is that these funds have been reducing their investments in local markets and have been increasing investment in global equities as global markets — especially the U.S. — have maintained a bullish rally since the 2008 financial crisis.

This has helped improve investment yields.

The employment insurance fund enjoyed a 7 percent profit return on its investment last year, a sharp turnaround from its 2.22 percent loss in 2018.

As is the case with the national pension fund, global investment contributed largely to the improvement in the employment insurance fund’s profits. Global investment profit was up 31 percent, higher than the 10.2 percent profit for domestic equities and much higher than the 2.41 percent profit from domestic bonds.

The situation is similar for the workers’ employment insurance fund, which saw its profit increase 7.58 percent, a sharp turnaround from the previous year’s 2 percent loss.

Global equities investment profit soared 31 percent, higher than the 11 percent profit made from investing in local equities and much higher than the 2.98 percent profit from Korean bonds.

The social insurance funds are currently more focused on the domestic stock market than global equities. But the recent volatility in markets, both locally and globally, have undoubtedly have an impact on the funds — especially the national pension fund.

Although it has recently recovered, the Kospi tumbled sharply in March, with arguably more volatility than the index had experienced at any prior time.

Several of the funds have announced intentions to increase global investments.

The national pension fund said it will expand overseas investments, including global bonds, to 50 percent by 2024.

The fund has also in recent years have been actively exercising its shareholders’ rights on stakes they own in local companies.

In the past, the national pension fund remained mostly on the sidelines. However, amid problems with family leadership within Korea’s top conglomerates, the pension fund has increasingly shifted into a stewardship role, more frequently exercising its substantial voting power on major issues.

BY LEE HO-JEONG [lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)