Investors who bet against Korea lost big

![An employee looks at the benchmark Kospi index displayed on the screen attached to the walls of dealing room of KB Kookmin Bank, in the financial district of Yeouido, western Seoul, Wednesday. [YONHAP]](https://koreajoongangdaily.joins.com/data/photo/2020/05/13/608e2be9-9ead-4855-bcfe-c970adb921c3.jpg)

An employee looks at the benchmark Kospi index displayed on the screen attached to the walls of dealing room of KB Kookmin Bank, in the financial district of Yeouido, western Seoul, Wednesday. [YONHAP]

It has long been said that “when the United States sneezes, Asia catches a cold.” That may not be so true anymore.

Hong Kong's Nine Masts Capital, which is known for making high-risk bets on volatility, suffered one of its worst losses in its eight years in March as it gambled that equity market swings in Asia would exceed those in the United States. The fund lost 23.5 percent as stocks in Korea, Japan and China fell less than expected.

Bloomberg quoted Bharat Sachanandani of Societe Generale explaining that many hedge funds suffered losses “blind-sided by a decade-long relationship assumption that when the U.S. sneezes, Asia catches a cold and vols spike much higher.” The assumption that the volatility in Asia will be higher than in the United States fell apart in March as “the coronavirus pandemic roiled global stocks.”

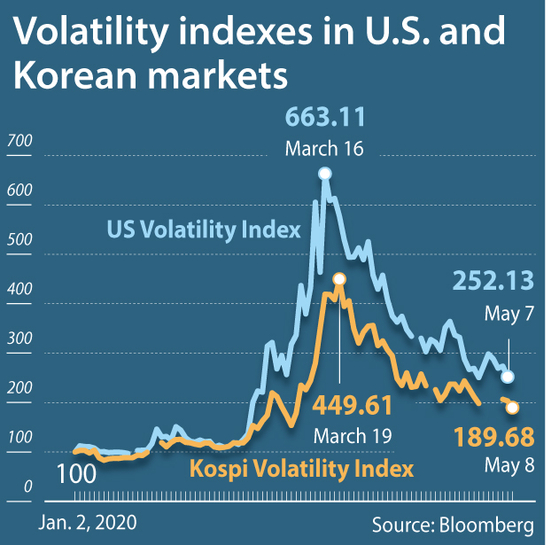

According to data generated by Bloomberg, the difference can be seen in the volatility indexes of the Kospi (Vkospi) and S&P 500 (VIX). When fears of the coronavirus reached its peak on March 19, the Korean index hit 449.16 points. The VIX peaked at 663.11 points in March 16.

The volatility index, also known as the Fear Index, represents investor expectations of market volatility for the following 30 days. The higher the index, the deeper the fear among investors. The 214 point difference in the two markets for March indicates that the anxiety felt by investors was higher for the U.S. market than for the Korean markets.

Experts say buying by retail investors, dubbed the “Donghak Ant Revolution,” cushioned the blow from the coronavirus and kept the volatility index in the Korean market relatively low. The volatility in the benchmark Kospi was minimized as more individuals bought stocks.

“Renowned hedge funds made bets that the Korean market would collapse from the coronavirus crisis, however the fall proved to be less severe than its U.S. counterparts. The index was largely supported by retail investors that took place of institutional and foreign investors who left the market during the coronavirus outbreak,” said Yoo Dong-won, head of Global Investment at Yuanta Securities.

“Retail investors were holding up the market from 2005 through 2007,” added Yoo. “This time the money from retail investors headed to individual stocks, such as Samsung Electronics.”

Bloomberg reported that such a dramatic reversal “highlights the risk of relying on historical market relationships to guide investments.” The trades turned out to be a “disaster for some hedge funds,” said Sachanandani.

Bloomberg writes that other reasons may help explain the lower-than-expected volatility in the Asian stock market. The Japanese government rolled out an aggressive monetary stimulus program and bought stocks when the market declined. In the case of China, its government’s “active intervention in the economy and markets” during the coronavirus outbreak helped lower market volatility.

BY CHUN SU-JIN [kang.jaeeun@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)