P2P lending could be regulated right out of existence

![[SHUTTERSTOCK]](https://koreajoongangdaily.joins.com/data/photo/2020/08/25/fdf25a5b-a293-4746-9b9b-22124a78d232.jpg)

[SHUTTERSTOCK]

Peer-to-peer (P2P) lenders will soon have to prove they are not loan sharks if they want to stay in business. And that may not be easy.

The practice of peer-to-peer lending involves people and business connecting directly online so that one may borrow from the other. So far, it has been lightly regulated and the domain of errors, missteps and outright scams.

After the Act on Online Investment–Linked Financing and User Protection comes into effect on Aug. 27, players who want to continue to operate P2P lending businesses are going to have to meet a number of new requirements.

They must have equity capital of 500 million won ($421,000) and a compensation plan for investors and must appoint a compliance officer.

When the act was first passed late last year, regulators were hopeful it would strengthen the P2P lending business and encourage innovation.

With just one day before the law becomes effective, optimism is nowhere to be found. The worry is that the legislation will scare off players and create barriers to entry that will discourage newcomers.

Financial regulators are concerned as so many businesses in the industry “do not even meet the basic requirements", including the required capital. Out of 240 businesses offering this type of financing, industry insiders say only 10 of them will survive, as many do not meet the requirements stipulated in the new law.

Another concern is that the market is losing credibility due to a series of fraud and embezzlement cases.

Pop Funding, an operator acknowledged by the Financial Services Commission (FSC) for its innovation, is currently under investigation for a 55-billion-won Ponzi scheme. The CEO of Nexrich Funding, also a P2P business, was arrested for fraud and embezzlement. There are many other operators, such as C-So Funding and Top Fund, that were troubled for being late with repayments.

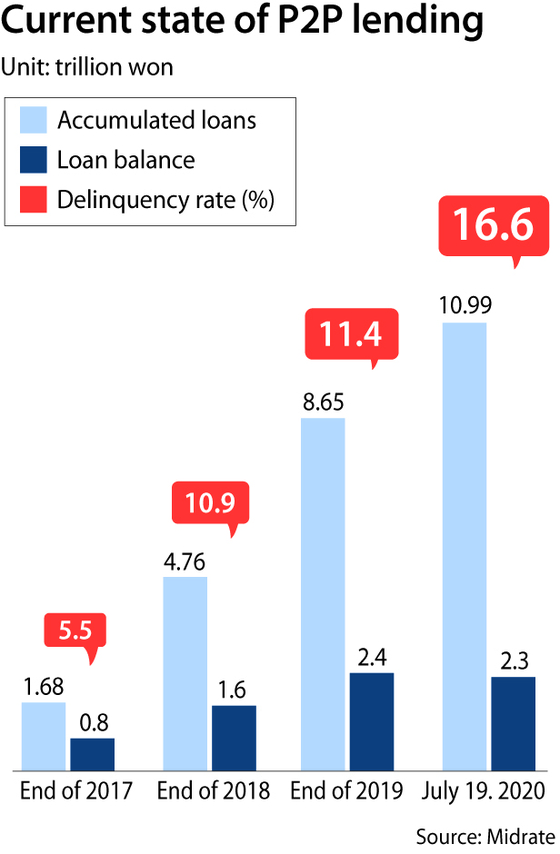

Delinquency rates are also increasing to worrying levels.

According to Midrate, a market tracker of P2P lending, the average delinquency rate in the industry was 16.69 percent as of Aug. 4. This up from 11.47 percent earlier this year.

Financial regulators have issued a consumer warning on such investments and ordered all businesses operating in the P2P market to submit an audit report.

“The new law will give the businesses a one-year grace period, but operators that do not meet the necessary requirements will likely have to close,” said an official from the Financial Supervisory Service (FSS).

Another issue of concern is that some large operators are under investigation for violating the credit business act by imposing interest rates higher than the 24-percent limit imposed by law.

The FSC says that if fees are added to the rate of interest, the effective rate is too high. P2P businesses respond that fees and rates are two separate issues and that the platform fees are never directly charged to the customers.

If financial regulators conclude these companies have violated the credit business act, P2P lending will be shaken.

“If we conclude an operator to have violated the law, it would have to close the business completely for six months. We are carefully deciding whether such strong measures would be necessary,” said an official from the FSS.

![Investors in P2P lending operator Pop Funding demand brokerage firms compensate them for losses in front of the Seoul Southern District Court on June 29. [YONHAP]](https://koreajoongangdaily.joins.com/data/photo/2020/08/25/c77571b5-1c96-407a-b03b-a4545a616b6e.jpg)

Investors in P2P lending operator Pop Funding demand brokerage firms compensate them for losses in front of the Seoul Southern District Court on June 29. [YONHAP]

Others are concerned that P2P lending will become an alternative channel for people seeking to finance their homes. Most operators offer mortgage loans on their platforms, with some promising up to 85 percent loan-to-value ratio. They can do this because they are not banking institutions, which are capped in terms of the loan-to-value ratio.

Experts worry that this will cause a "balloon effect" where individuals take out loans from commercial banks and get the rest from P2P operators.

Operators claim they have made efforts to strengthen self-regulation.

“It’s highly unlikely for a borrower with good credit scores to go to P2P lenders to finance purchasing of houses, since the interest rate is much higher here than commercial banks. We inform customers that the funds should not be used to purchase property,” said one industry source.

The FSS has yet to come up with a regulation to stop people from borrowing funds from P2P lender to purchase homes, but is keeping "a close watch for potential problems.”

Officials from the finance industry say the new law will provide an opportunity for a fresh start.

"If the law forces operators to be more transparent in their businesses, [financial regulators] can create a healthy business model as they are able to collect and analyze credit data from marginal borrowers, which have not been included in statistics," said Chung Yoo-shin, a dean of Sogang University's Graduate School of Technology and Management.

"It will help filter out the good operators from the bad ones.”

BY SUNG JI-WON [kang.jaeeun@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)