Apple Pay's Korea arrival is a rumor good enough to be true

![A close-up of a man using Apple Pay to pay for public transportation [SHUTTERSTOCK]](https://koreajoongangdaily.joins.com/data/photo/2022/10/20/66ea0668-f993-4dda-b6bd-594d2215f5ce.jpg)

A close-up of a man using Apple Pay to pay for public transportation [SHUTTERSTOCK]

In Korea, it doesn't work, and neither banks nor card companies in the country support the service.

The lack of Apple Pay in one of the most advanced and high-tech economies in the world is one of the enduring mysteries of fintech, and rumors, always unconfirmed, are repeatedly spawned about its imminent arrival. Speculation about Apple Pay in Korea began to circulate more than five years ago.

The latest involves a deal between the Cupertino, California, maker of the iPhone and Hyundai Card.

Hyundai Card is a privately-held credit card company more than a third owned by Hyundai Motor. In May, it halted plans for an initial public offering and instead sold almost 20 percent of its stock to two companies from Taiwan.

On Oct. 6, a Korean iPhone user posted on Naver what appears to be terms and conditions for the use of Apple Pay in Korea. Some iPhone users claim to have registered their Hyundai Cards with their iPhones earlier this month.

In the posted user agreement, the text is contract for the use of the Apple Pay transaction service provided by Hyundai Card.

Hyundai Card isn't confirming a possible deal with Apple and declined to comment on the posted user agreement. Notoriously leak-free Apple did not respond to questions about entry to the Korean market including the rumored arrangement with Hyundai Card.

Precedent suggests caution. In early 2021, an agreement between Hyundai Motor and Apple for the making of an Apple EV was rumored and widely reported. The deal never materialized and the whole fiasco became the subject of an insider trading investigation of Hyundai Motor executives by the Financial Services Commission.

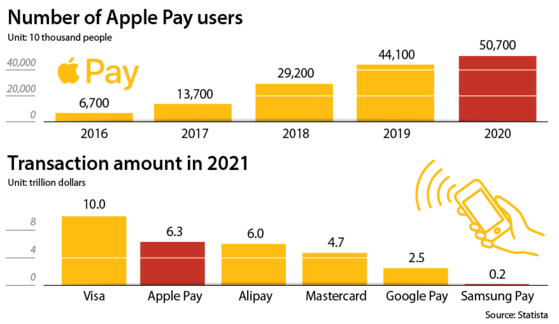

Apple Pay was the second largest payment service provider globally following Visa in 2021. It was followed by Alipay, Mastercard, Google Pay and Samsung Pay, according to Statista.

Apple Pay is available in around 60 countries and the number of its users reached broke 500 million in September 2020.

Hyundai Card was the third largest credit card operator in terms of transaction amount through September this year, after Shinhan Card and Samsung Card, according to Yonhap.

“Part of the reason the Apple Pay entrance did not take place smoothly is because of the influence of Samsung in Korea,” said Lee Chang-min, an analyst at KB Securities. “But market share for Apple smartphones is rising and that may affect” the success of Apple Pay in Korea.

If a deal between the two does happen, it would be significant for many reasons, affecting the credit card business, which is struggling for growth, the smartphone market and payments in Korea, which are falling behind in terms of technology for contactless transactions.

The credit card business is mature and slow growing in Korea. So for a credit card company to show meaningful growth, it has to increase market share because the market isn't getting any bigger, according to Lee Jeong-hwan, assistant professor, College of Economics and Finance, Hanyang University.

“To change the ranking in the stagnant industry, card companies have to continuously offer special events to customers. And an exclusive agreement with Apple Pay is one such marketing strategy that could be effective in attracting young customers that use iPhones,” Lee said.

The number of credit cards was up 2.7 percent this year through June, but the number of credit cards that were not used for a year or longer grew 11 percent in the same period, according to data from the Financial Supervisory Service in September. The number of debit cards issued declined 0.6 percent in the same period.

“Hyundai Card will be able to have exclusive access to iPhone users that are largely young consumers,” said a source from a competitor, who has no direct knowledge of a deal between Hyundai Card and Apple. “That itself could be effective marketing. If the strategy turns out to be successful, other major credit card firms will also start to partner with Apple Pay.”

Hyundai Card has been particularly active in targeting young customers, like with the offering of private label credit cards for influencers and Starbucks users.

The effectiveness of Apple Pay on raising Hyundai Card’s earnings may not be that big.

If 50 percent of 11.32 million iPhone owners in Korea use Apple Pay, and they make around 200,000 won ($140) of transactions monthly, which is around 60 percent of Samsung Pay monthly average transactions, users will spend around 13.6 trillion won annually, according to Kim Jae-woo, an analyst at Samsung Securities in a report Oct. 4.

That is only around 1.4 percent of all transactions made with cards in Korea in 2021.

“The increase of the market share will be only 1.7 percentage points even if Hyundai Card makes all the transactions, limiting the chance of changing the industry structure,” Kim said. “Maintaining the exclusive partnership and the length of the contract period will be the key” to dramatically improving Hyundai Card’s market share in a mid to long term, he added.

As part of the promotion for Apple Pay, Hyundai Card will return annual membership fees as cashback and offer discounts for the purchase of new Apple devices, according to local media reports.

The smartphone business may also be affected, as Samsung Pay was considered a major benefit of Galaxy smartphones over iPhones.

“If a proposed bill to ban recording of phone conversations passes and Apple Pay becomes available, there will be no need to use Samsung smartphones,” said a commenter on the iPhone & iPad & Mac User Community.

Samsung had 58.38 percent of the smartphone market in Korea in September, down from 64.51 percent in the same month a year earlier, according to statcounter. Apple’s market share grew to 34.1 percent from 27.39 percent in the same period.

According to a small survey of the online community in September, 45 percent said they will “immediately” change their phones to iPhones once Apple Pay is available, while 34 percent said they will continue using Galaxy smartphones.

More than 90 people voted.

To make Apple Pay feasible in Korea, devices that support near-field communication (NFC) need to be installed at stores. Apple Pay only works via NFC, a technology that allows for short-distance wireless communication between a terminal and a device.

Less than 5 percent of stores in Korea are equipped for NFC transactions. NFC terminals are expensive, more than 100,000 won per unit.

Unlike Apple Pay, Samsung Pay supports both NFC and magnetic secure transmission (MST), a mobile payment technology that processes transactions by sending magnetic signals. It can be used with existing card terminals at stores.

“I see it as a positive factor” for Samsung Pay, wrote an online commenter named ironPhone on the Samsung Smartphone Community last month, referring to Apple Pay’s market entrance. “If Apple Pay becomes available, the use of NFC payments on Samsung Pay will soon grow.”

“Unless NFC technology is available at stores nationwide, impacts of Apple Pay will be small,” said Lee from KB Securities.

“It took more than 20 years for the infrastructure of credit card devices to be established nationwide since the 80s,” said the credit-card company source. “Other credit card firms will of course team up with Apple Pay once NFC is installed nationwide. But due to the cost and the time required to install the technology, we currently do not dare jump in.”

Commissions are another issue.

Unlike Samsung Pay, which only charges a fixed rate to credit card operators for using the payment technology, Apple Pay requires a commission for transactions.

Apple Pay collects 0.15 percent of every Apple Pay transaction in the United States.

If Apple charges the same in Korea, stores and credit card companies could be affected. This could discourage stores from adopting the technology, ultimately slowing the spread of Apple Pay usage.

But Apple could be more flexible in Korea, considering the 0.05 percent commission it charges in Israel.

“If the performance of Apple Pay is smaller than expected in the initial phase of the adoption, the private sector may delay the adoption of the payment device, slowing the growth of Apple Pay,” said analyst Kim.

But he added that the start of the service will intensify the competition and force companies to provide better technologies, which they have been reluctant to do these days given higher interest costs and economic instability.

BY JIN MIN-JI [jin.minji@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)