Greedy banks threaten economy

The author is a senior editorial writer at the JoongAng Ilbo.

One sector is thriving amidst rapid rises in interest rates and consumer prices. The four major financial groups — Shinhan, KB, Hana and Woori running commercial banks — earned nearly 14 trillion won ($10 billion) in net profit from January to September. Their interest income alone exceeded 29 trillion won, up 20 percent from the same period a year ago. As the Bank of Korea bumped up the base rate from 1.25 percent to 3 percent this year, commercial banks raised their lending rates faster than deposit rates to benefit from the margin. Banks usually earn profit under a rate rising environment at the expense of consumers.

The deposit-to-loan rate gap in commercial banks rose from 2.05 percentage points at the end of 2020 to 2.21 percentage points a year later and to 2.46 percentage points by September this year. On top of that, banks upped the share of new loans priced with floating rates to 83 percent in the second quarter from 68 percent in 2020 on the bet the rates would go higher.

Banks do not owe their enhanced bottom line to better management, but largely to rate increases. The concept does not fall under the Yoon Suk-yeol administration’s slogan of “fairness and common sense.”

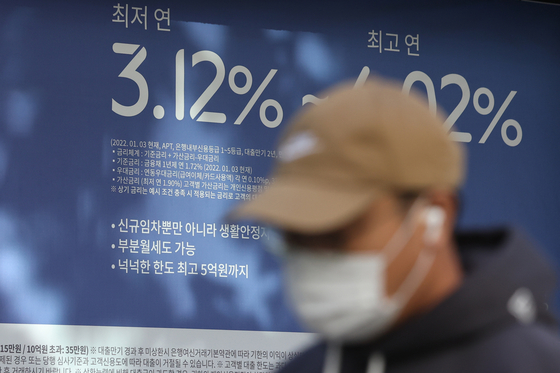

Nearly all lending rates have topped 7 percent, the highest in 13 years. Since the Monetary Policy Board of the central bank is mostly likely to deliver another hike possibly beyond the usual 25 basis points on a Nov. 24 meeting, lending rates will break 8 percent. They could top the 9 percent range next year as rate increases will continue as long as inflation remains high. Banks explain the gap in lending and saving rates usually widens during a tightening period. They argue the difference should be determined by market principles. During economic downturns, the lending rate usually would go higher due to a lack of money, say the banks. But when interest income swells, banks could consider moderating the rises in lending rates. But the thought does not come to their heads.

Instead of sharing the pain with the rest of our society, banks indulged employees. The average pay of four major banks exceeded 100 million won last year. Those opting to retire early packed up three to four years of their annual salary. Including special severance pay, some banks paid 500 million won to 1 billion won to outgoing employees. The financial industry union threatens to start a general strike by demanding retirement age be extended to 65 and a 4.5 workweek.

That’s not all. Bank CEOs extend their seats into the second or third term based on their impressive income report card. They woo customers, but do not care to lessen their inconvenience. Although social restrictions have been fully lifted, banks keep to their one-hour-shortened business hours. The labor and management buy time by tossing the liability.

The banking sector is monopolized by the four majors. They are the dominant money lenders. Their influence grows during a monetary tightening period in particular. Household and corporate borrowers are at their mercy. If banks keep to their margin-based business, they will stay the winners and the rest the losers. But banks cannot win forever. If households and companies default on their loans due to excessive interest costs, the risk builds up at banks. Banks expand their business during a boom, but during hard times, they tighten loans and gather insolvencies to seek a government bailout at the end.

The practice has not changed despite two major financial crises. Much has been discussed about a comprehensive corporate lending platform, megabanks, digitalization and internationalization. But they have not been able to venture beyond the local market.

According to the World Competitiveness Rankings by Swiss-based IMD Business School, South Korea’s banking and financial services ranked 47th out of 64 countries this year, falling from 42nd a year ago.

The government also has not changed. Late last year, the Financial Services Commission (FSC) issued a press reference release advocating for banks by saying the rises in loan rates should not be blamed on banks.

The FSC under the new government is the same. The government must stand by the public, not the banks. State interference in financial management cannot be right. But bureaucracy to contain greedy practices of banks should be welcomed.

Goldman Sachs and Morgan Stanley caused controversy by handing out generous bonuses to executives and employees with their massive bailout funds after the Wall Street meltdown. They went back to avaricious days as soon as they escaped the danger. Their profiteering triggered the Occupy Wall Street protests in 2011. Korean banks also are heavily indebted to the public. Tax funds of 168 trillion won went to rescuing commercial banks after the Asian financial crisis in the late 1990s. During the 2008-09 global financial crisis, the government raised a 20-trillion-won fund to bolster their capital. Banks enjoying the interest binge must ask themselves if they can dare to ask for help the next time they run into trouble.

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)