Rate cap pushes Korea's most vulnerable to loan sharks

![A payment being made at a café in Seoul on Nov. 22. [YONHAP]](https://koreajoongangdaily.joins.com/data/photo/2023/01/29/d6c6fc8a-a8b5-4e6f-b139-09a95f8cd8f0.jpg)

A payment being made at a café in Seoul on Nov. 22. [YONHAP]

Lenders are prohibited from charging more than 20 percent annual interest. Financial institutions and lenders that violate the rule can face penalties of up to three years of imprisonment or maximum 30 million won ($24,000) in fines.

The purpose of the regulation is to protect debtors from having to pay excessive interest.

As the central bank raises its base rate, which is up 3 percentage points in two years, lenders have simply stopped making loans to riskier borrowers. The spread between the cost of money and the lending ceiling has narrowed, and they can't charge people with bad credit enough to make the business worthwhile.

Hyundai Capital has stopped taking new loan applications from Toss or Kakao Pay. Apro Financial, the operator Rush and Cash, stopped writing new loans last month.

“We’re not sure when we will resume taking loan applications from platforms,” said Yang Seong-sik, senior manager at Hyundai Capital’s public relations team. “We raise money by issuing bonds, but the rate has tripled as of the end of last year compared to early 2022.”

People with low credit scores were the first to be shut out from the loan services.

Loans extended by secondary financial institutions fell 5.9 trillion won last year, according to the Financial Services Commission (FSC) in January.

Loans extended by SBI Savings Bank fell 46.3 percent in the fourth quarter compared to a previous quarter, while loans by Welcome Savings Bank plunged 85.4 percent in the same period, according to Korea Federation of Savings Banks.

“The purpose of cutting the legal lending rate is to practice inclusive finance, but it has consequently reduced the opportunity” for some people, said Choi Chul, consumer economics professor at Sookmyung Women’s University at a conference hosted by Consumer Loan Finance Association in November.

After the legal lending rate was revised down in July 2021, the total unsecured loans outstanding fell 21 percent from a year earlier, said the association.

“People that borrow near the legal lending rate are those that urgently need money,” said Lee Jeong-hwan, an associate professor at College of Economics and Finance at Hanyang University. “They borrow at a high rate with a short maturity, like a couple of months. Blocking the channel where they can urgently finance loans forces them to knock on the doors of illegal loan firms, which hire illegal collectors to retrieve the funds.”

As complaints about the falling legal lending rate grew, the FSC started looking at possibly adjusting the maximum lending rate.

The FSC “is looking over the present conditions,” said Choi Keun-ho, a spokesperson for the FSC. “But to what extent the FSC is reviewing hasn’t been confirmed.”

Cho Moon-hee, a spokesperson for the FSC's consumer finance department, said the FSC is "very cautious" about discussing the rate adjustments, adding that the authority is "monitoring" the market situation.

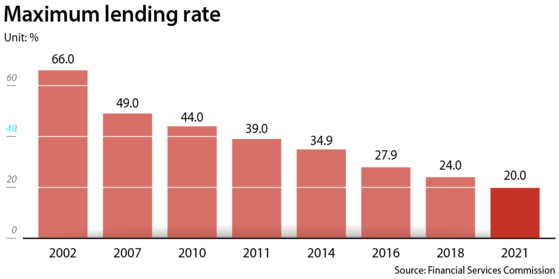

The legal lending rate was 66 percent in 2002. GDP growth that year was 7.7 percent, according to Statistics Korea. But the rate has gradually fallen along with Korea’s economic growth, which fell to 2.6 percent last year. The current 20 percent was revised in 2021 from 24 percent.

Adopting a variable maximum lending rate is an idea proposed by some experts, as interest rates for procuring funds by financial institutions is volatile.

If the rate for procuring funds rises, the spread with the maximum lending rate falls. That means lenders shut out households that had borrowed funds near the maximum rate because their lending rate cannot rise any further. Losing access to loans could make it difficult for financially vulnerable households to roll over the debt.

If vulnerable households “face restrictions rolling over the borrowed money, overdue payments can spread across the financial sector,” said Kim Mee-Roo, a researcher at the Korea Development Institute.

Almost 85 percent of households that took out loans at a rate between 18 and 20 percent were vulnerable households as of June, according to Kim, citing data from a credit rating agency.

Connecting the maximum lending rate with a monetary stabilization bond with one-year maturity or state bonds with two-year maturities are some of the ways that can be adopted to adjust the legal lending rate, added Kim.

Similar methods are already used abroad.

In Germany, the maximum is double the average market rate or average market rate plus 12 percentage points, whichever is lower. In Italy, the rate cap is 1.5 times the average market rate.

These countries charge different maximum lending rates for different types of loans, unlike in Korea where the fixed rate cap is applied to all types of loans.

“The total amount of unsecured loans borrowed near the maximum lending rate is a lot smaller than other types of loans, like mortgages. So the pressure to pay back the loans caused by the rate increase is limited,” Kim added, “A reduction in consumer benefits caused by being excluded from the loan market is a lot bigger.”

BY JIN MIN-JI [jin.minji@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)