Korea's corporate reform push pales in comparison to Japan's

![Left: An electronic board in central Seoul shows Korea's benchmark Kospi on June 27. Right: A person walks in front of an electronic screen showing Japan's Nikkei 225 index on February 26. [YONHAP/AP]](https://koreajoongangdaily.joins.com/data/photo/2024/07/02/54cf82fc-5459-42ec-b4e2-f3b88d48f9fb.jpg)

Left: An electronic board in central Seoul shows Korea's benchmark Kospi on June 27. Right: A person walks in front of an electronic screen showing Japan's Nikkei 225 index on February 26. [YONHAP/AP]

[NEWS ANALYSIS]

The government's much-hyped Corporate Value-up Program aims to emulate the success of a similar initiative in Japan — but nearly two months after its launch, it has failed to attract active participation from market players, at least as of yet.

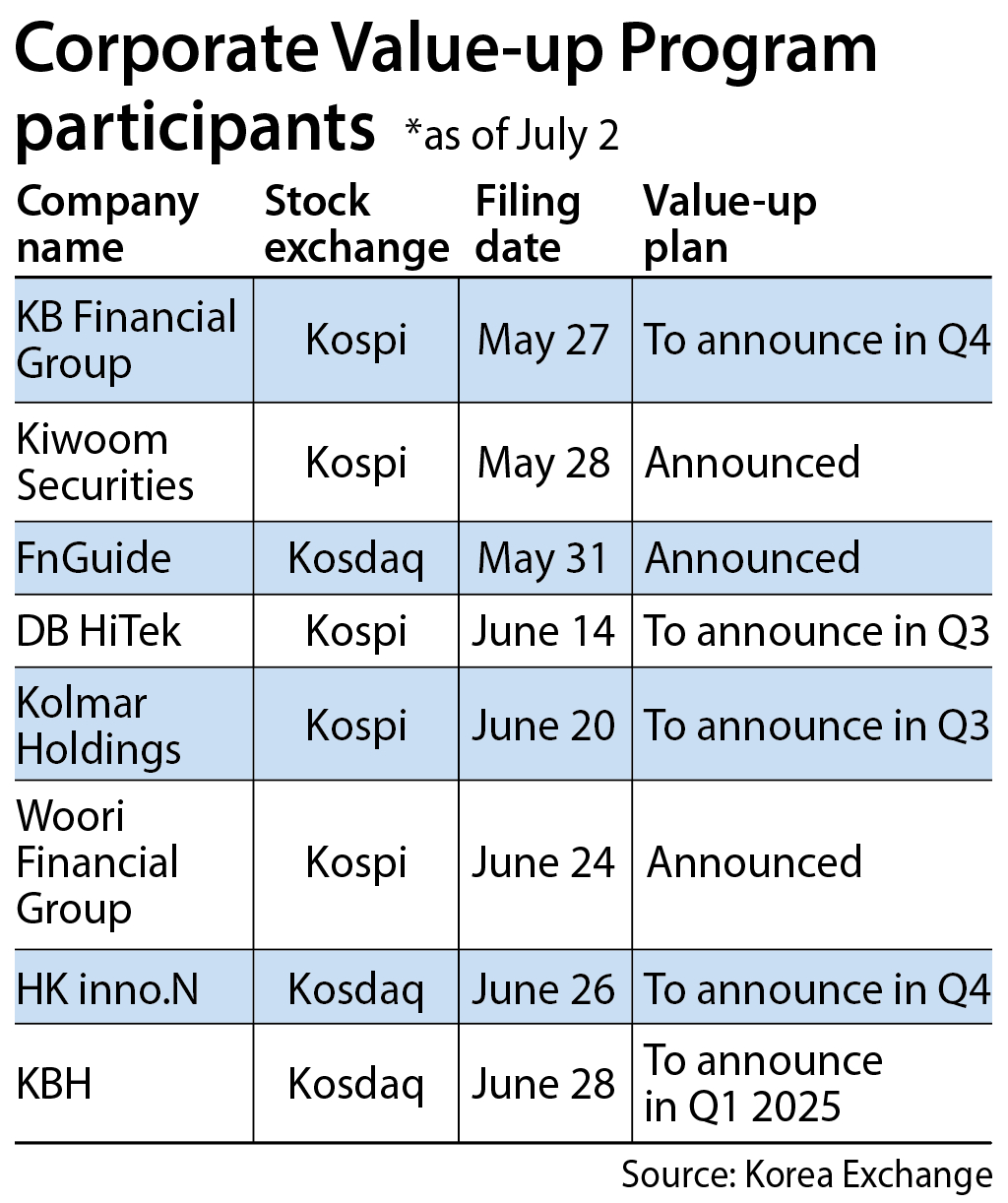

Only eight companies, including KB Financial Group, out of over 2,600 listed companies in Korea announced their participation, either by outlining plans for shareholder value enhancement or by scheduling the release of such plans.

Stock prices have not responded much yet, as the benchmark Kospi gained only 5.6 percent so far this year, while Japan's Nikkei 225 rose 18.4 percent and the S&P500 advanced 14.8 percent during the same period.

Investors are casting doubts over the voluntary program’s lack of enforcement bite, while also pointing out that it failed to address an arguably more fundamental issue behind the poor performance of Korean stocks: an outdated corporate governance structure.

“The current government lacks a clear CG [corporate governance] road map to guide its reform efforts,” said Stephanie Lin, a research manager at the Asian Corporate Governance Association, in a recent report.

“While the CVP [Corporate Value-up Program] has garnered much attention, incentives for corporate participation are still unclear,” Lin noted.

The Korea discount was often blamed on ever-present geopolitical risks stemming from the missile-firing neighbor to the north, shabby shareholder returns and poor corporate governance structures that have often worked in favor of controlling shareholders at the cost of financial gains for minority shareholders.

The Yoon Suk Yeol administration’s value-enhancing system, taking after a similar program implemented by the Japanese government in March of last year, mainly focuses on improving listed companies' shareholder return policies.

The Korean version of the shareholder value enhancement drive resembles its Japanese counterpart in many respects, including the voluntary-basis approach and incentive measures.

However, Seoul's attempt, still in its infancy, lacks a clear standard regarding target companies, while the Japanese authorities specifically recommended the participation of companies with a price-to-book ratio of one or less.

The initiative also does not include any solid plans to directly address governance reform, unlike in Japan, where the government has been implementing measures to incentivize or pressure companies to improve their shareholder return policies and corporate governance since 2013.

Korea's chief financial regulator also pointed to corporate governance structure as one of the major obstacles in the capital market's advancement.

"During the period of rapid growth in the past, when a company's pace of expansion outstripped asset accumulation, a unique corporate governance structure specific to Korea emerged, enabling controlling shareholders to maintain control over the company with only a small stake," said Financial Supervisory Service (FSS) Gov. Lee Bok-hyun during a corporate governance seminar on June 26.

![Financial Supervisory Service Gov. Lee Bok-hyun speaks during a seminar on a governance reform for the corporate value-up initiative held in western Seoul last Wednesday. [YONHAP]](https://koreajoongangdaily.joins.com/data/photo/2024/07/02/29465e61-6b86-4cfc-bab1-7491dcd069b6.jpg)

Financial Supervisory Service Gov. Lee Bok-hyun speaks during a seminar on a governance reform for the corporate value-up initiative held in western Seoul last Wednesday. [YONHAP]

"Such a governance structure is vulnerable to a conflict of interest between controlling and minority shareholders, and increases risks of discrepancy between a company's performance and shareholder value."

One notable example was a controversial merger between Samsung C&T and Cheil Industries in 2015, which benefited Samsung Electronics Executive Chairman Lee Jae-yong — then vice president — and his family members.

As the exchange ratio for the merger deal was drastically favorable to Cheil Industries, in which the Lee family held a significant stake, it helped them during the succession process from the late Chairman Lee Kun-hee to his son Jae-yong.

The deal, however, hurt the stock value for minor shareholders of Samsung C&T significantly. The shareholders filed a lawsuit against the companies and the Samsung-owning family in 2015 that was ultimately unsuccessful, before filing another in 2020, but proceedings have been sluggish for the past four years.

SK Group, which has been struggling to make ends meet with its money-losing EV battery maker SK On, is mulling a merger of SK Innovation and SK E&S as SK Innovation has been under burgeoning financial distress to fund the massive capital expenditure of SK On.

If the exchange ratio is set favorably for SK E&S, in which SK Inc. holds a 90 percent stake, shareholders of SK Innovation are likely to find themselves holding the short end of the stick as their stakes in the company may shrink.

As part of the corporate governance reform, the FSS governor has recently been floating the idea of revising the Commercial Act to expand the scope of responsibility for corporate directors in order to bolster a safety net for minority shareholders.

Korea’s largest business lobby groups have strongly opposed the proposed revision, saying that it will increase the risks of legal disputes and slow down the decision-making process, especially regarding decisions made for the long-term growth of a company that may result in a short-term loss for shareholders, such as merger and acquisition deals.

Hwang Hyeon-young, a research fellow at the Korea Capital Market Institute, noted that the revision of the clause itself is not likely to change much in reality due to its abstract nature, but may serve as a starting point for governance reform as a symbolic gesture.

"For example, there is no regulation in Korea that [sufficiently] protects minority shareholders or holds directors responsible when minority shareholders suffer losses during a merger process, unlike in the United States, Japan or Germany," said Hwang.

"As such, there are misconceptions surrounding the relevant systems and legal interpretations [in Korea], so I believe the [revision] can be a starting point for a general refinement."

Meanwhile, some have also pointed fingers at Korea's excessive inheritance tax rate as the reason for the discount, arguing that the heavy tax burden is incentivizing controlling shareholders to keep share prices low.

"Excessive inheritance tax has been causing many side effects including the outflow of wealth and tax evasion," said the Korea Chamber of Commerce and Industry in a tax system reform proposal filed with parliament and the government earlier this year.

"The heavy inheritance tax is discouraging companies preparing for management succession from increasing shareholder returns, while encouraging unfair internal transactions between affiliates that the controlling shareholders own a significant stake in," said a spokesperson for the business lobby.

BY SHIN HA-NEE [shin.hanee@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)