[Korea and the fourth industrial revolution <10-1 Finance>] Need investment advice? Call a robot (국문)

[BAE MIN-HO]

서울 우리은행 본점 입구. 매끄러운 흰색 로봇이 반짝이는 파란 눈으로 손님을 맞는다.

One lady goes up to the machine and asks Alpha, the robot’s name, whether it’s eaten lunch yet, a common greeting in Korea.

한 여성이 로봇, ‘알파’에게 다가가 안부인사로 점심은 먹었냐고 묻는다.

Alpha turns its head toward the woman and playfully responds, “Don’t dare to ask unless you’re buying.”

알파는 고개를 돌리며 “안 사줄 거면 묻지 마세요”라고 장난스럽게 답한다.

The lady chuckles and then asks Alpha for the latest stock market numbers.

그 여성은 유쾌하게 웃으며 알파에게 최근 주식 시장이 어떠냐고 묻는다.

The interaction might seem contrived, but the gimmick belies the machine’s true power: the ability to recommend financial products based on the users’ investment appetite.

일반 은행에서 흔히 볼 수 있는 장면은 아니다. 어쩌면 알파의 재치에 감탄하겠지만 알파의 진정한 능력은 그게 아니다. 고객의 투자 성향에 따라 금융 상품을 추천하는 능력이다.

Alpha asks investors three questions about the amount of risk they’re willing to take and their preferred type of investment, and based on the answers, the robot can generate a list of recommended funds for the client.

알파는 투자자들에게 세 가지 질문을 던진다. 어느 정도의 리스크를 감당할 의사가 있는지, 어떤 타입의 투자를 선호하는지 등이다. 그리고 그에 알맞은 펀드 상품 목록을 작성해서 고객에게 추천한다.

Woori Bank staff demonstrate its robo adviser, Alpha, at its branch in Myeong-dong, central Seoul, on June 13. [PARK SANG-MOON]

알파는 한국 금융이 나아가는 방향을 보여주는 보여주는 대표적인 사례다. 디지털 기술과 스마트폰 앱은 이제 금융 상담, 투자 포트폴리오 관리 및 실시간 시장 분석까지 제공하고 있다.

In February last year, the Financial Services Commission, Korea’s financial regulatory agency, approved the use of so-called robo advisers, paving the way for the commercialization of automated investment services.

지난해 2월 금융위원회는 로보어드바이저 사용을 허용함으로써 자동화된 투자 서비스 상용화의 길을 열었다.

Many of these advisers use systematic trading strategies aimed at balancing expected returns with risk to devise the optimal portfolio.

대부분의 로보어드바이저는 체계화된 트레이딩 전략을 사용하는데 이는 최적의 포트폴리오를 구성하기 위해 기대 수익과 리스크를 조율하도록 디자인돼 있다.

Analysts expect the widespread use of robo advisers will give general investors access to wealth management services once reserved for high-net-worth individuals because of their lower fees.

전문가들은 로보어드바이저가 대중화되면 고액 자산가 중심이던 자산관리 서비스가 일반 투자자들까지로 확산될 것으로 보고 있다.

“When we look at the case of the United States, where the industry is booming, clients can enjoy advisory services for less than 0.5 percent,” said Park Seon-hoo, a researcher at IBK Economic Research Institute. “Money managers at major banks and securities companies currently charge at least 1 percent.”

IBK경제연구원의 박선후 연구원은 “미국의 자산관리 서비스 수수료는 0.5% 이하”라며 “(한국의 경우) 주요 은행과 증권사의 자산관리 매니저들은 최소 1%의 수수료를 부과하고 있다”고 말했다.

Park believes robo advisers will likely draw Korean millennials, the demographic cohort born between 1980 and 2000, as they have in the United States.

박 연구원은 로보어드바이저 대중화가, 미국에서 그랬던 것처럼, 한국의 밀레니얼 세대(1980~2000년 사이에 태어난 세대)를 자산관리 시장으로 끌어들이는 역할을 할 것으로 기대했다.

Another target client base is the upper middle class whose net assets range from 100 million won ($88,000) to 1 billion won, and even lower than 100 million won. This group could become underserved as legacy investment companies focus on wealthier clients.

또 다른 타겟 고객은 자산 규모 1억~10억원 사이, 혹은 그보다 적은 중상층이다. 더 부유한 고객에 초점을 맞췄던 기존의 투자 회사들이 간과했을 그룹이다.

“Private bankers will be able to give time for consultation when a potential client has at least 600 million won,” said Choi Byung-gil, director at Fount Investment, a robo adviser company. “But we are looking at broader, younger clients who might have fewer assets but potential to grow. Our vision is to serve customers who maintain assets as low as 100,000 won per month.”

로보어드바이저 회사 ‘파운트’의 최병길 이사는 “현재 PB들은 적어도 6억원 정도의 자산이 있는 고객이라야 상담할 시간을 내준다”며 “하지만 우리는 좀 더 광범위하고 젊은 고객들, 즉 현재 자산 규모는 작아도 향후엔 커질 수 있는 잠재력 있는 고객을 주목하고 있다”고 말했다. 그는 “우리의 목표는 월 10만원을 맡기는 고객에게 자산관리 서비스를 제공하는 것”이라고 설명했다.

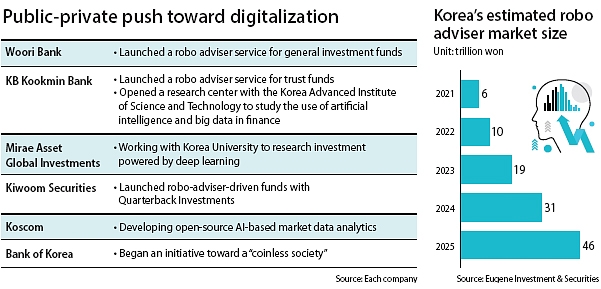

There are currently 12 funds in Korea run by robo advisers, according to the Korea Financial Investment Association, which represents the country’s financial industry.

한국금융투자협회에 따르면 국내에는 총 12개 종류의 로보어드바이저 펀드가 운영되고 있다.

The asset size is estimated to be around 200 billion won. Although the figure pales in comparison to more mature markets like the United States, Korea appears to be on a fair track given the service is only a year old.

로보어드바이저로 운영되는 총 자산 규모는 2000억원 정도로 추정된다. 미국과 비교하면 매우 적지만, 서비스가 허용된 지 1년밖에 되지 않았다는 점을 감안하면 상당한 규모다.

Eugene Investment & Securities predicts Korea’s market growth will flat-line through 2020 but rise to 6 trillion won in 2021 and 46 trillion won in 2025.

유진투자증권은 한국의 로보어드바이저 시장 규모가 2020년까지는 눈에 띌 만한 성장을 보이지 않다가 2021년에는 6조원, 2025년에는 46조원 규모로 확대될 것으로 전망했다.

For the beginning phase, leading banks and securities companies have opted to sign partnerships with robo advising firms like Quarterback Investments, December & Company and Fount to test algorithms and platforms. Quarterback is working with KB Kookmin Bank and Kiwoom Securities, and December & Company has joined with NH-Amundi Asset Management.

시장 초기 단계인 현재 국내 주요 은행과 증권사들은 쿼터백자산운용· 디셈버앤컴퍼니·파운트 같은 로보어드바이저 전문회사와 파트너십을 맺고 있다. 쿼터백자산운용은 국민은행·키움증권과 협업하고 있고, 디셈버앤컴퍼니는 NH아문디자산운용과 계약했다.

“Robo advisers can craft portfolios and manage funds based on quantitative analysis and are more objective than their human counterparts,” said Lee Seung-jun, chief strategy officer and director of investment at Quarterback Investments, the oldest and largest robo adviser firm in Korea.

한국에서 가장 크고 오래된 로보어드바이저 회사인 쿼터백자산운용의 이승준 이사는 “로보어드바이저는 양적 분석을 통해 포트폴리오를 짜고 관리하는 것이 가능하며 인간보다 훨씬 객관적”이라고 말했다.

When the giants come marching

도전장 내는 대형 금융사들

Major Korean firms like Mirae Asset Global Investments, KB Asset Management and Samsung Securities are eyeing moves into algorithm-based wealth management, and when they throw their hats in the ring, the market for robo advisers will likely experience significant growth.

미래에셋자산운용·KB자산운용·삼성증권 같은 한국의 주요 금융사들은 알고리즘 기반의 자산관리에 뛰어들고 있다. 그리고 대형사의 이러한 움직임은 로보어드바이저 업계 전반의 성장으로 이어질 것으로 보인다.

The three firms earlier this year either launched robo adviser-driven funds or applied to participate in a test system run by the Financial Services Commission.

세 회사는 올 초에 로보어드바이저 펀드를 출시하거나 금융위에서 진행하는 테스트 시스템에 참여했다.

In the United States, small automated investment service firms like Betterment and Wealthfront were the kindling that drove the industry’s early-stage growth in the 2000s, but it was the entry of industry giants like Charles Schwab, Fidelity and Vanguard that contributed to increased access to robo advisers, and now these big players dominate the market.

미국의 경우 작은 규모의 로보어드바이저 전문회사인 베터먼트와 웰스프론트가 초기 성장을 주도했다. 이어 찰스슈왑·피델리티·뱅가드 같은 대형사들이 들어오면서 로보어드바이저 대중화가 급속하게 이뤄졌고, 지금은 이들이 시장을 주도하고 있다.

The amount of assets under management by robo advisers in the United States is now $224.8 billion, according to market tracker Statista, with an annual growth projection of 47.5 percent through 2021.

통계 전문 사이트 ‘스태티스타’에 따르면 미국 내에 로보어드바이저가 운용하는 자산은 약 2248억 달러 규모이며 2021년까지 연평균 47.5%씩 성장할 것으로 예상된다.

Many of them focus on a diversified mix of exchange-traded funds at different risk levels.

많은 로보어드바이저 펀드는 리스크에 따라 다양한 상장지수펀드(ETF)를 포함해서 포트폴리오를 짠다.

Despite the promise, firms complain strong regulations are hampering the industry’s growth.

한편, 로보어드바이저가 가진 가능성에도 불구하고 강한 규제가 업계의 성장을 가로막고 있다는 지적도 있다.

Presently, automated investment cannot be done completely online since clients still have to visit the offices of securities companies and speak face-to-face with fund managers for the initial sign-up.

현재는 고객들이 로보어드바이저 펀드에 가입하기 위해 창구나 증권사에 직접 가서 펀드매니저들의 설명을 들어야 한다. 자동화된 투자라고 해도 완전한 비대면 거래는 불가능한 것이다.

Lee Seung-jun of Quarterback Investments argues that the rule prevents service providers from significantly lowering their fees since human guidance requires cost.

쿼터백인베스트먼트의 이승준 이사는 비대면 일임을 허용하지 않는 규제 때문에 인력에 대한 비용을 지불하는 것이 불가피하고, 비용을 줄여 수수료를 낮추는 것이 어렵다고 주장했다.

“We can’t charge the same commission rates as in the U.S. because we are not allowed to reduce costs through digitization,” he said.

“우리는 디지털화를 통해 비용을 줄이는 구조가 가능하지 않는 상태이기 때문에 미국 수준으로 수수료를 줄일 수 없다”고 그는 말했다.

Lee declined to specify how much commission his company charged, though he said it was “in line with or slightly lower than existing asset management firms.”

이 이사는 쿼터백자산운용 펀드의 평균 수수료를 밝히지는 않았지만 수수료가 “기존 자산운용사와 비슷하거나 조금 낮은 수준”이라고 말했다.

Fees at Korea’s 12 robo adviser funds range from 0.6 to 1.3 percent, according to the Korea Financial Investment Association.

금융투자협회에 따르면 국내 12개 로보어드바이저 펀드의 수수료는 0.6~1.3% 수준이다.

A source at the Financial Services Commission said the government agency wants to foster the robo adviser market but hasn’t decided whether to lift the regulation requiring human advisers.

금융위 관계자는 금융위가 로보어드바이저를 더욱 활성화할 방침이지만 비대면 일임 금지 규정을 없애는 방안에 대해서는 결정된 것이 없다고 말했다.

“The Financial Services Commission acknowledges that non-face-to-face transactions are an irreversible trend,” the source said.

이 관계자는 “금융위는 비대면 거래가 피할 수 없는 추세라는 점을 인지하고 있다”고 말했다.

Limits of the robotic touch

로봇 금융투자의 한계

Financial authorities aren’t the only ones cautious about automated wealth management.

금융 당국만 자동화된 자산운용 서비스에 조심스러운 것은 아니다.

Investors are, too, as reflected by the modest size of assets handled by robo advisers in Korea.

시장 규모에서 확인할 수 있듯, 한국 투자자들의 이에 대한 확신도 크지는 않다.

The lack of reliability and impressive returns has been considered a weak point for the technology.

낮은 신뢰도와 낮은 수익률 등이 대표적인 약점이다.

Last month, the country’s robo funds only made an average 0.86 percent return on investment, according to the Korea Financial Investment Association.

금융투자협회에 따르면 지난달 로보어드바이저는 평균 0.86%의 수익을 기록했다.

But analysts like to point to more fundamental downsides of machine-led investment, namely the lack of human touch and inability to comprehend diverse goals at different stages of life.

뿐만 아니라 일부 전문가들은 기계에 의한 투자가 보다 근본적인 한계를 갖고 있다고 주장한다. 바로 인간미가 부족하다는 점이다. 그리고 생애 주기에 따른 다양한 목표를 이해하고 포트폴리오에 반영할 수 있는 능력을 갖추지 못했다.

“Robo advisers are unable to provide more diverse and multilayered financial consulting such as retirement plans and predicting the value of asset prices in the future,” said Seo Bo-ick, a researcher at Eugene Investment & Securities.

유진투자증권의 서보익 연구원은 “로보어드바이저는 은퇴 계획, 미래 자산가치 전망 같은 보다 다양하고 복잡한 금융 컨설팅을 제공하지 못한다”고 말했다.

In a survey of 2,530 people in January, 34 percent of respondents said they were not willing to use robo advisers, according to the Korea Financial Investors Protection Foundation, a consumer rights group.

실제 올해 초 한국금융투자자보호재단이 발표한 설문조사 결과에 따르면 응답자 2530명 중 34.0%는 로보어드바이저를 이용할 의향이 없다고 답했다.

Only 18.9 percent said that they would consult with a robot, while the remaining 41 percent remained neutral.

이용할 생각이 있다고 답한 비율은 18.9%에 불과했고, 나머지 41%는 중립이라고 답했다.

The skeptics cited reliability as the biggest factor for foregoing the new technology.

부정적인 답변을 한 응답자들은 그 이유로 낮은 신뢰도를 꼽았다.

They argued that human needs are too complex for a simple paint-by-number approach that most robo advisers right now can provide.

인간의 필요는 로보어드바이저가 숫자를 기반으로 제공하는 분석으로 해결하기엔 너무 복잡한 것이라고 그들은 주장한다.

This is precisely why firms in the United States that specialize in robo advising still complement their automated investment services with human consultations.

이는 미국의 로보어드바이저 전문회사들이 왜 자동화 서비스를 인간의 자문을 이용해 보완하고 있는지를 설명해 준다.

Betterment, for example, has two additional tiers of service that provide regular advice from financial planning experts.

예를 들어 베터먼트는 금융전문가의 상담을 제공하는 두 가지 옵션을 추가했다.

Other analysts see risk in robo adivsers’ susceptibility to technical glitches and hacks.

일부 애널리스트들은 로보어드바이저의 기술적 결함 가능성이나 해킹에 대한 위험을 지적하기도 한다.

“There is also no clear legal protection for those affected by cases where robo advisers don’t perform as intended,” said Lee Hyo-seob, a researcher at the Korea Capital Market Institute.

자본시장연구원의 이효섭 연구원은 “아직은 로보어드바이저가 의도한 대로 움직이지 않을 때 피해를 입은 투자자들을 위한 어떠한 법적 보호도 정립되어 있지 않다”고 말했다.

The Financial Services Commission and industry players have played down the negatives, saying test bed platforms are designed to filter out any underperforming algorithms.

하지만 금융위와 업계 관계자들은 정부의 테스트 베드 플랫폼이 기준에 못 미치는 알고리즘을 걸러내도록 만들어졌다며 우려를 일축했다.

Concerns about mass layoffs, especially of human financial advisers, will also likely get in the way of widespread adoption of robo advisers in Korea.

또 펀드매니저들이 대량 해고될 수 있다는 우려도 한국에서 로보어드바이저가 확산하는데 장애가 될 수 있다.

There’s precedent for such concerns: BlackRock, the world’s largest fund management company, has removed at least seven portfolio managers from their current assignments, and the Royal Bank of Scotland said it plans to replace 220 investment staff members with robo advisors.

이 같은 우려는 이미 외국에서 현실화됐다. 세계 최대 운용사인 블랙록은 이미 최소 7명의 주식포트폴리오 매니저들을 해고했고, 스코틀랜드 왕립은행은 220명의 투자 인력을 로보 어드바이저로 대체하겠다고 밝혔다.

In Korea, the number of employees in the securities industry has been on a constant decline since 2011, falling 19 percent to 35,699 as of the end of last year, and observers predict the broader application of automated investment services will exacerbate the trend.

한국에서는 2011년부터 증권가 인력이 계속해서 줄어들고 있다. 증권사 직원 수는 지난해 말 기준으로 3만5699명으로 전년 대비 19% 줄었다. 전문가들은 자동화된 투자 서비스가 대중되면 이 같은 추세는 더욱 심해질 것으로 전망했다.

Crunching the numbers

경쟁력 줄어드는 금융 애널리스트

Asset managers are not alone in potentially losing their jobs to digital equivalents — financial analysts are feeling threatened by analytical software capable of parsing through large amounts of data in a matter of minutes.

운용사 직원만 로봇들에게 자리를 뺏기고 있는 것이 아니다. 금융 애널리스트들도 거대한 데이터를 몇 분만에 정리하고 분석할 수 있는 분석 소프트웨어의 등장에 위협받고 있다.

Let’s take the impact of North Korea’s missile tests on the financial markets as an example.

북한의 미사일 실험이 금융에 미치는 영향을 예로 들어보자.

If one wants to calculate the exact numeric correlation between North Korea’s posturing and changes on the Kospi, currencies, bonds and commodities over the past 30 years, it would take at least several days or even weeks, a process that would require a combination of Bloomberg codes, Google searches and Excel spreadsheets.

만야 어떤 사람이 지난 30년간 북한의 미사일 실험과 코스피, 환율, 채권 간의 상관관계 수치를 구하려고 한다면 최소 며칠 또는 몇 주가 걸린다. 블룸버그 코드를 찾고 구글을 검색하고, 엑셀 작업을 하는 과정도 필요하다.

An algorithm could do the work in about five minutes.

하지만 알고리즘은 그 작업을 5분 만에 끝낼 수 있다.

There are many start-ups developing this type of analytical software — one of the biggest is Kensho, which has received investment from Goldman Sachs.

금융 분석 소프트웨어를 만드는 많은 스타트업이 생겨나고 있다. 그 중 가장 눈에 띄는 업체는 바로 골드만삭스에서 투자를 받은 ‘켄쇼’다.

The U.S.-based start-up’s flagship platform, Warren (named after Warren Buffett), can instantly answer millions of complex financial questions and even create sophisticated financial models.

켄쇼의 대표 플랫폼인 ‘워렌’은 수백만 가지 복잡한 금융 관련 질문에 바로 답할 수 있고 정교한 금융 모델까지 만들어 낸다.

Koscom, a Korean government-run financial IT solutions company, envisions a landscape where market participants and the public can access such platforms.

코스콤은 시장과 대중 모두 워렌과 같은 플랫폼에서 정보를 얻게 하겠다는 비전을 갖고 있다.

It announced earlier this year that it is working on a financial market analysis system based on artificial intelligence. It hopes to begin by providing analytical reports on certain stocks written by robots.

올해 초 코스콤은 인공지능에 기반한 시장 분석 시스템을 개발하고 있으며 로봇이 작성하는 주가 리포트 서비스 제공을 시작할 예정이라고 밝혔다.

Another Korean company, Uberple, hopes to be the native answer to Kensho.

또 다른 한국 회사인 ‘위버플’은 한국의 켄쇼를 지향한다.

Founded in 2013, the Seoul-based start-up built a platform called Snek that can analyze various data sets including news articles, analyst reports, corporate electronic disclosures and government announcements.

2013년 설립된 위버플은 ‘스넥’이라는 플랫폼을 개발했다. 스넥은 정부 발표, 공시, 애널리스트 리포트, 기사 등을 통합해 분석한 내용을 제공한다.

The company plans to install a search engine called DeepSearch to perform keyword-based queries.

위버플은 스넥에 딥서치라는 키워드 기반의 검색 엔진을 탑재할 예정이다.

“Current financial analysis offers limited perspectives,” said Joo Eun-hwan, a manager at Uberple. “But we try to provide broader, user-oriented data analysis that allows investors to find a correlation between certain events and financial market movements using the quants.”

위버플의 주은환 매니저는 “현재 금융 분석은 제한된 시각을 제공하지만 위버플은 이용자 중심의 더 광범위한 분석을 제공하고자 노력한다”며 “투자자들이 특정 사건과 금융시장의 변동 사이의 상관관계를 도출할 수 있도록 한다”고 말했다.

박은지 기자 PARK EUN-JEE [park.eunjee@joonang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)