Weak dollar boosts foreign currency insurance

Foreign currency deposits have long been considered the top investment choice when the value of the U.S. dollar drops in comparison to the Korean won. A large amount of capital is often moved around to take advantage of a drop in the dollar by putting money into foreign currency deposits as they guarantee a certain level of interest as well as future profit by changing it back to Korean won when the dollar value goes back up.

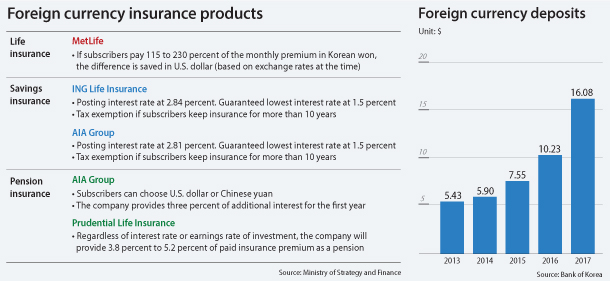

According to data by the Bank of Korea, the total amount of money in individual foreign currency deposits in Korea as of December last year stood at 16.08 billion won ($14.95 million), up nearly 6 billion won compared to a year earlier.

Foreign currency insurance works in a similar manner but instead of putting money into a deposit account, subscribers pay an insurance premium with foreign currency, such as U.S. dollars, and receive payments with the same currency. Interest rates on the policies are often higher than the one percent guaranteed for foreign currency deposits.

Some policies are created in the form of universal life insurance, which means subscribers can choose to put in more money than the original amount they are obliged to pay.

The additional funds are credited to the value of the policy with a certain level of interest. Subscribers can also withdraw cash out of the policy account, making it work similarly to a regular deposit account.

While most foreign currency insurance was in the form of savings insurance or pension insurance, companies are expanding the scope and rolling out life insurance.

MetLife, for instance, recently introduced “MetLife Universal Dollar Life Insurance,” the first life insurance that is traded in U.S. dollars. The company lowered policy fees by 15 to 20 percent compared to the industry average. It gives a 3.5 percent interest rate per year to subscribers.

One notable option that MetLife added to the product is allowing subscribers to pay a monthly premium at 115 to 230 percent of the policy rate in Korean won. The option works as a safeguard since the premium that Korean subscribers would have to pay in won will change each month due to fluctuations in the exchange rate. The company exchanges the total premium paid by the subscriber in Korean won to U.S. dollars in accordance with the exchange rate at the time and credits the excess to the value of the policy.

Industry insiders, however, recommend buyers are cautious when they subscribe to life insurance policies.

Some policies currently available give subscribers a choice between the U.S. dollar and Chinese yuan while others guarantee a certain level of return as a pension regardless of the investment earnings rate.

“Dollar [based] insurance is an ideal option to make long term investment as it diversifies currencies [in the portfolio],” said Jeong Sun-mi, a director at the WM Advisory Center at Woori Bank.

BY HA HYUN-OCK [choi.hyungjo@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)