A delinquent payment can stay on your record for five years.

It was great news for Korea and underscores the country’s stability as it emerges from the global economic slump.

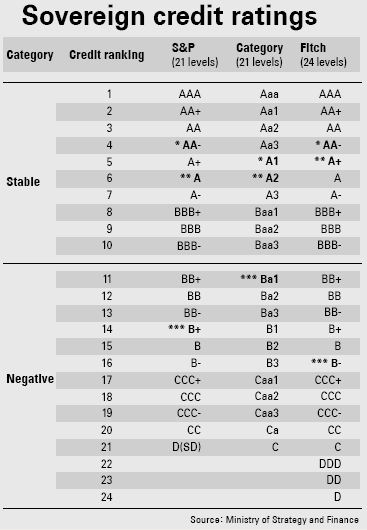

But what the heck does it actually mean? A credit rating for a country, much like one for an individual, is an official evaluation of its overall ability to repay loans, which is key for attracting investments used to fund government projects.

The leaders of the credit-rating world - a triumvirate consisting of Fitch Ratings, Moody’s and Standard & Poor’s - each use a slightly different method to rank credit worthiness, relying on letters combined with numbers or positive and negative signs.

*Korea’s rating before the Asian financial crisis

**Korea’s present rating

***Korea’s lowest rating during the Asian financial crisis

A nation’s credit rating can also differ depending on the currency it uses to pay the loans. For example, Korea’s rating based on the won is AAA, which means that there is almost no chance that the local government will not be able to pay off loans with won. Most of Korea’s private banks have AAA grades. However, Korea and its banks have a much lower credit rating based on the U.S. dollar. That’s because the amount of U.S. dollars that the government and local banks have is limited, and there is a chance that they might not be able to pay up on time - which is exactly what happened after the Asian financial crisis in 1998.

It’s rather difficult for countries that have seen their sovereign credit ratings decline to get them back up. But Korea managed to do just that in only nine months when it came to the Fitch rating. Last November, Fitch lowered Korea’s credit rating from stable to negative as the global economic downturn set in. In July, however, the agency launched a three-day field review of Korea. It then decided to upgrade its rating based on the government’s efforts to overcome the current economic crisis, improvements in the country’s macroeconomic data and an increase in foreign currency liquidity.

Currently, Korea has the sixth-highest credit rating offered by S&P and Moody’s and the fifth-highest offered by Fitch - lower than the ratings it had before the Asian financial crisis. One of the main reasons that Korea has not been able to recover fully since then is that the country still gets a bad rap from the crisis. Thus, the past is very important when it comes to a country’s credit rating.

The sovereign credit rating system has its flaws, though. On May 2002, Moody’s lowered Japan’s sovereign credit rating two levels - from a AA3 to an A2 - in one fell swoop, citing the country’s “serious” financial deficit.

As a result, Japan’s rating was lower than the one given to the Republic of Botswana in Africa, where half of the land is desert and one-third of the economy is based on mining.

Moody’s kept Japan’s credit rating at that level until 2007. But it only moved the rating up by one notch, to A1, which simply put it in the same tier as Botswana.

Aside from country credit ratings, there are personal credit ratings as well. Individual credit scores aim to show a person’s ability to pay off loans on time, which companies consider key when deciding whether to loan people money and at what rates they will do so.

Personal credit ratings can differ slightly depending on the credit bureau behind the evaluation. Credit bureaus typically use a 1,000-point system as a base for assessing individual credit worthiness. They then rank individuals using a scale of one (lowest) to 10 (highest). If you get a loan and pay it off on time, your score - and thus your rating - goes up. If you’re delinquent, it falls.

For the most part, if a person has no particular record of receiving or paying back a loan, he or she receives a six. Those with ratings of seven or lower are deemed “speculative,” making it extremely hard for them to receive loans.

However, your credit rating can change, albeit slightly, if you are a customer of a bank for a prolonged period of time and have a good history with the firm.

But there are some misconceptions when it comes to personal credit ratings. One important aspect to note is that deciding to forgo loans and credit cards won’t help your rating, which is somewhat counterintuitive. Your rating can only really move up if you actually borrow money and make purchases on credit cards and then pay them off on time.

Another misconception is that your credit rating will rise if you have more money in the bank. Although an individual bank might take that into account, credit bureaus don’t have access to that information and therefore won’t include it in an assessment of your credit risk. The only information a credit bureau is concerned with is your payment history.

Missing a payment isn’t the end of the world, and we all do it from time to time.

But a delinquency can stay on your record for up to five years after you’ve settled it. So the best remedy in that case is time.

The average credit rating for a male in Korea between the ages of 30 and 59 is four, while the average for women in this age group is three, according to Korea Information Service.

The most important thing to remember when it comes to personal credit is to pay your bills on time. If you delay making a payment for just five days, the delinquency will go on your record at credit bureaus. If you wait three months or longer, your name will be listed in the Korea Federation of Banks as “a person who made a default on a loan.”

Now what if you already have a bad credit rating?

All hope is not lost. But, again, it’s going to take time. Financial experts recommend clearing up all your debts and resuming financial activity to prove that you are now reliable.

By Cho Jae-eun, Kim Won-bae [jainnie@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)