[Sustainable Future] A little less sulfur, a little more profit, please

For oil refiners and ship makers, the new standard could offer the performance boost both industries desperately need. The opportunity is all the more important as these are markets where global regulatory disruption is virtually unheard of.

High-sulfur fuel oil, or bunker fuel, has been the most widely used marine fuel since the 1960s, thanks to its low price. The new sulfur limit will cut that demand by 60 percent within a year, the International Maritime Organization (IMO) - the United Nations agency responsible for the new regulation, known as IMO 2020 - predicted in a March forecast.

“Never in world history has a widely commercialized fuel seen global demand nearly halve in such a short time span - this is why IMO 2020 is seen as a historically meaningful event that will shake things up in not only the refinery market, but also the crude oil market,” said Korea Investment & Securities analyst Daniel Lee.

Opportunity for refiners

The alternatives for high-sulfur fuel oil are low-sulfur fuel oil (LSFO), which is desulfurized bunker fuel, and marine gas oil, the equivalent of diesel for ships. Local analysts have suggested the increase in demand for the two low-sulfur options poses a serious opportunity for Korean oil refiners.

The opportunity couldn’t have come at a better time - oil refiner performance has been suffering this year due to low refining margins - the difference in value between the products produced and the value of the crude oil used.

The average price of fuel produced by refiners during this year’s first half plummeted to as low as $2 per barrel - $4.50 per barrel is considered the break-even point for local oil refiners.

The IMO’s new regulation going into effect is generally expected to increase the average profit margin led by the demand hike for diesel. Diesel not only serves as a low-sulfur fuel itself, but is also mixed with bunker fuel to pull down its sulfur content. In fact, refining margins for the year’s second half have already shown a significant increase. From July, refining margins have largely stayed above $6.0 per barrel.

Mirae Asset Daewoo analyst Park Yeon-ju said stockpiling of low-sulfur fuel oil will gain more traction in the next two months as it is taking longer for shipping lines to install scrubbers - a device that allows shipping lines to use regular bunker fuel by removing sulfur from emissions.

“We believe shipping lines will have no choice but to use LSFO,” she said.

Analysts say the upward trend will continue throughout the rest of this year as the regulatory change approaches, thanks to an anticipated margin increase for diesel, which already contains less sulfur. At the same time, the margins for bunker fuel will inevitably decline.

The widening gap between high-sulfur and low-sulfur fuel could be an opportunity for Korean oil refiners who already have a smaller share of the bunker fuel market compared to other Asian competitors.

S-Oil's residue hydrodesulfurization unit in Ulsan, part of the company’s 5-trillion-won ($4.2-billion) facility expansion completed last November. The unit removes impurities like sulfur from residue oil so that it can be used to produce high-value petrochemical products afterwards. [S-OIL]

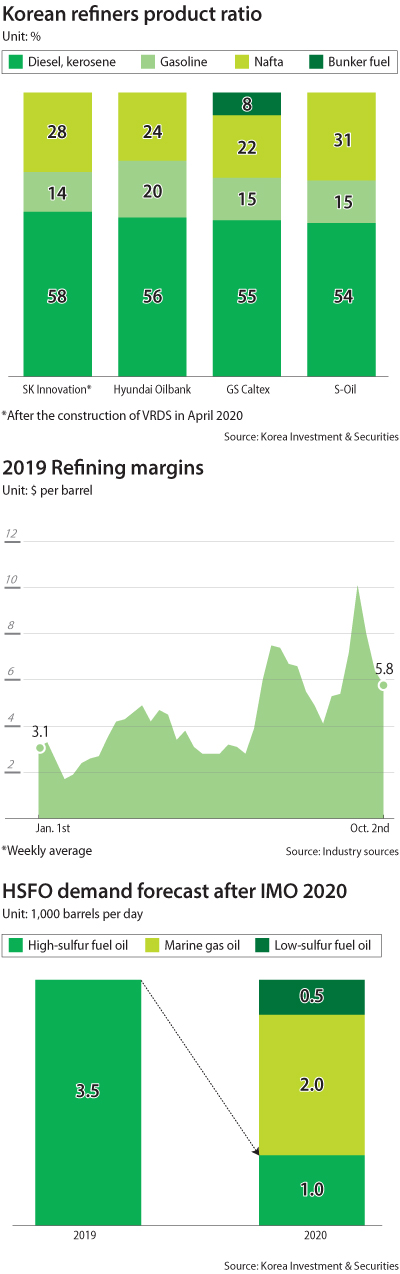

“From this perspective, Korea’s four oil refiners all hold advantages,” he added, referring to SK Innovation, S-Oil, Hyundai Oilbank and GS Caltex.

Over the past few years, local companies have actively moved away from bunker fuel production, concentrating instead on installing equipment that can convert the high-sulfur fuel to low-sulfur products or chemical materials.

This means that not only can they start producing low-sulfur marine fuel on a large scale, but when high-sulfur fuel prices plummet, those refiners will be ready to buy up the cheap bunker fuel and convert it to more popular products at a higher margin.

Last year, S-Oil completed a 5-trillion-won project to construct a petrochemical complex that can convert bunker fuel into gasoline, propylene and other chemical products - which the company anticipates will lower high-sulfur fuel oil’s production share by more than 70 percent. It is also investing in facilities to desulfurize bunker fuel, which it plans to have in stable operation from early 2021.

“Bunker fuel is a natural byproduct in the oil refining process - you can’t completely rule it out. But the only usage today is in ships, and because of IMO 2020, refiners are driving efforts to minimize it because it’s no longer profitable,” said a local industry source.

SK Innovation is building a vacuum residue desulfurization plant in Ulsan, capable of desulfurizing bunker fuel to produce low-sulfur fuel and diesel, due for completion next April. It is also the only local refiner that does business in off-shore oil blending - another way to produce low-sulfur fuel. The company plans to expand the business by fourfold next year.

Hyundai Oilbank installed solvent deasphalting equipment in its plants last year, which eliminates asphalts from bunker fuel and thus increases the extracted volume of gasoline and diesel. It also announced Monday that it will start selling low-sulfur fuel oil with a sulfur content of less than 0.5 percent starting next month.

China’s so-called teapot refiners - which were responsible for the oversupply that crashed refining margins a few years ago - Japanese and Indonesian refiners are relatively unprepared for the downfall of bunker fuel. Asian refiners’ average ratio of bunker fuel production is around 25 percent, whereas for local refiners, the figure is closer to zero, according to Lee.

However, some analysts are pessimistic about IMO 2020’s effect on diesel demand, claiming there’s a “valuation bubble” involved.

In a report published earlier this month, SK Securities said the impact on diesel prices will be minimal. “The idea that the ship industry alone can shake grounds for the entire diesel market is absurd,” commented SK’s oil analyst Sohn Ji-woo.

Marine fuel accounts for 5 percent of the entire fuel market - not a significant enough share to seriously disrupt diesel prices, the report says, especially considering diesel demand in cars. Passenger cars eat up 27 percent of fuel demand, but diesel demand has been falling since the so-called dieselgate in 2015, when German carmaker Volkswagen was found to have internally faked diesel emissions test results for its vehicles.

SK Innovation’s ship pumps fuel into a crude oil carrier for offshore oil blending, which is one method of creating low-sulfur fuel oil. [SK INNOVATION]

The tighter sulfur cap comes mostly as good news for shipbuilders that have been seriously struggling with an order drought over the last decade.

When the industry first started preparing for the regulatory change, expectations were high that shipping lines would use the sulfur cap as an opportunity to scrap old, less efficient ships in favor of greener and more efficient ones.

In practice, that hasn’t really happened. The market has not seen a dramatic boost in demand yet, as shipowners are still deciding how to adapt to the new rules.

“As it is a huge investment to make, it is not easy to make a bold choice for shipping lines, and they are still watching each others’ moves,” a source from the shipping industry said.

Analyst Lee Bong-jin from Hanwha Investment & Securities wrote in a report last month that orders for new ships in response to the new sulfur regulations would have been placed in the past three years.

“Considering it takes roughly two years to build a ship ... I think it would be correct to say new orders spurred by the sulfur cap have already been placed,” Lee said. “According to Clarksons Research, though, the increasing portion of orders placed this year are for ships using non-heavy fuel oil or dual fuels. Shipowners have already started to prepare for environmental regulations to take effect after 2025.”

Apart from the 2020 sulfur regulations, the IMO is also pursuing a rule to cut carbon dioxide emissions by at least 40 percent from 2008 emissions levels by 2030.

According to shipping market tracker Clarksons Research in June, orders for a total of 27 LNG carriers have been placed in the first half of this year, and nearly 80 percent of those orders went to Korea’s three large shipbuilders.

If demand for LNG-powered ships increase, it is likely that Korean players will be the major beneficiaries.

“It is hard to predict exactly how much demand the IMO regulation will create because shipowners consider various other factors like finances, shipping rates and the age of ships before making new orders,” said Hwang See-cheul, a senior officer and head of the LNG carrier sales department at Hyundai Heavy Industries.

“But among the commercial ships we are building, 85 percent have adopted scrubbers or LNG-powered engines or are at least designed with LNG-ready option, which enables ships to be retrofitted to LNG-powered ships in the future.”

In the meantime, all three carriers are developing technology to make LNG-powered ships more efficient and affordable - the greener ships currently cost around 20 percent more than fuel oil-powered ships.

“Our focus now is to develop ships that can make shipowners comply with the tightening regulations but at the same time are affordable for them,” a spokesperson from Samsung Heavy Industries said.

While scrubber makers are the major beneficiaries of the to-be-implemented sulfur cap, they are already preparing for cleaning systems that can reduce other pollutants including nitrogen oxide and carbon dioxide.

“Until recently, scrubber makers have been the major beneficiaries of the IMO 2020 regulation,” said Yoon Young-jin, a team leader in the scrubber department at Hyundai Power Systems, a scrubber making arm under Hyundai Heavy Industries Group.

“However, due to controversies on the effect of wash water discharged to seas from scrubbers and regulations imposed by individual governments, there may be limitations on increasing scrubber installation. Scrubber makers have already begun investing in systems to clean up other pollutants apart from sulfur oxide.”

Realistic expectations

Despite the broadly rosy outlook, there are pessimists that say the IMO 2020 hype in Korea is getting excessive.

“Looking back at previous IMO regulations, which actually have no legal force, it’s questionable whether [the sulfur limit] will actually be followed this time,” SK Securities said in a report this month.

A fundamental question lies in the IMO’s authority to enforce regulations. The International Maritime Organization is an inter-governmental body under the United Nations with 174 member countries. The legal binding force of the IMO’s industry rules depends on the member states’ voluntary decision to incorporate the rules into their own respective laws.

And despite the global consensus in support of the green initiative, governments cannot completely ignore the expected hardship for the shipping industry. Earlier this year, U.S. President Donald Trump made attempts to delay compliance. Indonesia asked for more time to meet new requirements, although it quickly withdrew that request.

The IMO has postponed implementation of maritime regulations before, bending to the requests of members and companies that appealed due to the cost burden and infrastructure shortage.

Its latest example was the regulation on ballast water that was supposed to oblige ships to install management systems to clear wash water before pumping it into the sea. Its implementation was delayed from 2022 to 2024 after complaints from shipping lines that owned old vessels.

IMO head Lim Ki-tack admitted at a conference earlier this month that difficulties may lie ahead due to low-sulfur fuel availability. “There might be some challenges” for shipping companies active in north-to-south trade, he said.

But on its official website, the IMO gives a downright “no” to whether the deadline can be changed, saying the matter should have been finalized six months ahead of adoption. The entire process to make that change takes 22 months. In other words, there is no time left.

BY SONG KYOUNG-SON AND KIM JEE-HEE [song.kyoungson@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)