Samsung reveals secrets behind retirement riches

In Korea, facing retirement is a daunting task. From the lowliest salaryman to senior managers, many workers fret about how to make ends meet in later life amid a rapidly aging and increasingly expensive society. But recently, top investment experts at Samsung Securities have attempted to dispel these fears by authoring a confidential how-to booklet of investment tips for retiring Samsung Group executives.

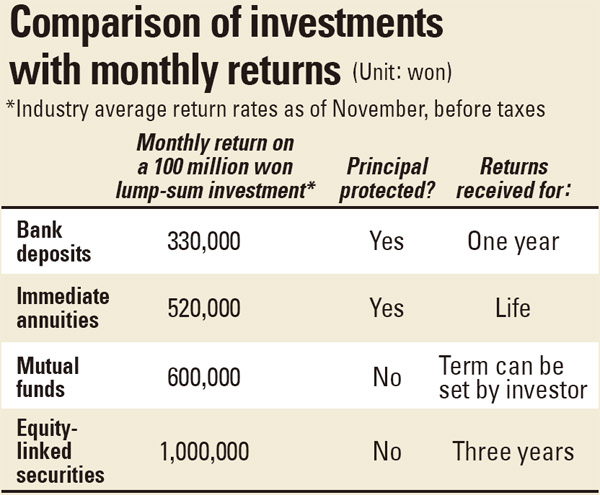

Samsung Securities reportedly planned to distribute the booklets among some 400 retiring executives this week. In the booklet, experts downplay the benefits of mutual funds, bank deposits and even equity-linked securities for generating the optimum monthly income.

This is an insurance product where the policyholder invests a lump sum in return for a guaranteed periodical income.

Because the monthly payment consists of a chunk of the principal together with investment returns, immediate annuities provide for a higher monthly “paycheck” than interest from regular deposit accounts.

According to Samsung Securities data, a 100 million won ($87,000) investment in an immediate annuity policy would yield 520,000 won each month on average upon retirement as of November this year. In contrast, interest payments from a time deposit account would only yield 330,000 won.

Moreover, as central banks in Korea and abroad maintain low interest rates, experts say keeping your money in a bank account in such low-interest conditions could result in losses when taking taxes and inflation into account.

“You should prepare for the era of low-interest rates by investing in long-term treasury bonds that mature in 10 years or more,” the booklet instructs. “In order to fend off inflation, which can chip away at the value of your assets, consider treasury inflation-protected securities (TIPS).”

Korean government bonds that mature in 19 years reported yields of 4.7 percent per annum last week, higher than the average interest rate of banks’ time deposit accounts, which were in the upper 3 percent range.

Concerning the recent popularity of rentable properties as retirement investments, Samsung Securities’ experts advised caution in investing in shopping districts in newly developed areas such as Pangyo-dong in Bundang or Gwanggyo in Suwon, both in Gyeonggi, because of their expensive price tags and uncertain market conditions.

“The college belt that stretches from Hongik University through Sinchon to Ewha Womans University is worthy of attention,” experts wrote.

They also urged executives to consider an individual retirement account (IRA). These are products sold by banks, insurance companies and securities firms that are backed by the government in the form of tax breaks.

When retirees transfer severance pay to one of these individual retirement accounts, they can reclaim the tax paid on their retirement income - and take it out later when they use their retirement funds. This gives the retiree more seed money during the period when the tax payment is delayed, and any returns the retiree gains in the meantime are tax free. However, retirees must hurry to sign up for an IRA account, as they only have 60 days to do so once leaving their jobs.

By Lee Jung-yoon [joyce@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)