Risks remain after Lone Star goes

Overcoming M&A risks

Having begun as a merchant bank in 1971, then building up by acquiring now-defunct banks such as Seoul Bank, Hana Financial Group served as a distant fourth among Korea’s top commercial banking groups in asset size, number of branches and the size of its workforce.

But after swallowing KEB, Hana Financial is set to become the second-largest banking group in the country with 285 trillion won ($254.5 billion) in assets as of Sept. 2011. It will also maintain the largest network of foreign branches among domestic banking groups, with a local presence in 22 countries.

This is set to transform the landscape of Korea’s financial industry, as Hana Financial will be able to draw on Hana Bank’s strength in marketing to the wealthy, and KEB’s fortes of corporate banking and trade finance.

In the credit card sector, a potential merging of latecomer Hana SK Card and KEB’s card business would increase Hana Financial Group’s market share in Korea’s plastic payment from 5 percent to 9 percent, putting it ahead of Lotte Card and Woori Bank’s card business (both 8 percent) to rank fifth behind Shinhan Card’s 23 percent, KB Kookmin Card’s 14 percent and the 11 percent to 12 percent market shares of Samsung Card and Hyundai Card, respectively.

But while Hana may have received a stamp of approval to acquire KEB, the vitriolic opposition registered by the bank’s union, as well as attempts to further politicize the issue before this year’s elections, could prove crippling.

Immediately after regulators’ approved the deal on Friday, KEB’s union began preliminary preparations for a strike by submitting an application for mediation of a labor dispute to the National Labor Relations Commission. It vowed that “all employees will fight [the acquisition] until the end.”

To appease the workforce, Hana Financial has said they will face no immediate restructuring. It also said earlier that a “two-bank” system would be put in place in the near future, with Hana Bank and KEB kept as separate entities under the same holding company.

“An artificial restructuring of the workforce is not being considered,” said Hana Financial Group Chairman Kim Seung-yu on Friday. “We will engage in earnest talks [with KEB’s union.]”

However, observers said that the status quo cannot be sustained indefinitely. As of last September, the combined workforce of Hana Bank and KEB stood at 16,962, much more than Woori Bank or Shinhan Bank. M&A experts believe some of the fat will need to be shaved off to ensure the banks’ survival.

And while two banks can co-exist under one roof in Korea - Shinhan and Choheung managed to do so for two and a half years before merging in 2006 - “there is a limit to how much synergy can be achieved,” said an official at Shinhan Financial.

Taxing Lone Star

Meanwhile, Korea’s tax agency is preparing to mount one last skirmish against outgoing owner Lone Star, which has been demonized here for taking generous dividend payments on top of stock price returns while letting Korea Exchange Bank’s market share dwindle.

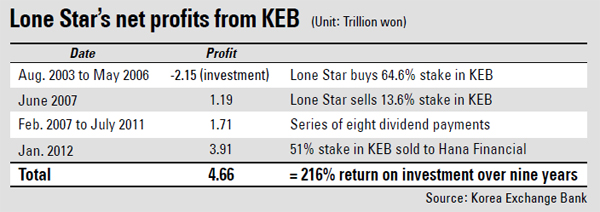

With Hana Financial about to hand over roughly 3.9 trillion won to acquire a 51 percent stake in KEB, the U.S. buyout fund is set to gain 6.8 trillion won through stake sales and dividend payments - more than three times its original 2.15 trillion won investment in buying a 64.6 percent stake in KEB. If profits from other investments are added, such as Star Tower in Yeoksam-dong, southern Seoul, Lone Star is set to walk away with about 5.4 trillion won.

Yet during Lone Star’s tenure as the controlling shareholder, KEB’s market share of total bank deposits shrank from 7 percent in September 2003 to 5.8 percent as of last September. Over the same period, the bank’s 5.9 percent share of total bank loans dwindled to 5.2 percent.

Against this background, the National Tax Service (NTS) is preparing to tax Lone Star’s gains in a “strict and fair manner,” according to an official from the agency.

The NTS is said to be reviewing the viability of withholding income tax and the stiffer corporate tax, although for the latter, proving that Lone Star had an established business in Korea would be difficult because it collapsed its Korean unit back in 2008. Experts said that Lone Star is likely to be taxed between 300 billion won and 400 billion won.

As the tax agency and Lone Star continue to dispute the amount of tax due from the 1.19 trillion won block sale of KEB shares in June 2007, this is expected to be the last hurdle the U.S. fund must clear before exiting the country.

Legal revisions

Regulators are now free to change laws concerning bank ownership, which have proven the source of much controversy. Under local banking law, a “nonfinancial” player, or an entity that owns more than 2 trillion won of nonfinancial assets, cannot be the major shareholder of a bank. This made Lone Star’s ownership of more than 2 trillion won in nonfinancial assets as of the end of 2010 - through its affiliate in Japan - fodder for protest.

By Lee Jung-yoon [joyce@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)