Tough decision on mortgage rates

Noh, a 37-year-old salary worker, wants to buy an apartment, but he can’t decide how to finance it: Should he get a mortgage with a fixed or variable rate?

A loan with a fixed rate a little above 4 percent by the Korea Housing Finance Corporation sounded attractive. A set interest payment would be withdrawn from his bank account every month, making it easier to plan his financial management.

But variable rates, despite their fluctuations, are starting to seem as attractive or more so - and there are expectations that the central bank may further lower the benchmark borrowing rate later this year.

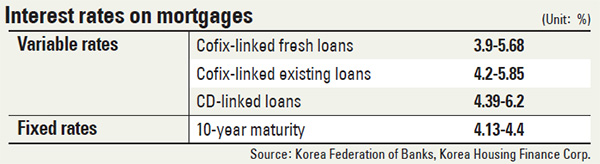

Since last month, commercial banks have been competing to lower their variable rates on mortgages. Variable rates have even fallen below 4 percent for the first time in two years. According to the banking industry, the Cofix rate - on which some variable rate mortgages are based - fell to 3.4 percent last month from 3.62 percent in June. This is far lower than the 3.75 percent rate in January.

As a result, KB Kookmin, the nation’s largest lender, has lowered its variable rate from 4.13 percent in July to 3.91 percent this month. The variable rates on mortgages offered by other banks also fell.

This trend was triggered by the central bank, which for the first time in three years loosened its monetary policy to combat the deepening economic slowdown in the global and domestic markets.

After the central bank lowered the benchmark rate, new fixed-rate loans also got cheaper after borrowers rushed to banks to take out loans with variable rates.

Last month, fixed-rate loans issued by the four commercial banks - KB Kookmin, Woori, Shinhan and Hana - fell 13 percent from the previous month to 2.6 trillion won.

However, analysts say a fixed rate is still more beneficial for borrowers, especially for long-term loans with a maturity of 10 years.

“Once the economy recovers, the interest rate will be raised in order to tame inflation,” said Kim Il-soo of KB Kookmin Bank’s PB center. “It is better to apply for a fixed rate to lower the risk from rising interest rates especially when taking out loans whose maturity exceeds 10 years.”

Variable rates can also rise up to five percent depending on the person’s credit status and borrowing conditions. The lower the credit rating of the loan applicant is, the higher the rates go, which pushes the rates far higher than fixed rates between 4.13 percent and 4.4 percent on a 10-year maturity loan.

Another strategy for people who expect long-term economic woes is to take a loan with a fixed rate for a certain period and then change to a variable rate.

Major banks offer a loan with a fixed rate for the first three to five years and then a variable rate.

But reading the fine print is necessary for all borrowers trying to get the best rate.

“Those who already have an existing loan need to be cautious since additional expenses may occur when canceling a loan contract on a fixed rate and then converting to a variable rate,” said Kim of Kookmin.

By Sohn Hae-yong [ojlee82@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)