Ratings for household debtors slide

Within the past five years, many debtors with midrange credit ratings have slid to the bottom tier and are barely able to pay their loans.

Younger debtors were shoved down to the lowest level faster than any other age groups as they continue to struggle to land jobs.

But debtors in the middle age group were at a higher risk than their younger or older counterparts and accounted for most of the people whose credit ratings have slipped.

Korea’s household debts, which have already passed the record level of 1,000 trillion won ($922.7 billion), is considered by many to be a ticking time bomb that could someday cripple the financial markets and derail the nation’s economic growth - especially if interest rates start to rise in the future.

According to the Bank of Korea yesterday, although the overall credit ratings situation in the country is improving, there is a credit divide in which debtors with better credit ratings are improving, whereas debtors in the middle and bottom ranges are in a deteriorating position.

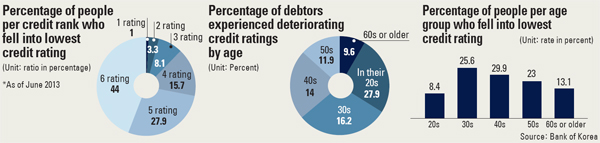

Korea’s credit ratings range from one to 10, with 10 being the worst.

The top four ranks saw their credit ratings improve - fewer people saw their credit ratings drop.

In 2009, the percentage of debtors in the top four ranks who had their credit ratings fall was 17.1 percent. Four years later, that figure eased to 13.8 percent. But debtors in the five and six tier had the worse time. Only 15 percent had a deterioration of their credit rating in 2009, which rose to 19.4 percent last year.

Debtors with rating of seven and below struggled to improve their credit ratings between 2009 and 2013. The credit ratings improvement rate in 2009 was 25.9 percent, but it fell to 25.2 percent last year.

What stands out the most, however, is that one out of four debtors in the midrange - with rankings of five and six - fell to the lower brackets of seven through 10.

In the top four ranks, 7.2 percent saw their credit ratings fall to the bottom four ranks.

The closer the ratings were to the lower bracket, the more likely the person was to tumble into the group. Among those who fell to the lowest four ratings, debtors with ranks five and six accounted for nearly 72 percent, whereas only 1 percent came from the top ranks.

Debtors with annual income less than 20 million won were more likely to see their ratings fall to the bottom, accounting for 21.4 percent.

This is a stark contrast to 7.5 percent for debtors with annual earnings of more than 60 million won.

It shows that debtors become more dependent on loans from nonbanking financial institutions with higher interest rates, which lowers their credit ratings while increasing the risk of defaults.

“It has been found that such a vicious cycle has only worsened debtors’ ability to pay back their debt and has only increased their overdue debts,” said Lee Jang-youn at the Bank of Korea’s macro economic analysis department. “The quality of debt has been getting worse at an alarming rate.”

By age, debtors in their 20s were the fastest to see their credit ratings drop to the lower levels followed by debtors in their 30s.

The biggest cause cited by the report was jobs. Among debtors in their 20s who saw their credit ratings fall to below seven, nearly 50 percent were jobless. The jobless included students and housewives. Those in their 60s came in second with 44.9 percent.

The report noted that if the economy falters or if the job market for youths fails to improve quickly, it will be much more difficult for both the young and the old to see their credit ratings improve.

Older debtors are particularly at risk. It turns out while only 8.4 percent of those whose credit ratings have been lowered were in their 20s, debtors in their 40s and 50s who are facing retirement accounted for more than half.

The report noted that the biggest risk for people who are 40 or older is securing a steady income.

While only 5 percent of debtors in their 20s and 12.8 percent of those in their 30s whose credit ratings deteriorated were self-employed, for the debtors in their 40s through 60s the figure was between 21 percent and 37 percent.

Many middle-aged debtors have loans from different institutions such as credit card companies, savings banks and insurance firms, which charge much higher interest rates than banks.

Debtors whose credits ratings were above six but are now seven or below saw their debts owed to banks (which charge lower interest rates) shrink from 57.7 percent to 28.5 percent in the past five years. During the same period, their borrowings from institutions with higher interests went up. Loans from credit card companies rose from 7.5 percent to 22.5 percent; loans from capital companies increased from 12.3 percent to 21.7 percent; loans from savings banks went up from 1.1 percent to 8.1 percent.

“Although the overall credit ratings situation is improving, there are signs that the younger generation and those that have trouble getting jobs are seeing their credit ratings fall,” said the central bank official.

“Once debtors with midrange credit ratings fall into the lower tiers, their access to bank loans becomes much more difficult and they will have no other choice but to borrow from nonbank institutions at higher interest rates.”

He said if the situation continues to worsen, it will not only affect financial institution’s soundness but also the government’s fiscal burden.

“It is necessary to look into all angles of policies to ease people’s credit ratings being lowered,” said Lee.

BY LEE HO-JEONG [ojlee82@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)