Options for lowering individuals’ tax bills

A major change in the 2015 tax reform plan is that, starting next year, there will be less of a tax benefit for people aged 20 to 59 who have been piling up money in fixed-term savings accounts.

They have been paying 9.5 percent in taxes on interest income of up to 10 million won ($9,502) a year. The rate will go up to 15.4 percent next year, and taxes on interest income are expected to increase as much as 18,000 won per person.

As of August, the total amount of money in such accounts at seven commercial banks - Kookmin Bank, Woori Bank, Shinhan Bank, Hana Bank, Nonghyup Bank, Korea Exchange Bank and Industrial Bank of Korea - stood at about 25 trillion won.

What can consumers do to reduce their tax liability? There are a handful of options.

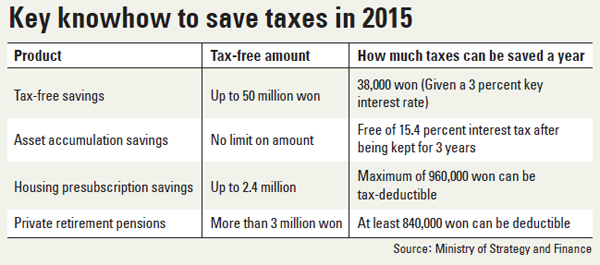

The most promising product is likely to be tax-free comprehensive savings products that will be launched next year for working-class people. They will be exempt from the 15.4 percent tax, providing tax-free savings of up to 50 million won a year.

At an interest rate of 3 percent annually, the tax savings would be 38,000 won.

However, the problem is that only people older than 60, those with physical disabilities and men of national merit are eligible for the tax-free accounts.

Because the eligibility age will be raised by a year annually over the next five years, people should apply for the tax-free products as soon as possible.

A more realistic choice will be government-led asset accumulation savings products. All financial institutions offer asset accumulation savings products with mandatory subscriptions that are tax free.

Long-term asset accumulation products were popular 10 years ago, then scrapped for a while. They were reinstated last year.

The number of newly opened asset accumulation savings accounts at the seven commercial banks stood at 8,077 in July and 7,634 in August, nearly double the figure in June.

From next year, the 10-year subscription period will be reduced to seven years to help consumers utilize their money more easily.

The government will also double the ceiling for tax deductible savings for housing pre-subscription products from 1.2 million won to 2.4 million won annually.

In addition, consumers could reduce their taxes by better use of pension plans.

From next year, the government will deduct 12 percent for private pension payments of up to 7 million won a year. Currently, the maximum deductible amount is 4 million won. Salaried employees will need to have separate private retirement pensions to take full advantage of the tax benefits.

If employees opt for severance pay on a monthly basis instead of lump-sum retirement allowances, the amount of retirement taxes would decrease 30 percent due to expanded deductions for retirees.

The ministry plans to expand the tax deduction ceiling on pension products from the current 4 million won to 7 million won to help the country’s aging population prepare for retirement.

Aggressive investors may consider investing in stocks. The biggest part of next year’s tax reform plan is to expand tax benefits for companies that raise employee wages or dividends.

Because of the policy, dividend stocks are gaining in popularity, too. The withholding tax rate for dividend income will be cut from the current 14 percent to 9 percent. Making investments directly into those stocks may produce higher returns than investing in funds, given the tax cut.

BY SONG SU-HYUN, MUN HEE-CHUL [ssh@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)