Taxman cometh on overseas fund profits

He’s making too much money.

The Korean investor earns an annual salary of 100 million won ($92,000). He invested 50 million won in February in a China fund. In just two months the profit has been more than 30 percent.

Thanks to the investment, he has made 15 million won in profit. That makes him subject to the financial income comprehensive tax because he also has investments in other financial products such as deposit and equity-linked securities.

He will have to pay the 15.4 percent dividend income tax and also a 38.5 percent comprehensive financial income tax. But he can’t pull his investment out of the fund. The money must stay in for a minimum of 90 days. If he pulls out, he has to pay a 30 percent penalty.

“I completely underestimated the comprehensive financial income tax on overseas equity funds,” said the hapless investor.

The global stock market has been on a tear and local investors who put money in funds investing in overseas equity funds have been enjoying hefty profits. But that makes them liable for a comprehensive financial income tax of as much as 41.8 percent on top of the 15.4 percent income tax levied on investment profits.

According to Zeroin, a financial investment provider, overseas equity fund investment in Korea has increased substantially. So far this year it has been able to attract over 1.6 trillion won. A lot of that is going into the Chinese market, where many Koreans are heavily investing.

Funds investing in Chinese equities have seen profits surge an average of 22 percent compared to the beginning of this year even though the market earlier this month saw a few adjustments on its bullish upswing.

When investing in financial products, investors usually pay a 14 percent dividend income tax and a 1.4 percent local tax. But when the financial income exceeds 20 million won, they are subjected to a comprehensive income tax with a maximum ceiling of 41.8 percent. This tax combines financial income along with other income such as annual salary and income made from leasing properties.

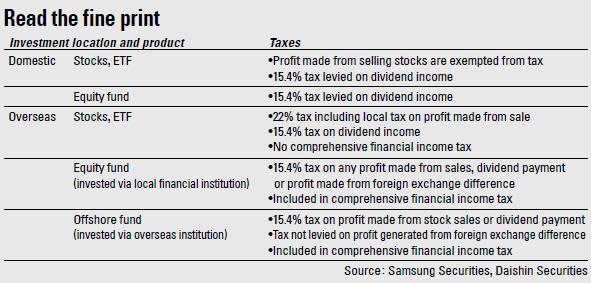

The tax on profits made from selling local stocks and bonds is different and is not subject to the comprehensive financial income tax. The only tax levied on profits from selling local stocks and bonds is 15.4 percent dividend and local tax.

The comprehensive financial income tax was first adopted in 1996 and 1997 but was put on hold in 1998 due to the Asian financial crisis. It was reinstated in 2001. The tax was previously levied on those who made a combined financial income from interest and dividend on financial products exceeding 40 million won. That bar was lowered to 20 million won in 2013.

With profit on equity funds hitting 20 to 30 percent, many investors are expected to be subject to the comprehensive income tax, even if they’re not particularly wealthy.

And few saw it coming.

“In the case of funds investing in China, if they have made an investment of roughly 50 million won they are likely to be subject to the comprehensive income tax,” said Kim Jung-nam, a researcher at NH Investment and Securities. “Especially since the level of taxable income has been lowered from 40 million won to 20 million won in 2013.”

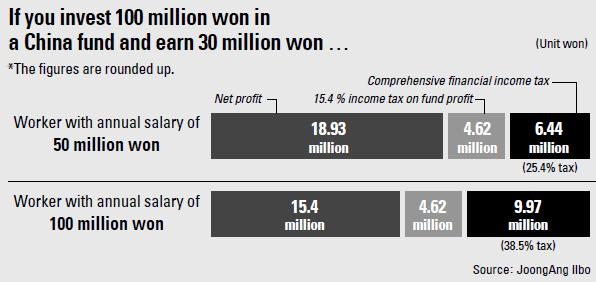

If a person has an annual salary of 50 million won and has made 20 million won on a China fund (excluding the dividend income tax), that investor will have to cough up an additional tax of 5.28 million won in comprehensive financial income tax.

“There are a lot of investors who were surprised as they previously thought [the comprehensive financial income tax] was a problem exclusively for the wealthy,” Kim said.

“If someone gives the fund to a spouse, up to 600 million won is nontaxable, and for children the ceiling is 50 million won,” said Shim Seung-ah, head of the fund investment team at Shinhan Investment Corp. “But when the amount exceeds those limits, the investor has to pay the so-called gift tax.”

Another way to avoid the comprehensive financial income tax is to use a pension account. When subscribing to an overseas fund via a pension account, it is not added to other income. It is only exposed to the pension income tax, which has a rate between 3.3 percent and 5.5 percent and other income tax with a tax rate of 16.5 percent. Additionally, when investing in a fund using a pension account, the investor could avoid being taxed on the dividend income tax.

BY JUNG SUN-EAN, LEE HO-JEONG [lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)