First 100 days prove K bank concept works

K bank is the first bank in the Korean banking sector that operates around the clock. This means if a customer needs to use a banking service after 4 p.m. - the typical closing time for regular commercial banks in Korea - all they have to do is call K bank’s service center located in Seodaemun district, western Seoul.

So when Park Seon-hee, a manager at the K bank call center, received a phone call early this month from a customer who wanted to discuss his loan choices but could only do so in the late evening, she consoled the caller and said, “We can call you back any time you want.”

Park used to be a teller at a local commercial bank. Along with 200 other former tellers, she decided to join K bank as more banks began downsizing their workforce and closing branches. KB Kookmin Bank, one of the largest commercial banks in Korea, dismissed nearly 3,000 workers earlier this year.

Meanwhile, Citibank Korea began the process of shutting down nearly 80 percent of its branches across the country, although the bank said it would not let go of any employees despite closures.

While cutting down on employees and branches, many commercial banks realized the need to go online, as demonstrated by K bank’s rapid rise since April.

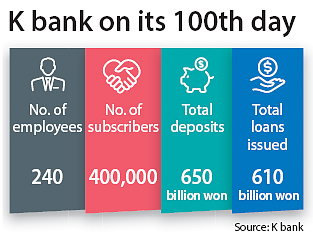

More than 400,000 customers across the country have accounts at the bank, with deposits totaling 650 billion won and loans of more than 610 billion won. K bank initially set the goal of accumulating 500 billion won in deposits and issuing 400 billion won in loans this year, demonstrating that public uptake of the bank has far exceeded its initial expectations.

To respond to the new market dynamic, existing Korean banks began introducing strategies of their own.

Wi Sung-ho, CEO of Shinhan Bank, outlined expanding the bank’s digital services as a top priority after his inauguration earlier this year. Shinhan created “digital group,” a department devoted to digital services, while launching “lab” agencies, dedicated to research and development in fields such as artificial intelligence and block chain. KB Kookmin recently revamped their mobile banking app to make it more “practical and easy to use.”

Yoon Jong-kyoo, the chairman and CEO of KB Financial Group, emphasized the need to “acquire service channels that do not limit place or time of services.”

Despite its role as the catalyst of changes in the local banking industry, K bank has the biggest obstacle to overcome if it wanted to sustain its services.

The current banking act caps bank ownership of non-financial institutions such as KT, a telecommunication provider who led the consortium that created K bank. This means, there is a limit to how much companies such as KT can contribute in terms of capital. The initial budget of 250 billion won is reportedly running dry. Under the current system, K bank will need to acquire funds from all members of the consortium, which includes startups and small companies who cannot afford to make significant contributions.

“While the law was necessary in the past to keep chaebols away from using banks as their private vaults, it is outdated now that financial authorities can better monitor such practices,” said an industry source. “Institutions such as K bank, that are still at the infantile stage, need bigger companies with capital to inject funds when necessary to maintain their competitiveness against already-large banks.”

BY CHOI HYUNG-JO, JEONG JIN-WOO [choi.hyungjo@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)