Getting a loan in just 60 seconds

He didn’t really need the money, but he figured the loan application was a good way to see how much he could borrow because he has a history of getting denied by traditional banks due to his low credit score.

Kim found out he could get up to 1 million won ($890) with an annual interest rate of 8 percent from Kakao Bank.

“I didn’t really need the money,” he said, “but I applied for it anyways. It only took a minute to get the loan.”

Such small loans are becoming a major business opportunity for banks. Those that don’t require heavy paperwork and can be delivered in a short period of time, as quick as one to three minutes through a mobile app, are especially popular.

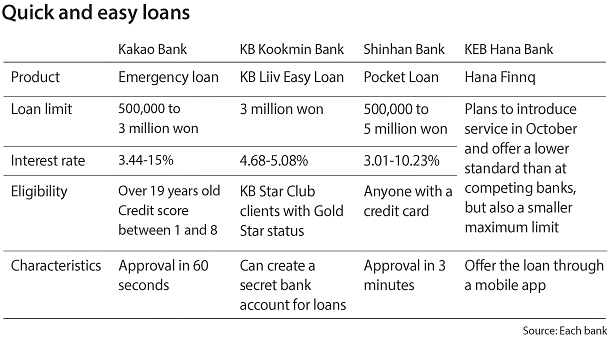

In fact, just over half of loans provided by Kakao Bank have been emergency loans, though by virtue of their small size, they’ve accounted for about 7 percent of the 1.4 trillion won that the bank has lent out since opening in July.

The biggest appeals of the loan product are quick delivery - the bank touts approval in 60 seconds - and fewer restrictions.

Anyone with a credit score under 8 on a scale of 1 to 10, with 10 indicating the worst credit, can take out an emergency loan at Kakao Bank. The upper limit is 3 million won, though most people borrow 1 million won on average.

Seeing Kakao’s success, the banking industry’s old stalwarts have started offering similar products.

KB Kookmin Bank’s KB Liiv Easy Loan lets its existing clients borrow as much as 3 million won without having to go through a rigorous identity verification process.

Shinhan Bank on Monday launched a mobile-exclusive loan program, where customers - even those without a history at Shinhan - can borrow as little as 500,000 won and as much as 5 million won as long as the applicant has a credit card.

KEB Hana Bank is working with SK Telecom, the country’s largest mobile carrier, on an app that can provide loan services.

Industry analysts believe the advent of mobile technology will make fast and easy loan services more widespread.

“Banks can set interest rates and limits on loans based on individuals’ credit scores without having to have those people file paperwork or meet in person for an evaluation,” said Lee Soo-jin, a researcher at the Korea Institute of Finance. “The introduction of internet banks has fueled competition in loan services, and the resulting convenience within the banking industry is a positive.”

The more easily accessible loans have relieved a burden for borrowers with mediocre credit scores, who previously had to rely on loan sharks for money.

However, there are also concerns that fierce competition in loan services could lead to a similar situation like in 2003, when Korean credit card companies started recklessly issuing credit cards to compete against each other, only to experience massive defaults that threatened the overall economy.

“There is a possibility that excessive lending could happen with the launch of internet banks,” Rep. Sim Sang-jung, leader of the Justice Party, said during a National Assembly meeting on Monday. “It reminds me of the credit card crisis that left four million people with credit insolvency in the early 2000s.”

Activists believe financial authorities need to more actively manage the risk from loans.

“The financial regulators are overlooking a situation where a new bank whose risk management has not been verified could recklessly hand out easy loans,” said Kwon Oh-in of the Citizens’ Coalition for Economic Justice. “The financial authorities have to intensify their management and oversight of loans because once interest rates go up and the loans mature, the amount of insolvent debt could increase.”

But while some experts agree that managing debt to avoid insolvency is necessary, they disagree that tightening regulations is the way to do it. Rather, they propose loosening regulations.

“The crucial point is whether loan evaluation can be properly done without having to go through a bank employee,” said Oh Jung-geun, a professor of financial technology at Konkuk University in Seoul. “The government needs to loosen regulations on big data so that internet banks can properly conduct their evaluations so that it won’t lead to insolvency.”

The professor said in the case of Chinese internet banks, they actively use big data, including transactions made on e-commerce sites like Alibaba as well as public data like tax payments, to evaluate the likelihood of loan repayment.

BY HAN AE-RAN [lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)