Crypto spring may be coming as banks get into the game

![[SHUTTERSTOCK]](https://koreajoongangdaily.joins.com/data/photo/2022/02/03/2164e9bc-3536-4d9e-988d-cd3071f71e3b.jpg)

[SHUTTERSTOCK]

The recent history of cryptocurrencies in Korea is a story of ups and downs, mania in 2017 followed by a long winter as uncertainty set in largely a result of regulatory confusion and the decline in value of bitcoin.

Institutionalization of cryptocurrencies could lead to a resurgence of interest in blockchain-based coins. With the likes of Goldman Sachs and JP Morgan beginning to support the asset class and offer products based on it, crypto is gaining legitimacy globally, and increasingly in Korea.

"Crypto assets have become a trend that cannot be resisted," said Lee Jae-sun, an analyst at Hana Financial Group.

The footprint is already significant despite challenges in recent years.

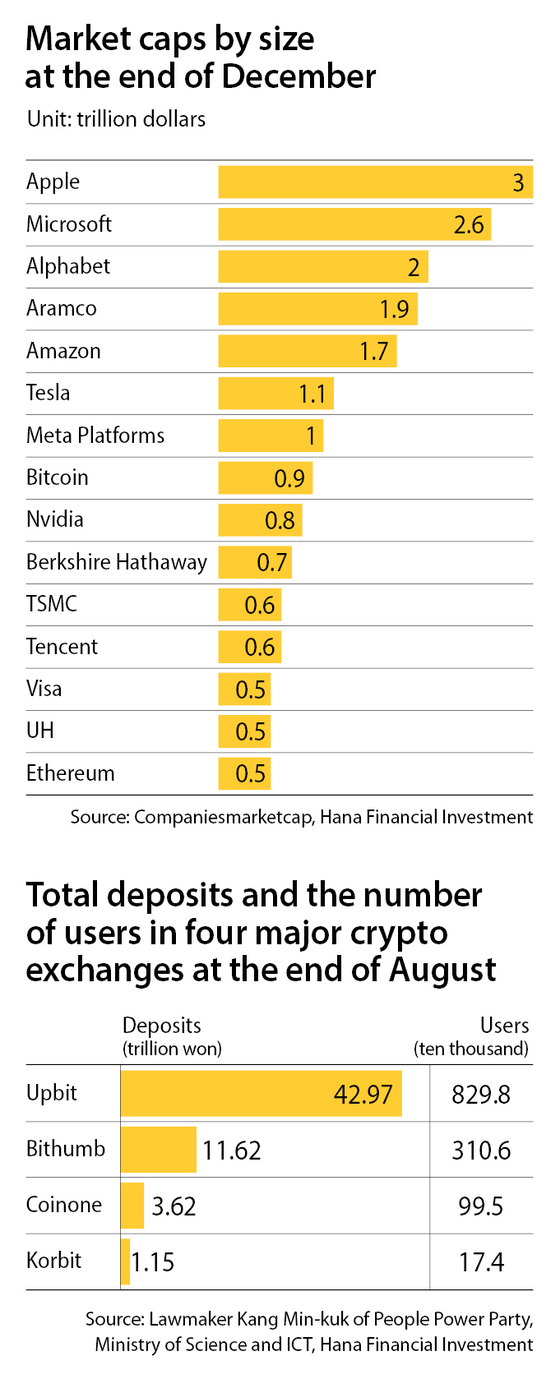

Total deposits at Korea's four major cryptocurrency exchanges — Upbit, Bithumb, Coinone, Korbit — jumped about 13-fold in a one-year period through August 2020. The global market cap for Bitcoin in 2021 was up 61 percent on year to around $900 billion.

With interest growing from banks, brokerages and central banks, the market could further evolve.

"Crypto assets were ignored or held in check by the finance industry when only characterized as a currency," said Lee Hak-mu, an analyst at Mirae Asset Securities. "But as its characteristic as a decentralized finance platform starts to be highlighted, it's rapidly becoming a subject of investment. The existing financial companies are enthusiastically reviewing investment in crypto assets and are trying to graft their advantages to their services. Through their participation, the virtual asset market will become less volatile and grow stably."

Crypto services

Domestic banks have been relatively slow in developing services related to crypto assets compared to banks in the United States. But there has been some progress recently.

In November, Shinhan Bank announced the completion of a review of cross-border wiring and transfer technology for stablecoins. Stablecoins are cryptocurrencies that can be pegged to a currency like the dollar. They are designed to avoid the volatility of cryptocurrencies.

With stablecoin transactions growing overseas, including JP Morgan's JPM Coin, the banks says it felt the need to review key related technologies to keep pace with the global market. A cross-border transaction service was one of its first choices.

The bank notes that the cross-border wiring of stablecoins is more convenient and affordable, costing less than a 100 won ($0.8) and taking a minute for the transaction to be complete compared to $20 and two days for traditional currency transfers.

The service is not yet being offered but is being tested.

KB Kookmin Bank, the largest bank in Korea by total assets, announced last month that it developed a "Multiasset Digital Wallet" capable of storing, transferring and making payments using the digital assets, including non-fungible tokens (NFT) and the central bank digital currency (CBDC).

The virtual wallet is based on the Klaytn blockchain, developed by Ground X, a Kakao subsidiary. The bank plans to add more functions to the digital wallet, like digital identification and electric documents.

KB Kookmin Bank indirectly offers cryptocurrency custody through KODA, a joint venture. The joint venture with Haechi Labs, a Seoul-based operator of a crypto wallet maker, started offering asset services in May.

Woori Bank is providing custody services through a joint venture with Coinplug, a Bitcoin-focused fintech provider. The joint venture, DiCustody, stores and manages crypto assets like NFTs, and allows for the storage and management of decentralized finance products. It was established in July.

Indefinite offerings

Though banks are very interested, they are highly cautious about offering crypto asset services they have already developed, saying they are just for research purposes.

"We don't have plans on marketing the cross-border wiring and transfer technology for stablecoins," said Cho Sung-woong, a spokesperson for Shinhan Bank. "Since there aren't established laws on crypto assets for banks, development of the service was just for research purposes."

Huh Woong, a spokesperson for KB Kookmin Bank, said the date for the Multiasset Digital Wallet being made available is "uncertain," adding the introduction was "intended to prepare for the future."

"According to the banking act, banks are required to provide only financial services if they roll out a new service that isn't part of their main business: loans, custody, exchange," said Kim Yeon-ju, a spokesperson for the Financial Services Commission (FSC). "We don't see services related to crypto assets to be a financial services."

Small equity investments are acceptable.

"Currently, there are no legal grounds for banks to handle crypto assets, so banks tend to become involved in crypto services through either the establishment of a joint venture or by buying a stake in a company," said Park Soo-jin, a spokesperson for Woori Financial Group. Bae Hyun-il another spokesperson for the company, said, "We made an indirect investment in cryptocurrency service as a way to monitor how the crypto market is being operated and potentially becomes a new revenue source."

Banks are allowed to acquire up to 15 percent of a non-financial company without FSC approval, according to Kim.

CBDC

The closest a bank has come to offering a product is the CBDC being developed by the Bank of Korea.

A CBDC is the virtual form of a fiat currency issued and regulated by a nation's monetary authority or central bank. They are being developed by central banks around the world, as cash usage lowers and finance becomes quickly digitized.

China has already trialed its CBDC across the country, while in the United States, the Federal Reserve initiated a review of the potential benefits and risks of issuing a U.S. digital currency, according to a report from the Wall Street Journal on Jan. 20.

The Bank of Korea recently completed the first phase of CBDC testing with successful results, with the second of the two phases set for completion in June. CBDC production, publication and distribution were tested in the first phase. In the following phase, the central bank is testing the feasibility of making a payments without an internet connection and adding new technologies, like strengthening the protection of personal data.

In a report released on January 24, the bank said that there are concerns that the adoption of a digital currency could "weaken the fund brokerage function of financial institutions, the effectiveness of monetary policy and the integrity of financial institutions and their systems."

The effectiveness of CBDCs varies by country.

"A CBDC won't make much difference in Korea's financial market, where creating a credit card or opening a bank account is easy," said Park Sun-young, an economics professor at Dongguk University. CBDCs will be more effective in countries where the financial industry is less developed because it can "raise financial inclusion by improving people's access to the financial system and help overcome the country's unstable currency."

Park added that a CBDC can make cross-border transactions more convenient by cutting transaction costs and time.

The Bank of Korea argues that a CBDC can create a difference in Korea.

"When a transaction is made through a credit card, the date of when a person receives payment is delayed for a couple of days," said Yoo Hee-jun, an IT specialist at the bank. "But when payment is made through a CBDC, there isn't such delay."

Some warn CBDC could also be a very useful tool for a central bank to hold a grip over their citizens.

"Under the CBDC system, the government can provide currency or cancel currency that was already issued, making it a very useful tool for the monetary policy," said Seo Byung-su, an analyst at Mirae Asset Securities. In some countries, such characteristic of the CBDC could be "used as a major tool to control citizens that resist the government."

"It's difficult to assert that all central banks will adopt CBDCs in the future, and even if they do decide to adopt one, it is expected to take a considerable amount of time until it is actually issued," the Bank of Korea said in the report.

BY JIN MIN-JI [jin.minji@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)