MSCI or bust even as index inclusion raises some questions

Korea is continuing to push for inclusion in the MSCI Developed Market Index, a challenging jump that would bring investor recognition at the possible expense of market stability and the ability to control speculation and hot-money flows.

New York's MSCI is an investment research firm that provides stock indexes. The indexes are divided into three categories: developed, emerging and frontier markets. Mutual funds and exchange-traded funds (ETFs) track MSCI indexes.

Korea is in the emerging market index.

Financial regulators are hoping to make a number of adjustments to the market for won trading and in rules for short selling in the first half to meet the conditions for inclusion in the MSCI index.

Korea has made attempts to be upgraded since it was added to the MSCI Emerging Markets Index in 1992. But MSCI had asked Korea to open a 24-hour offshore currency market and ease regulations on the registration of overseas investors to get to the next level.

The government's goal is for Korea to be placed on the watch list in June. To be reclassified, a country is required to be on the watch list for at least one year. If Korea makes it onto the list this year, actual inclusion in the MSCI Developed Market Index could happen in 2024.

Korea's inclusion in the index could push up the benchmark Kospi to as high as 4,500 points if earnings grow 10 percent a year, according to a Feb. 14 report from Goldman Sachs.

"A developed market upgrade could prompt over $44 billion potential incremental foreign investor portfolio flows," the report read, adding that Korea's persistent valuation discount may narrow following the reclassification.

Korean stocks have historically traded at lower multiples than stocks in other comparable markets. The phenomenon is known as the Korea discount.

Background

The subject of the MSCI index was brought up in 2009 when the Financial Times Stock Exchange Group (FTSE) reclassified Korea as a Developed Market.

FTSE, a wholly owned subsidiary of London Stock Exchange Group, is also an index provider.

"Korea already achieved the economic status and fulfilled the conditions to be included in the developed market index in late 2000s in terms of liquidity," said Noh Dong-kil, a senior researcher at Shinhan Investment.

Korea's stock market cap is No. 11 globally, 8.3 times Israel's, which was included in the MSCI Developed Market Index in 2010.

Korea is the world's 10th largest economy and has a gross national income per capita of $33,000. With an economy this big, Korea languishing in the emerging market index is "unprecedented," according to a report from the Korea Economic Research Institute released in May.

But the MSCI is requiring more than just market liquidity.

It says Korea still needs to improve in six categories to make its market more accessible globally.

The six categories are: foreign exchange market liberalization level; investor registration and account setup; market regulation information flow; a well-functioning clearing and settlement system; eased transferability of securities; and the availability of investment instruments such as ETFs, futures, options and swaps

.

Key achievements needed would be an offshore currency market, the resumption of short selling, English-language information readily available, improved corporate governance standards and the determination of the dividend at board of directors meetings.

Financial authorities have been conservative about opening Korea's currency market because "the 1997 Asian financial crisis left a strong impression that the sudden foreign capital outflow could be detrimental enough to put a country's financial system at risk," said Lee Hyo-seob, a researcher at the Korea Capital Market Institute. "But the government recently announced plans to open the foreign exchange market after years of setting the foundation, like accumulating enough foreign reserves and growing strong exports to buffer risks when currency volatility temporarily rises."

Effort for reclassification

In response to the MSCI requests, Finance Minister Hong Nam-ki said last month the government is considering extending the foreign exchange market operating hours and permitting foreign financial institutions to directly take part in the interbank foreign exchange market to encourage more foreign participation. It is also considering easing regulations on offshore transactions of the Korean won.

Only locally-licensed institutions are allowed to participate in onshore dollar-won spot market trading, and only from 9 a.m. through 3:30 p.m. Overseas investors rely on the non-deliverable forwards market to manage their exposure to the won offshore.

For the index upgrade, Korea is also expected to fully resume short selling in the first half.

Short selling was partially resumed last year for large and mid-cap companies in the Kospi 200 and Kosdaq 150 indexes after it was prohibited for all shares in March 2020 following the market crash caused by the Covid-19 pandemic.

"The existence of active stock lending and short selling practices has become a clear standard in Developed Markets in support of direct hedging practices and quantitative management," according to the annual MSCI Global Market Accessibility Review released in June last year. "Stock lending and short selling activities also need to be efficient and well tested."

Lee Jae-myung, a presidential candidate from the ruling Democratic Party, pledged to improve the short selling system instead of scrapping it. Some retail investors are demanding the government end short selling, saying institutional and foreign investors benefit from the system at their expense.

"A complete scrapping of short-selling system is against the upgrade to the MSCI Developed Market Index," Lee said, promising to strengthen monitoring of the system.

Yoon Suk-yeol of the People Power Party pledged to adopt a circuit breaker system for short selling when a stock plunges excessively, while remaining vague about the full resumption of the system.

Impacts

Korea's inclusion in the MSCI Developed Market Index could attract more foreign capital and reduce market volatility.

"It's easier to attract investment when a country is included in the developed market index because the inclusion means it has received an international nod as a place for safe investment," said Won Chae-hwan, a finance professor at Sogang Business School.

The total assets for ETFs managed by Vanguard that track developed markets jumped 1,618 percent since early 2010. The growth for emerging market ETFs was 249.4 percent, according to a February report from Shinhan Investment.

"Market volatility in developed markets has also been historically lower due to relatively smaller changes in fund flows and currency" rates, the report read.

This is because capital invested in the developed market index is commonly made as a long-term investment for pension funds or sovereign wealth funds, compared to the capital from hedge funds for the emerging market index.

The upgrading would also help Korea avoid risks caused by remaining in the emerging market index.

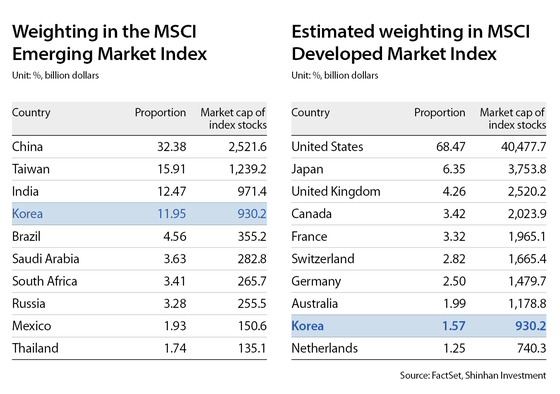

China receives most emerging market index investment, followed by Taiwan, India and Korea.

The weight of Korean stocks in the MSCI Emerging Market Index fell to 11.9 percent from 15.4 percent in late 2012. During the same period, the weight of Chinese stocks went up 19.4 percentage points to 32.4 percent from 13 percent in late 2012.

China's growth over the years was helped by its large initial public offerings.

The total IPO funds collected by Chinese companies both in and outside the country was 1.3 trillion yuan ($205 billion), or 245 trillion won, in 2020, compared to 4.54 trillion won in Korea in the same year.

But Korea could be a star in the developed market index.

"Korea is an economy with a relatively high growth rate compared to others in the developed market index, like the United States and Japan, on the growth of the bio, self-driving vehicle and semiconductor sectors," said Lee.

Critics counter that foreign capital may not be good for Korean companies.

"Korean shareholders tend to value long-term growth, whereas foreign investors, like those from the United States, value the shareholder return policy," said Won. "Divided allocation could lower a company's growth potential."

"It's not certain that the reclassification on the MSCI index alone will lead to the rapid inflow of foreign capital and result in a Kospi and Kosdaq boost," said Lee. "The Korean indexes will go up under the condition that uncontrollable factors like geopolitical risks or global monetary tightening do not newly intrude."

BY JIN MIN-JI [jin.minji@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)