Local banks face changes as regulators push for more competition

![A customer uses an ATM installed in front of a diner in Seoul on Feb. 16. [YONHAP]](https://koreajoongangdaily.joins.com/data/photo/2023/02/28/96094a64-d444-4179-8125-a7118f77a239.jpg)

A customer uses an ATM installed in front of a diner in Seoul on Feb. 16. [YONHAP]

Stock prices of financial holding firms remain sluggish as financial regulators continue to pressure banks to play a bigger role in sharing their record profit with the public.

The share price of KB Financial Group is down 15 percent from its recent peak in January. Shinhan Financial Group is also down 13 percent in the same period. Hana Financial Group is down 15 percent and Woori Financial Group 10 percent.

The prices peaked in January on an activist fund’s push for higher shareholder returns from financial holding firms and the regulators’ earlier remarks to minimize intervention in banks’ dividend policy. But the stocks weakened from mid-February on President Yoon Suk Yeol’s description of the banks as having a “strong characteristic of public goods” earlier this month because of the industry’s oligopoly structure.

Financial regulators followed suit, criticizing banks for redistributing their record profit to employees and not sharing enough with the public that are suffering from high interest burden amid the rapid rise of policy rate.

Regulators said they will review methods to intensify competition in the banking industry, like the introduction of challenger banks. They are small and recently created retail banks that compete with the longer-established banks. The Fair Trade Commission also announced plans to review banks' sales policies or unfair terms and conditions that could limit competition.

“Government regulations usually don't hurt banks' stock prices because regulations have long been there," said Kim In, an analyst at BNK Securities.

"But they recently fell because the president’s remarks disappointed investors that expected the new administration to deregulate the bank industry. But banks are strengthening their shareholder return policies, and are projected to report more record earnings this year on the rise of net interest margin, so the outlooks for their stock this year is solid.”

Strengthening oligopoly structure

The five major commercial banks in Korea are KB, Shinhan, Hana, Woori and NongHyup. They accounted for 74 percent of all loans and 63 percent of all deposits as of the end of last year.

“Banks have public nature because the industry became oligopolized by the government,” said Lee Jeong-hwan, an associate professor at the College of Economics and Finance at Hanyang University.

To operate a bank, an approval by the Financial Services Commission (FSC) is required.

Korea’s banking industry has become oligopolized following the Asian financial crisis in 1997. To avoid chain bankruptcy, the government pushed mergers and acquisitions among banks.

More than two decades later, it has become very difficult for the oligopoly structure to be threatened. The structure grew more solid following the exit of global banks.

Citibank Korea announced in 2021 it will wind down consumer banking in Korea as part of its global business reorganization. The Northern Trust Company, an Illinois-headquartered wealth management firm, pulled out from the country after six years of operation, according to local media reports in December. Bank of Nova Scotia, Canada's third-largest bank, shut down its operations in 2021.

“It now seems impossible to intensify competition in the banking industry because their total assets and banking history — the two crucial factors in a bank — have built up to a level that can’t be easily caught up to by a new bank.” Lee added.

The oligopoly structure has helped banks run business by focusing on lending relatively safe loans, which has raised their financial soundness.

The banks are therefore able to function as a prop when the economy faces a financial crisis,” Lee added.

Vulnerability to government intervention

But this structure has also made banks vulnerable to government intervention in their business operations, which has been the key factor that led to the sector’s undervaluation.

The president recently told banks to come up with ways to reduce the loan-deposit margin, while financial regulators advised banks to raise financial soundness by increasing their appropriation for bad debts, which could affect their shareholder return policies.

The average loan-deposit interest margin at local banks over the past five years through last May was 2.01 percent, according to the Financial Supervisory Service last July. The rate is higher than Hungary (1.59 percent), but lower than other major countries, including Singapore (5.11 percent), Hong Kong (4.98 percent) and Switzerland (2.98 percent).

“Pressuring banks on how they run business inevitably results in a Korea discount because it directly affects shareholders’ expected profit and dividends,” said Seok Byoung-hoon, an economics professor at Ewha Womans University.

The Korea discount refers to a tendency for Korean companies to have lower valuation than their global peers.

“Financial authorities’ pressure on banks to raise their role for the public is a direct violation of the free market.” said Won Chae-hwan, a finance professor at Sogang University. “The regulators should not ride on public sentiment of criticizing banks.”

Sources from the finance industry say the pressure is too harsh.

“Banks are private companies,” said an industry insider who spoke under the condition of anonymity. The recent pressure seems a little unreasonable as the interest rate went up along with the Fed’s monetary tightening to tame inflation.”

But banks also benefited from the regulations.

The four financial groups, excluding NH, reported record earnings last year largely led by high interest rates.

The large amount of incentives and severance pay were given based on the record net profit.

The estimated incentives given out by the five major banks to employees for last year’s performance stand at around 1.38 trillion won, up 35 percent on year.

A primary reason for the record earnings is the rapid rise of the property prices under the previous Moon Jae-in administration and the aggressive monetary tightening over the past year and a half, during which the policy rate was upped by 300 basis points.

Outstanding household loans in 2021 rose 123.5 trillion won, while shrinking 7.8 trillion won last year on the rapid rise of the policy rate.

The banks' interest margins grew from last July to January.

The net interest margin at KB Bank, for instance, grew to 1.81 percent from 1.18 percent from last July to January. That of Woori Bank grew to 1.59 from 1.29 percent, while Hana Bank inched up to 1.44 percent from 1.10 percent in the same period.

Complaints from customers

Customer complaints against banks have grown along with the rise of loan rates and the record incentives employees received.

The rapid shutdown of branches and shortened operating hours after the Covid-19 outbreak built up their anger.

“What achievement did banks accomplish?” wrote a commenter on an online community for workers called Blind in February. “The self-employed are falling and facing bankruptcy because of the lack of liquidity. Banks deserve to be pressured more”

“Why is the labor union so against returning the operating hours back to how they was?” wrote another commenter in January. “They are acting so selfishly.”

Banks returned to their normal operating hours late January from 9 a.m. through 4 p.m., after the hours were reduced by an hour due to the pandemic.

As complaints grew, banks also began lowering their loan rates.

KB announced it would cut its mortgage rate and loans for jeonse (when a very large refundable deposit is paid up front for rent-free occupancy for a fixed period) by up to 0.55 percentage points starting on Feb. 28. Woori Bank also cut its mortgage rate for a five-year loan by 0.20 percentage points in February, while Hana and Shinhan said they are reviewing reducing their rates.

Banks are also hiring more.

Twenty banks in Korea are expected to hire 2,288 workers in the first half of this year, which is up 48 percent from a year earlier, according to the Korea Federation of Banks.

As for shareholders, banks promised higher returns.

KB Financial Group’s total shareholder return for last year was 33 percent, up 7 percentage points on year, while Shinhan Financial Group upped the return by 4 percentage points to 30 percent in the same period.

The banks announced plans to improve the returns, including Hana Financial Group that set its total shareholder return in the mid-to-long term at 50 percent. Shinhan is aiming for a rate between 30 and 40 percent this year.

Their efforts should go beyond to make structural changes in how they make profit.

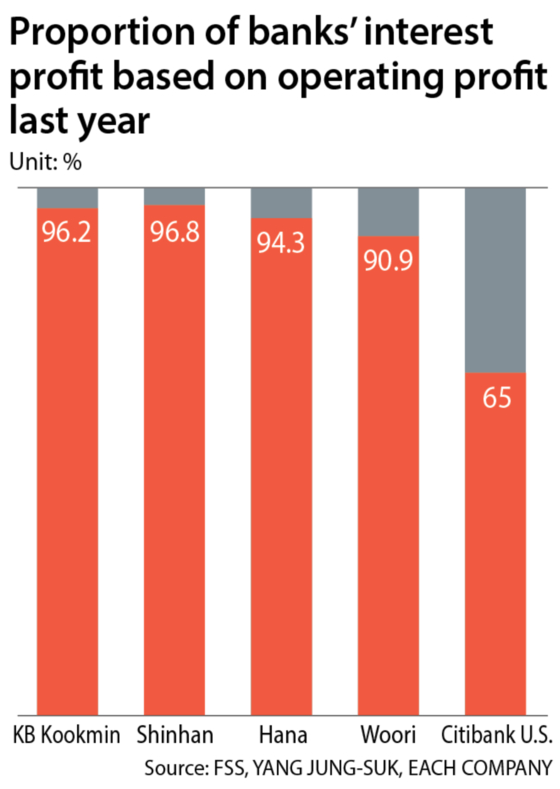

“Banks tend to rely excessively on interest margin without putting much effort into developing non-interest profit,” said Won. “They have to expand their sources of profit in various ways instead of just trying to cut costs by downsizing the workforce and closing down branches.”

Non-interest profits at seven financial groups, including BNK, DGB and JB, only accounted for 19.2 percent of their total profit as of the end of 2021, according to Kim Woo-jin, a senior research fellow at Korea Institute of Finance’s banking industry division.

BY JIN MIN-JI [jin.minji@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)