Household debt in Q2 hits new record of $1.42T as mortgage wave continues

Published: 20 Aug. 2024, 16:53

Updated: 21 Aug. 2024, 13:50

-

- SHIN HA-NEE

- shin.hanee@joongang.co.kr

![Financial Services Commission Chairman Kim Byoung-hwan speaks during a meeting with chief executives of domestic banks held at the Korea Federation of Banks in central Seoul on Tuesday. [YONHAP]](https://koreajoongangdaily.joins.com/data/photo/2024/08/21/3bcc6e0a-74d7-4485-8efd-b2bb20fd2001.jpg)

Financial Services Commission Chairman Kim Byoung-hwan speaks during a meeting with chief executives of domestic banks held at the Korea Federation of Banks in central Seoul on Tuesday. [YONHAP]

Korea’s outstanding household credit rebounded to a fresh record in the second quarter, driven by the continued surge of mortgages, central bank data showed Tuesday.

As real estate transactions in Seoul and the surrounding regions continue to grow ahead of anticipated rate cuts within the latter half of the year, the financial authorities are tightening loan regulations to rein in rising housing prices.

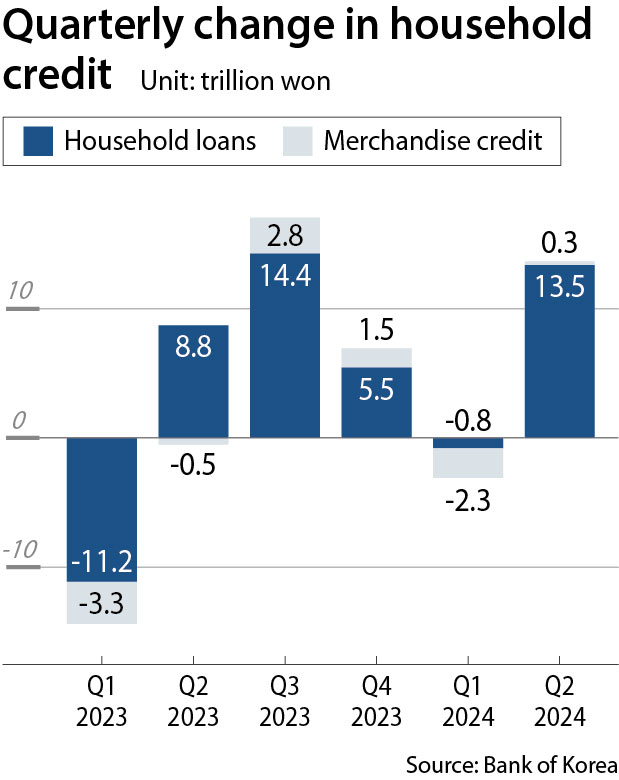

According to preliminary data from the Bank of Korea (BOK), outstanding household credit, which includes both household loans and purchases on credit, came to an all-time high of 1,896.2 trillion won ($1.42 trillion) at the end of the second quarter, up 0.7 percent or 13.8 trillion won from the preceding three-month period.

This is a reversal from the previous quarter’s decline of 3.1 trillion won on quarter.

Outstanding household loans stood at 1,780 trillion won, an increase of 13.5 trillion won, or 0.8 percent, from the end of March.

Outstanding mortgage loans, in particular, increased by 16 trillion won to 1,092.7 trillion won in the second quarter. The growth accelerated from the previous quarter’s 12.4 trillion won expansion.

Merchandise credit, which refers to the outstanding balance of credit card purchases by households, rose by 300 billion won to 116.2 trillion won, after logging a quarterly decrease of 2.3 trillion won in the January-March period.

Household loans are expected to further grow in the third quarter as well.

“As housing transactions affect [the household debt level] with a gap of about two to three months, we believe that household credit growth is likely to come at a similar level to the second quarter in the third quarter as well,” said Kim Min-soo, head of the financial statistics at the BOK, on Tuesday during a press briefing held in central Seoul.

![Kim Min-soo, head of the financial statistics team at the Bank of Korea (BOK), speaks during a press briefing held at the BOK headquarters in central Seoul on Tuesday. [BOK]](https://koreajoongangdaily.joins.com/data/photo/2024/08/21/ab82a96e-baf1-464c-aea4-0a1bb9e8f106.jpg)

Kim Min-soo, head of the financial statistics team at the Bank of Korea (BOK), speaks during a press briefing held at the BOK headquarters in central Seoul on Tuesday. [BOK]

Kim stressed that the government and the banks are closely monitoring the situation.

“The financial authorities and banks have been bolstering efforts to manage the household debt level, a new housing supply initiative was announced on Aug. 8, and the second-phase stressed DSR [debt service ratio] program will also take effect in September as planned,” said Kim, adding that “such efforts will begin to make a notable impact with a delay, so we need to monitor how the effects come.”

As mortgages continue to grow with housing transactions increasing, banks have been raising interest rates for mortgage products, while the financial authorities are further tightening regulations.

The Financial Services Commission (FSC) on Tuesday announced that it will up the hypothetical spread added to interest rates when issuing mortgages in the greater Seoul area to 1.2 percentage points, compared to 0.75 percentage points applied to other regions, under the second-phase stressed DSR scheme set to be implemented in September. The goal is to temper the rising apartment prices in Seoul and the surrounding regions by lowering the loan limits.

The stressed DSR rule was designed to reduce the limits by adding a hypothetical spread when calculating these limits in consideration of potential future rate hikes. The goal is to adjust the limits based on expected hikes, considering the potential increase in repayments on floating-rate loans during rate hike cycles. The spread is applied only for calculating loan limits and is not included in the actual interest rate.

“In the current situation, banks need to be cautious and preemptively manage household debts,” FSC Chairman Kim Byoung-hwan said during a meeting with CEOs of banks held in central Seoul that day.

“We request the banks to have a household debt management system in place on a voluntary basis based on the stressed DSR program,” said Kim.

BY SHIN HA-NEE [shin.hanee@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)