Crushing household debt is starting to worry central bank

According to the central bank’s monetary and credit policy report released Thursday, household debt to nominal gross domestic product reached 103.8 percent as of the end of last year. The ratio is the sixth highest among 37 members of the Organization for Economic Co-operation and Development.

On-year household debt growth was positive in every quarter last year.

In the first quarter, household debt grew by 4.6 percent on year. In the second quarter, the growth was 5.2 percent, in the third quarter 7 percent and in the fourth quarter 7.9 percent.

Soaring house prices was the main driver.

House prices in the first quarter of last year increased by 1.1 percent on year. In the second quarter, house prices rose by 2.4 percent on year, third quarter 4.5 percent and fourth quarter 7.2 percent.

In the first quarter of this year, house prices skyrocketed by 10.3 percent on year.

The greater Seoul house-price-to-income ratio in the first quarter this year reached 10.4, meaning that the average home price is 10.4 times annual average income.

The ratio was 6.8 in the first quarter of 2017, 7.2 in the same quarter 2018, 7.8 in 2019, and 8.4 in 2020.

Some economists argue that debt can help economic recovery, but too much debt is invariably seen as a problem.

If high debt repayments reduce money available for spending, demand can drop.

According to a report by the International Monetary Fund in 2017 on the effects of household debt growth on private consumption and economic growth, a 1 percentage point increase in household debt led to 0.23 percentage point increase in private consumption in the first year. However, from the third year, consumption growth went negative, indicating that household debt growth in the long run negatively affects private consumption.

The central bank noted in report that positive correlations between debt and consumption growth have weakened as the country's household debt growth rate has outpaced income growth since 2014.

"Funds being pulled into certain focused areas like real estate could increase economic volatility and weaken a country's growth potential," the bank said in report.

"It has been a long time since Korea's household debt ratio passed a level that could help boost consumption," said Ha Joon-kyung, an economics professor at Hanyang University. "As debt weighs on households, there is a big possibility the financial market could face instability."

The central bank, despite the warning, said the country's financial system won't collapse due to the accumulated debt for now saying "local banks have sound capital adequacy ratios and the capacity to absorb losses."

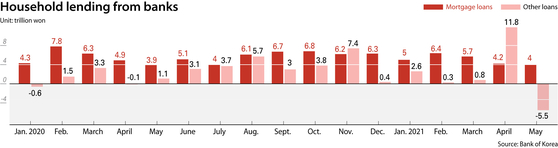

The balance of household borrowing from banks decreased by 1.6 trillion won ($1.4 billion) in May compared to the previous month. It is the first time since January of 2014 that household debt growth fell month on month. The balance came to 1,024.1 trillion won as of May.

The decline was largely due to people paying back money they borrowed after subscription deposits for SK IE Technology were returned to investors early last month. People had borrowed heavily to subscribe to publicly offered shares of the battery material company.

The balance of household mortgages stood at 747.2 trillion won as of the end of May. The balance increased by 4 trillion won compared to April. The increase was smaller than 4.2-trillion-won increase in April compared to the previous month.

However, the bank said the growth is still very fast.

BY YOUN SANG-UN, KIM JEE-HEE

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)