47 accounts get intensive audits

In another case, a businessman named Yoo opened an offshore bank account under the names of his employees in overseas branches. He then hid kickbacks that he received from overseas business partners under the assumed-identity account, never reporting his personal holdings to the Korean tax agency.

These are two of the 47 accounts undergoing intense audits by the Korean National Tax Service (NTS).

The agency yesterday again reaffirmed its determination to track down offshore tax dodgers.

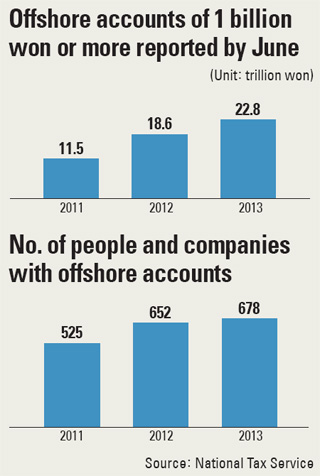

The agency said 678 individuals and businesses reported having overseas financial accounts of 1 billion won ($892,260) or more as of the end of June. The total amount reported was 22.8 trillion won. This is a 22.8 percent increase compared to a year ago.

The tax agency said 310 individuals reported 1 billion won or more in offshore accounts, a 2.6 percent increase from a year earlier; 368 businesses reported such accounts, a 5.1 percent increase.

Individual account holders had 2.5 trillion won in 1,124 offshore accounts, which is 19 percent more than last year. Businesses reported 20.3 trillion won in more than 5,500 accounts, up 23.3 percent year-on-year.

According to the tax agency, 44 percent of the 310 individuals reporting have 1 billion won to 2 billion won in their accounts, 31 percent have 2 billion won to 5 billion won and 25.1 percent have more than 5 billion won.

In the case of companies, 54 percent have more than 5 billion won in their offshore accounts, 22 percent have between 2 billion won and 5 billion won, and 22 percent have 1 billion won to 2 billion won.

Most financial holdings in foreign accounts were in cash deposits and savings, which accounted for 51 percent, followed by stock accounts at 46.6 percent. Last year, deposits and savings accounted for 48.9 percent and stocks 49.4 percent.

The offshore accounts reported were in 123 countries, five more than last year and eight more than in 2011.

The top five countries for Koreans’ individual overseas accounts were Japan (1.1 trillion won), the United States (658.2 billion won), Singapore (165.3 billion won), Hong Kong (154.6 billion won) and Switzerland (96.8 billion won). Hong Kong saw the largest increase, skyrocketing 63.9 percent from last year’s 94.3 billion won.

For Korean companies, Japan still ranked No. 1 (6.4 trillion won), followed by the United States (2.4 trillion won) and China (1.7 trillion won). Singapore and the United Arab Emirates rounded out the top five.

Most companies or individuals owning large offshore financial accounts were concentrated south of the Han River.

The largest amount of overseas holdings came from Banpo, where 411.5 billion in accounts were reported, followed by north-of-the-Han Yongsan (276.5 billion won).

The other top areas - Yeoksam, Samseong, Jamsil, Seocho and Gangnam - were all south of the river.

“We will make sure that we penalize those who failed to report their offshore financial accounts,” a tax agency official said.

BY LEE HO-JEONG [ojlee82@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)