Saving for pensions can be tricky

“At a time like this when interest rates are so low, I believe the best investment move is to subscribe to products that can save on tax payments,” Kim said. “As a result the most appropriate investment is the pension savings, through which I can get a tax refund after settling my taxes.”

The government recently introduced a plan of raising the tax refund on pension savings for people with annual salaries under 55 million won ($51,000). The previous tax refund rate of 13.2 percent has been raised to 16.5 percent. The tax refund ceiling was raised from 4 million won to 7 million won.

But for people whose annual income is more than 55 million won, the refund rate remains 13.2 percent.

Investors like Kim are on the rise. They save on yearly tax payments while buying a product that pays off after retirement.

But some studies warn that subscribers might be disappointed with the payoff they receive after retirement.

According to the Bank of Korea, pension and insurance investments by households last year (including nonprofit organizations) accounted for 31.5 percent or 909.6 trillion won out of a total 2,885.8 trillion won in financial assets.

Insurance and pension investments have been growing by roughly 100 trillion won every year. Investment poured into pensions have been on a particularly steep rise.

A Mirae Asset Retirement Institute study shows that in 2010, pension saving investments amounted to 59.6 trillion won. That figure grew to 78.8 trillion won in 2012 and to roughly 101 trillion won last year.

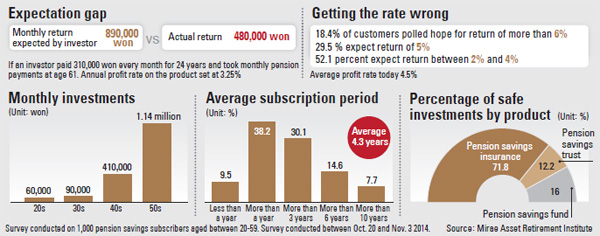

A survey of 1,000 pension savings subscribers by the institute showed that on average the clients expect to receive an average 890,000 won every month when they retire. However, the actually amount they are likely to receive is nearly half of that, or 480,000 won on average.

There are several reasons for the gap. Investors usually expect a higher profit rate than they actually get; the amounts they invest in pension savings are often small; the number of years they subscribe to the product is often shorter than the average 4.3 years; and many subscribe to products that are more concentrated on guaranteeing the principle repayment rather than those that offer higher returns, with higher risks.

“Our study found that because the payments the investors make is small, payout they receive is actually between 23 and 84 percent of what clients expect, depending on age group,” said a senior researcher at the retirement institute.

To fully utilize pension savings, the institute recommends increasing investments beyond the tax refund ceiling of 7 million won; reinvest the tax refund in pension savings; subscribe to the products as early a possible; and don’t cancel the subscription before maturity.

A researcher at Samsung Securities’ retirement planning center recommended pension savings funds over pension savings insurance for people with unstable incomes.

“In the case of a pension savings fund, someone can miss a monthly payment if they don’t have the money, but in the case of pension savings insurance, a contract is immediately cancelled when the monthly subscription is not paid on time,” the researcher said.

BY KIM CHANG-GYU [lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)