How internet banks could affect credit scores

Aside from the fact that they would rid the need to visiting brick-and-mortar locations, these banks, which are created by consortiums led by major IT companies, are determined to analyze a wide spectrum of data, such as one’s online shopping history in deciding a person’s credit score. While the idea itself is generally welcomed, analysts said banks must be careful in adopting such models, largely because some data may be misleading and unrelated to a person’s creditworthiness.

Currently in Korea, a person’s credit score is solely based on traditional financial data such as utility bill payments, making the new model planned by the internet-only banks unconventional. However, outside of Korea, similar models are frequently used already. For instance, Amazon, an American e-commerce giant, analyzes a person’s purchasing history to issue the customer a credit card even if the person is not qualified for one at local banks.

A professor at a university in Seoul thinks such system would change how things are done in Korea, as warranted by his own experiences. Granted a research project suddenly in the United States about a year ago, the professor had little time to prepare himself for life outside Korea. Upon arrival, he realized his credit card was for domestic-use only and without any record of transactions in the United States, his applications for a card from a U.S. bank were rejected. Amazon, from whom the professor had purchased books for several years, came to the rescue. Logging into Amazon one day, he received an inquiry asking if he wanted a credit card issued through Amazon. He eventually obtained a card that allowed him to spend as much as $2,000 a month.

“What Amazon used in such a case was the person’s purchasing history,” said a market insider and big data specialist from the United States. “If you use Amazon frequently, you can notice that after shopping with the company for a while, it gives you suggestions of items that you might be interested in buying. That’s done through analyzing the company database that includes your past search or purchasing history. In the professor’s case, Amazon knew he was a frequent and reliable shopper, not a risky one.”

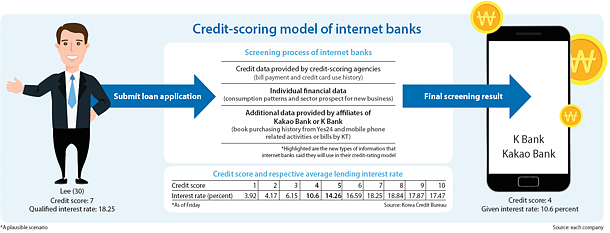

Similarly, borrowers with poor credit ratings in Korea - maybe due to lack of financial activity or other issues unrelated to creditworthiness - who are currently forced to turn to savings banks or loan sharks, may be given an escape from high interest rates and see their qualified rates go down from nearly 20 percent to around 10 percent.

“Our model will be similar to that of Amazon,” said a spokesperson from Kakao Bank. “Basically, we will use a variety of data about a person, rather than just his financial activities, which can be not expansively reflective of the person’s true reliability.”

Kakao Bank explained recently that, for instance, if a taxi driver wants to borrow money from the bank, the bank will evaluate his driving records or customer evaluations as well as things he bought on the internet, such as books on money management and investment, to decide his credibility. One of the companies included in the Kakao Bank consortium is Yes24, a Korean book company.

“This is just a long-term plan for now but we eventually would like to be able to do this,” said the spokesperson.

K Bank, which is in the final countdown of its launch, said it will adopt a similar credit scoring system. “We will still use information provided by the credit bureaus in Korea,” explained a bank spokesperson. “But in addition, we will analyze big data stored in the data banks of our affiliates.”

Oh Jung-geun, a researcher at Korea Economic Research Institute and a professor at the school of information and telecommunications at Konkuk University, said while he welcomes such a model, internet-only banks must develop a new paradigm to minimize losses.

“Right now, a loan screening process is done by employees of the banks,” Oh said. “But in the near future, it will be done by big data analysts who will have to plow through inexhaustible amount of data.”

“The success of such a model will depend on how well they find the relevant factors from the pool of data out there,” Oh added. “Mining appropriate data will be crucial because if they fail in cherry-picking and misjudge a person’s credit worthiness, it may lead to bad loans, which incur losses.”

Even some potential borrowers were skeptical and said the banks will have to implement safety-measures to prevent manipulation.

“So if I bought many books about investment and money management, would that give me better rates? But what if I just bought them to raise my credit score but never actually read them?” asked Lee Seung-geun, an office worker in Seoul. “It looks like the system could have so many loopholes.”

BY CHOI HYUNG-JO [choi.hyungjo@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)