Islamic bonds stuck in limbo

The Korean government last year promised to ease restrictions that would pave the way for the local issuance of Islamic, or sukuk, bonds that are favored by Muslim investors because they conform to Islamic laws banning interest payments.

The questions from the Islamic investors place Lee in an awkward position.

“I’m afraid that one day, they may find out what’s really going on in Seoul. I’ve been telling them for months the same story, saying the change will come soon. But I can’t field the questions this way for too long.”

The reason for Lee’s embarrassment is that the proposed changes being considered in the National Assembly are being blocked by Christian activists who claim that the sukuk bonds are being used to finance terrorism.

“Several Protestant church groups have lobbied against the bill, claiming about 5 percent of the money involved in sukuk sales is being used for terrorism-related funds,” said Na Seong-lin, a Grand National Party lawmaker and a member of the National Assembly taxation subcommittee that is considering the sukuk bond proposal.

Na said he found the allegations “absolutely ridiculous” and “lacking any evidence.” But political considerations ahead of local elections in June are making it hard for lawmakers, especially those with strong backing from Protestant church groups, to deal with the sukuk legislation, said Na and several National Assembly aides who did not want to be named.

The taxation subcommittee, chaired by Grand National Party lawmaker Lee Hye-hoon, has repeatedly delayed finishing a formal review of the sukuk bill, explaining in a memo by the panel last November that some sentences in the bill may “give an impression that local companies have to follow tenets of a certain religion.”

The disputed bill, which was proposed by the Finance Ministry in September, did not appear on this month’s legislative agenda to be reviewed by the nine lawmakers on the taxation subcommittee, which reports to the Strategy & Finance Committee.

The legislative impasse is proving frustrating to Korean companies who want to tap into the growing Islamic bond market for new sources of capital and local financial institutions who want to collect fees underwriting the sukuk bond issues.

“It’s embarrassing,” said a senior Finance Ministry official, who declined to be named, about the objections being raised to the legislation that would make changes in the tax code to allow the Korean issuance of the sukuk bonds.

The official said the ministry has already devoted a great deal of time to clear up “misunderstandings about sukuk and terrorism” among lawmakers.

“We’ve repeatedly told them that sukuk sales have little to do with terrorist funding, and we need this bill for closer economic cooperation with the Islamic world,” he said.

The controversy has left Islamic experts dumbfounded.

“I’ve never heard this kind of ridiculous claim being made in any other country,” said Hong Seong-min, president of the Korea Institute of the Mideast Economies.

“Sukuk is just one of many financial schemes widely used around the world. I’m afraid what investors in Islamic countries will think about us if they know some lawmakers here assume their benchmark financial instrument is somehow linked to terrorism.”

A growing number of countries, including Britain and Thailand, have made legal changes to allow the issuance of sukuk bonds and to attract wealthy investors from the Middle East and elsewhere in the Muslim world.

“More and more Western countries and companies are trying to gain access to the previously untapped pool of investors by conforming to Shariah [Islamic law] and sukuk is one of the signature products, accounting for more than 80 percent of Islamic financial schemes,” said Kim Han-so, a research fellow at Korea Capital Market Institute.

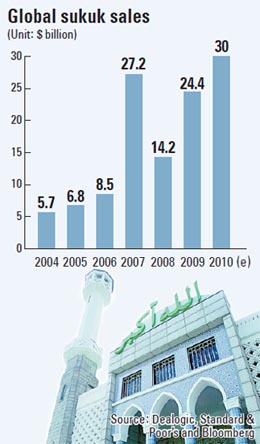

Global sukuk sales have grown from $5.7 billion in 2004 to a record $27.2 billion in 2007 and $24.4 billion in 2009, according to Dealogic, a market analysis firm, and data complied by Bloomberg.

GE Capital last November became the first Western multinational to issue Islamic bonds, completing a $500 million sukuk issuance. Japan’s Toyota Capital raised $300 million from a sukuk issue in 2008.

The interest of Korean companies in sukuk bonds has grown after the difficult borrowing conditions they experienced during the 2008 global financial crisis.

“The companies are beginning to realize the Islamic world can be a good alternative financing market,” said a local brokerage representative who declined to be named. “They started to consider the option seriously since 2008, asking us about the opportunities constantly.”

Companies that are seen as the keenest issuers of sukuk bonds include oil refiners that import crude oil from the Middle East, state-affiliated energy groups with business in the region and airline operators like Korean Air.

The legislative deadlock also is dealing a blow to Korean brokerages like Korea Investment & Securities and Daewoo Securities that want to arrange sukuk issues and have met with potential investors in the Middle East and Malaysia, which has the world’s largest sukuk bond market.

“Islamic investors who have recovered from the Dubai World debt crisis are again on the lookout for new investment opportunities and their interest in Asian borrowers, especially from Korea and China, have dramatically increased,” said Lee of Korea Investment. “This year would have been an excellent time to make a market debut.”

Moreover, Korean companies worry that if the sukuk law is delayed further they will have to contend with a crowded market for Islamic bonds in the next several years.

Standard & Poor’s this month estimated that the sukuk market could reach $30 billion in 2010. The supply of sukuk bonds could soon outstrip demand, which would drive bond rates higher and discourage Korean companies from tapping the Islamic market.

“The sukuk sales plan looked quite plausible back in 2008,” said an official with a local oil refiner. “But U.S. dollar financing conditions have improved and Islamic bond financing costs are probably higher than conventional bond rates. It’s not worth the hassle anymore.”

Nonetheless, analysts say Korean companies have to broaden their investor base to improve their access to a wide variety of financial markets.

Entering a new bond market requires months, or even years, of preparation to win the confidence of investors and negotiate favorable terms. State companies like Korea Development Bank or Korea Electric Power Corp. have played such frontier roles in global bond sales, paving the way for private sector companies.

“You can’t complete this complicated, lengthy process when the next crisis dawns on you. It has to be done when we have the luxury of time and energy,” said Lee of Korea Investment.

Kim of Korea Capital Market Institute says the political controversy over the sukuk bonds is quite contradictory to Korea’s self-proclaimed goal of becoming an Asian financial hub.

“The Islamic financial market will become a major pillar of not just the Asian economy but the global economy. Yet we’re having this petty, ridiculous dispute in even taking the first basic step to gain access to the market,” said Kim. “This is something that makes a mockery of us to Islamic investors and they have a very good reason for thinking so.”

The legislation on sukuk bonds would make minor changes in the tax code by exempting certain taxes on transactions related to their issuance. Sukuk bonds are structured to conform with Islamic law, or Shariah, which prohibits the use of interest-bearing securities. A sukuk bond differs from a conventional corporate bond by collecting a stream of income from a group of underlying assets instead of bearing an interest rate.

Under current law, a sukuk bond would be subject to a variety of taxes, including value-added tax and an acquisition tax, on what is considered a transaction dealing with tangible assets. These additional taxes would raise the financial cost of sukuk bonds by 1.5 to 3.4 percentage points above that of conventional bonds, making them unattractive to investors.

“The tax break would create a level playing field,” said Kim at the Korea Capital Market Institute.

Na on the taxation subcommittee still believes that, “we will definitely pass the bill, once the election is over, since consensus has been built.”

By Jung Ha-won [hawon@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)