Brokerages and insurers looking for answers

Labor unions from brokerage firms protesting in front of the Korea Exchange in Yeouido, Seoul, on July 2 over the ongoing corporate restructuring at brokerage firms, which have seen their profits shrink significantly in recent years as stock transactions have fallen.[NEWS1]

Those words were part of a joint leaflet distributed this month by the Korean Finance and Service Workers’ Union and labor unions of 16 brokerages.

The leaflet was handed out to pedestrians in front of Korea Exchange headquarters in the nation’s financial district Yeouido, southwestern Seoul.

The leaflet also claimed the condition of the brokerage industry is far worse than that of banks and insurers.

It said that in the past two years, more than 300 branches have merged or closed and many branches are pushing employees to take early retirement.

And even though it was a workday, more than 400 employees of brokerages gathered at about 5 p.m. to protest, a clear indication of the dire straits in which the industry finds itself.

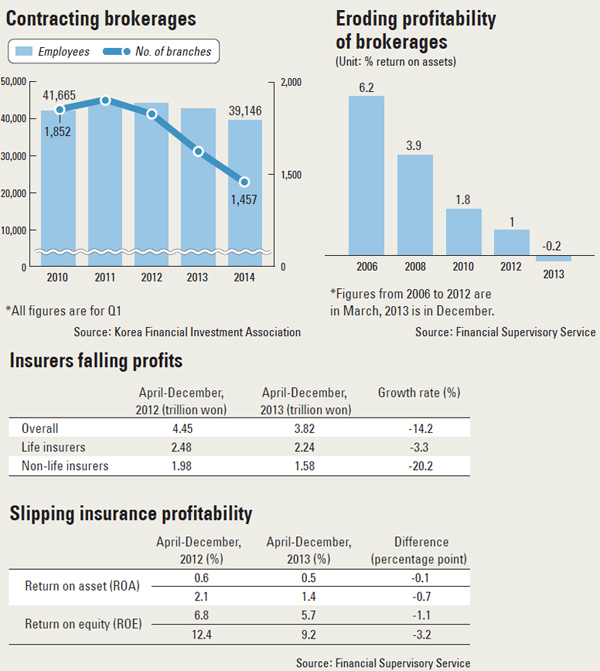

Struggling brokerages

Brokerage firms, which generated 2.8 trillion won ($2.8 billion) in net profit in 2010, lost 109.8 billion won last year. While a handful of brokerages managed to post a profit, the vast majority of smaller and midsize houses were neck deep in deficits. And credit agencies were busy lowering the ratings of Korean brokerage firms.

In the first half of 2014, 666.8 trillion won worth of stocks were traded, down 12.5 percent year-on-year. Trading hit a high note in the second half of 2011 with 1,142.6 trillion won worth of stocks bought and sold. Since then, it has all gone downhill.

The smallest commission on stock trades was 0.025 percent in the early 2000s, but that has fallen to 0.01 percent today.

Even fund sales, the chief alternative source of revenue for brokerages, have been struggling.

According to CEO Score, a management performance evaluation company, as of the end of April, active fund sales by the top 10 brokerage firms in the country were shy of 15 trillion won, nearly 2 trillion won less than the same period last year.

Market experts say investors have been shifting away from fund investments because brokerage firms failed to follow up and actively manage the funds after creating them.

At the same time, brokerage firms weren’t able to penetrate areas such as private banking and mergers and acquisitions that have been the specialty of foreign investment banks.

Invest Chosun identified the foreign brokerage Deutsche Securities as leading the local M&A business with a market share exceeding 27 percent. Among local brokerage firms, Woori Investment & Securities was the leader with a market share of 1 percent. Overall, Woori ranked 12th.

The number of analysts is shrinking as well. As brokerages struggle to cut costs, typically one of the first moves is to reduce the number of analysts, who are highly paid.

According to the Korea Financial Investment Association (Kofia), at the end of May, there were 1,276 analysts at brokerage companies, compared with 1,580 in February 2011.

Woori Investment & Securities has the largest number of analysts at 86, while 23 brokerage firms have fewer than 10 analysts.

Taurus Investment & Securities has nine analysts, while Bookook Securities has seven and Golden Bridge Investment and Securities has two.

In the past, the work of analysts and researchers gave brokerages an important competitive edge. With their numbers declining, so have the quality of service and profits.

As a result, there already has been speculation that major M&As will sweep through the industry.

“While the market is contracting, the number of brokerage firms has increased, and as a result the industry is heading toward a situation where brokerage firms are entering a game of chicken with each other,” says Won Jae-woong, an analyst at Tongyang Securities. “There’s a possibility that an environment where major brokerage houses will be in a better position, like in Japan, will be formed as the polarization of income [between small and midsize brokerage firms and larger brokerage firms] widens rapidly.”

Some in the industry say M&As of Korean brokerage firms will lack appeal for a variety of reasons.

“Analyzing M&As of brokerage companies since 2000 showed that the synergy created is barely visible and it even hurt the stock values of the company,” says Jang Hyo-sun, an analyst at Samsung Securities. “If a company with no experience in this field took over a brokerage firm, not only would it have problems creating synergy, but also its efficiency would fall because of the hardcore labor union. And therefore the M&A of a brokerage company won’t be easy.”

Tough times for insurers

In the insurance industry, the situation isn’t much better.

At Kyobo Life Insurance, 480 employees who had worked for the company for more than 15 years were sent into early retirement, 180 more than initially estimated. The number of people who retired equals roughly 10 percent of the total work force of 4,700.

At Hanwha Life Insurance, 300 employees retired early, and the situation is the same at other companies, including Samsung Life Insurance, as a result of declining revenue and a halving of profits.

Among all insurers, life insurance companies are in the worst situation.

According to the Financial Supervisory Service, the net profit of life insurers from March through December last year slid 9.3 percent compared to the same period in 2012. Operating profit plunged 42.4 percent year-on-year.

Despite the critical situation facing the industry, life insurance companies have failed to find a way to turn around a situation that many experts say is largely of their own making.

High interest products the companies have been marketing since the early 2000s are now choking profitability as the nation is stuck in a prolonged low interest environment.

According to the financial industry, insurance contracts with fixed interest rates of 6.5 percent or higher accounted for 27.2 percent of all contracts, or 110.3 trillion won. On the contrary, the asset management interest of insurance companies is in the 4.4 percent range. This means payments to clients are more than investment income.

Experts say the current situation is similar to what Japanese life insurers faced in the 1990s. Because the Japanese were passive about low interest rates and low growth, seven life insurance companies starting with Nissan Mutual Life Insurance filed for bankruptcy over a period of five years.

Life insurance companies are largely in trouble because they have managed their assets conservatively, allocating most in bonds.

According to Meritz Securities, 66.7 percent of the managed assets of life insurance companies is tied up in bonds. Insurance companies, in hopes of increasing the profitability of their managed investments, recently have been trying to acquire other financial companies and expand overseas real estate investments.

Hanwha Life Insurance spent 250 billion won to buy the headquarters of international law firm Eversheds in London, and 13 other Korean insurance companies, including Shinhan Life Insurance and Kyobo Life Insurance, recently joined Shinhan Bank’s private debt fund worth 600 billion won.

The problems that non-life insurance companies face are not as serious as those of life insurers, which are saddled with long-term products. Additionally, the loss ratio for car insurance, which was a huge burden for non-life insurers last year, has eased.

The loss ratio at Samsung Fire and Marine Insurance, which has the largest number of car insurance policies, in the first quarter was 79.4 percent. This is a 0.2 percentage point drop from the previous year.

Hyundai Marine and Fire Insurance’s loss ratio fell 1.5 percentage points from last year to 83.7 percent. Most of the non-life insurers’ loss ratios were more than 85 percent.

The loss ratio is the percentage of premiums that is paid out in settlements. The non-life insurance industry estimates the most appropriate loss ratio to be 77 percent. The loss ratio, however, improved not because these companies are doing well but because rates were raised for owners of high-end imported cars.

When looking at asset management performance, there is little difference between non-life and life insurers. An evaluation by the Korea Deposit Insurance Corporation showed that last year, the profit rate in asset management of non-life insurers was 4.03 percent. This is 0.04 percentage point lower than the burden rate of 4.07 percent that non-life insurance companies have to burden on the long-term insurance policies.

Experts say insurance is a business that generates income through management of risks, and new products are possible only when companies set the price of policies based on risk evaluation. However, they say the local insurers, instead of honing risk-management and evaluation skills, tend to rely too much on income from setting high premiums for policies. This is partly due to complex regulations of the financial authority that indirectly affect the price-setting process.

“Foreign insurers set their own price from the value of the policy to the cancellation fee and so forth, and then when they commit illegal activities such as fixing prices, they get severely punished,” says Jeon Yong-sik, a Korea Insurance Research Institute analyst. “There is a need to reduce regulations that inhibit competition so that the abilities of insurers are distinctively visible through competition.”

BY LEE SOO-KI [ojlee82@joognang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)