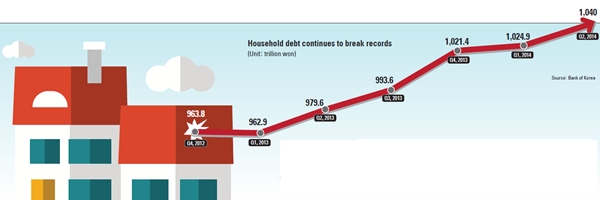

Second-quarter household debt hits 1,040 trillion won

Yet market experts expect household debt to further expand for the near future thanks to the government easing mortgage loan regulations and the central bank cutting its benchmark rate earlier this month. There are growing expectations the central bank may further cut the key rate as early as September to further encourage lending.

The government downplayed concerns about outsized leverage, saying the pace of growth hasn’t risen to an alarming point and the quality of debt is improving.

Data provided by the Bank of Korea yesterday indicated household debt shows no signs of slowing as it heads toward 1,100 trillion won. In just six months since it first broke the 1,000 trillion won mark, household debt is just inches away from the 1,050 trillion won level. Household debt, excluding credit cards, experienced year-on-year growth identical to overall household debt at 6 percent.

“The main reason household debt has further expanded is because some banks have increased lending, which consists of fixed and variable interest rates, in order to comply with the government’s policy of increasing fixed-interest loans,” said a BOK official.

In order to improve the quality of debt, the government since the last year of the Lee Myung-bak administration in 2012 has pushed to expand fixed-interest loans to buffer any market insecurity that could surface from tightening the nation’s monetary policy by raising the key interest rate.

Considering that the figure included only existing loans through the end of June, it is likely to spike in the third quarter.

The central bank this month already cut the nation’s key interest rate from 2.5 percent to 2.25 percent, the lowest in 4 years, to support the aggressive campaign to bolster the economy by Deputy Prime Minister and Finance Minister Choi Kyung-hwan.

Although there are still debates on the need for another rate cut, the market is responding to the recent changes - rate cut and eased mortgage regulations.

According to Standard Chartered Korea, since the government altered the debt-to-income (DTI) and loan-to-value (LTV) ratios, new mortgages more than tripled in the first 22 days of this month compared to July.

The bank said that so far this month, there have been requests for 927.5 billion won in mortgage loans, which is far more than the 313.7 billion won sought in July. It added that roughly 85 percent of those who asked for fresh loans received the maximum LTV ratio of 70 percent.

“As customers who have no overdue payments on other loans or credit card payments are eligible for the maximum 70 percent LTV ratio when applying for loans, we expect the number of applications to increase,” said Park Jong-gwan, who is in charge of retail lending at Standard Chartered Korea.

As there seems to be no factors that would curb continuous expansion of debt, some have argued that the growing debt could actually have a negative effect on the market.

Korea Development Bank in June released a study that argued the debt size has reached a near-critical point where consumers may reduce their spending.

Nomura Securities earlier this month released a similar statement, saying excessive debt in the long run could undermine the positive influence of the lowering of the key interest rate earlier this month.

“The government also should not ignore the fact that without proper management and control of the debt, excessive leverage could end up very much like the U.S. mortgage crisis in 2007 and 2008, where people borrowed more than the actual value of the property and ended up with huge debts,” said a market analyst who requested anonymity. “The policies should first be focused on increasing income rather than encouraging people to spend by borrowing.”

In fact, studies show that while household debt last year grew 6 percent, disposal income grew at a rate of 2.9 percent.

In a release yesterday, the Financial Services Commission (FSC) underplayed such concerns, saying even after the LTV and DTI were eased household debt is growing at a moderate pace.

The financial authority said that in the first 22 days of August, 2.4 trillion won worth of fresh loans was borrowed by households. That’s nearly equivalent to the monthly average of 2.7 trillion won from January through July.

Additionally, it stressed that the quality of debt was improving, citing the shift in the type of institutions where people are borrowing.

The FSC said those who previously would have had no other choice than to borrow from nonbanking financial companies at higher interest rates have mostly changed course to apply for loans at banks due to the relaxed regulations.

That, it said, lowers the financial burden of interest payments and reducing the overall risk of defaults.

The risk has further been lowered by the increased emphjasis on safer mortgages such as those with fixed interest rates, the FSC said. Mortgages with fixed-interest loans at the end of June accounted for 17.9 percent of all mortgages, a 2 percentage point increase from end of March. This is a significant increase considering such loans only took up 3 percent at the end of 2011. Additionally, installment payment mortgages that pay both the principal and interest simultaneously now cover 21.6 percent of all mortgages. This exceeds the government’s goal for this year of 20 percent.

“In the overall management of household debt, there were no visible signs of a major crisis and the effect of the [debt] quality structure is gradually showing,” said a FSC official.

“In particular, the key interest rate cut will further ease the interest payments of debtors.”

Even BOK Governor Lee Ju-yeol, during a press conference held after the monthly monetary policy committee meeting held earlier this month, said household debt was not at a critical level, although acknowledging the rate cut would further increase household debt.

“One needs to also consider the increase in income when looking at the absolute size of debts,” said Lee, stressing throughout press conference the need to put the rejuvenation of the economy first.

BY lee Ho-jeong [ojlee82@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)