Fundamental look at Korea economy

Published: 28 Aug. 2011, 23:04

The intense jolting of Korean markets forced the government to stress that the economy was fundamentally strong, and it strenuously denied the likelihood of a double dip recession in the global economy.

Many analysts agreed that compared to 2008 or the near collapse of the economy in the late 1990s, Korea’s economy was solid.

However, they note that there are lingering uncertainties about Korean economic growth. The biggest worry is that a contraction of the global economy could hurt Korea’s export dependent economy. But fiscally, Korea’s debt remains sound compared to other developed countries.

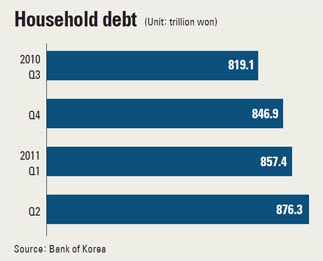

A sluggish domestic market and possible capital outflows could dent the economy, while high consumer prices and a large amount of household debt are possible problem spots.

Current account balance

The Finance Ministry stressed that in 2009, Korea’s current account posted a $32.8 billion surplus and last year it was $28.2 billion. This year the government estimates a current account surplus of more than $16 billion.

However, some analysts say that considering Korea’s external debt amounts to nearly $400 billion with an interest rate of 4 percent, a drop in the current account balance could result in the nation’s credit rating being downgraded.

The external debt is nearly 40 percent of the nation’s gross domestic product of $1 trillion. At 4 percent, the country would have to pay $16 billion in interest. This could come as a burden to the government if the current account balance shrinks or goes into deficit.

The Korea economy has long been export dependent, and that has increased since the global crisis of 2008.

“Since the 2008 crisis, Korea has shown solid growth centered on exports,” said Jeong Young-sik, Samsung Economic Research Institute researcher. “Global economic growth is slowing down and Korea’s momentum could slow down due to the recent financial uncertainties.”

JP Morgan earlier this month lowered its growth projection for the U.S. third quarter from 2.5 percent to 1.5 percent.

According to Bank of Korea, a 1 percentage point drop in the U.S. economy translates into a 0.4 percentage point drop for the Korean economy and a 0.2 percentage point increase in consumer prices.

Samsung Economic Research Institute earlier this month estimated that the Korean economy could see a dip in growth of 0.2 to 0.3 percentage points from its previous projection of 4.3 percent. The government is targeting 4.5 percent growth this year.

Adding to the burden is the appreciation of the Korean won. Many research institutes and the government earlier this year estimated the won would hover around 1,100 won to the greenback. The currency at one point hit the 1,050 won level. It recently hit 1,080 won to the dollar, below earlier predictions.

A strengthened won hurts exporters and also the nation’s ability to repay external debts.

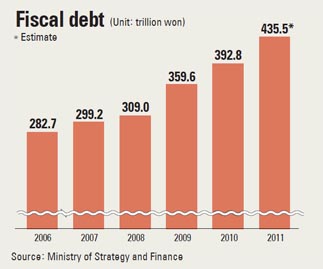

Fiscal debt

According to the Organization for Economic Cooperation and Development, Japan’s fiscal debt as compared to its GDP is expected to reach 204.2 percent by the end of this year and 210.2 percent in 2012. This is even worse than the U.S.’ 98.5 percent, Greece’s 136.8 percent and Ireland’s 112.7 percent.

Korea’s fiscal situation is relatively sound. According to an estimate by the OECD in June, Korea’s fiscal position is the third best among 24 member nations, trailing behind Australia and New Zealand.

The government is currently planning to lower the debt-to-GDP ratio to 31 percent. Last year, debt accounted for 33.4 percent of GDP. This year, the government estimates the ratio to 33.3 percent and predicts ratios of 33.4 percent for 2012 and 33.8 percent for 2013.

Last year the nation’s fiscal debt was at 392.8 trillion won ($363 billion).

In a report, the OECD noted that the Korea has limited the increase of central government spending to 5 percent per year.

However, over the years the debt ratio has grown rapidly. In 2002, the debt ratio was 18.6 percent of GDP, and it exceeded 20 percent in 2003 and 30 percent in 2006. In 2009, the debt rose sharply to 33.8 percent, largely from the government stimulus package in the wake of one of the world’s worst financial crisis in 2008.

In the first half of this year, the fiscal deficit exceeded 19 trillion won. Although small compared to the 29 trillion won deficit posted in the first half of last year, the deficit for first half is nearly 80 percent of the government target of 25 trillion won.

Some analysts say the situation will get worse if the economy slows down. Tax revenues will shrink and the fiscal debt could exceed the government target of 25 trillion won.

“Fiscal soundness deteriorates at an alarming speed when problems within the country are combined with external shocks,” said Kim Deuk-gap at Samsung Economic Research Institute. “Therefore it is important to work on managing the nation’s fiscal situation before the country is faced with a situation it cannot control.”

Expanding the domestic market

The role of the domestic market in Korea’s economic productivity has been backsliding for 40 years. The contribution of consumer spending to Korea’s real gross domestic product fell to 51.5 percent in the second quarter, the second-lowest level ever recorded following the first quarter’s 51.4 percent.

The domestic market once reigned supreme, contributing 84.1 percent to real GDP in the first quarter of 1970. But as Korea’s economy skewed toward foreign trade, that number fell to 59.4 percent in the second quarter of 1997 and has remained in the 50 percent range ever since.

And consumer spending is showing signs of slowing. According to the latest data from the Bank of Korea, growth in consumer spending has steadily fallen from 3.6 percent in the last quarter of 2010 to 2.9 percent and 2.8 percent in the first two quarters of this year. This has led the central bank to revise its outlook on consumer spending growth from 3.5 percent to 3.3 percent.

“Because our economy depends on the export market, Korea’s GDP growth slows down whenever exports waver,” said Lim Hee-jeong of Hyundai Research Institute. Analysts say that to maintain economic growth the domestic market should pick up the slack for the troubled export sector.

A focal point in developing the domestic market, analysts said, is bolstering the services sector. But a decade of attempts by the government to do that have faltered due to restrictive regulations that protect established companies in the services sector.

Korea’s services sector accounted for 58.2 percent of GDP in 2010, falling behind the 69.2 percent OECD average as of 2007 and backsliding from 60.8 percent in 2008.

Moreover, the current services sector is skewed toward comparatively simple, lower value-added businesses. According to a Korea Development Institute report released this month, some 22.9 percent of Korea’s services sector consisted of wholesale and retail, food and lodging services, while health, medical and social services only accounted for 4.8 percent of the sector.

“There needs to be improvements in the competitiveness of the pillars of the services industry, including medical, legal and financial services,” said Jeong of Samsung Economic Research Institute. “The quality of the domestic services industry must further rise in order to keep money within the domestic market and not have it drain out overseas.”

Progress has been slow due to existing players zealously guarding entry barriers that impede new companies from forming.

A recent clash over entry barriers took place between the government and the Korean Pharmaceutical Association (KPA) over allowing over-the-counter drugs to be sold in supermarkets.

The Ministry of Health and Welfare’s foot dragging due to the considerable lobbying power of the KPA’s 30,000 paying members only came to an end when President Lee Myung-bak rebuked the Health Ministry, saying that the public’s convenience should take precedence over protecting the pharmacies.

Although the over-the-counter debate ended with eased entry barriers, analysts say the controversy was just the tip of the iceberg, with countless more industries needing shaking up.

“A new approach to entry barriers is needed,” said Shim Young-sup of the Korea Institute for Industrial Economics and Trade.

The government has declared that revitalizing the domestic market is one of its key goals during the second half of the year, and it announced in July 66 measures.

Staunching capital outflow

Ever since the global financial market was hit with turbulence in August, much has been said about foreigner investors’ mass exodus from the local stock market, which helped push the benchmark Kospi into bigger drops than in the U.S. or Europe. But staunching an outflow of foreign capital during a global financial shock is a conundrum not just for the stock market, but also for bonds and other foreign currency debt.

According to the latest BOK data, foreign investors’ net selling of Korean bonds reached $500 million between Aug. 1 and Aug. 18.

The selling streak - offset somewhat by substantial purchases from emerging economies - was chiefly driven by European investors, particularly French banks, which sold some $1 billion in Korean bonds during the same period.

If the trend holds for the rest of August, foreigners would have net sold Korean bonds for the first time in seven months, as European money quickly recedes from Korea and other emerging.

Such outflows of capital were most dramatically seen in the stock market, where foreign investors sold some 5 trillion won or 86 percent of their net sales this year in Korean shares since the start of August. That phenomenon has been dubbed by the local media as the “ATM Korea” effect: foreign investors using Korea’s highly liquid market to withdraw money every time they are spooked by worldwide economic conditions.

Government officials and analysts say that remedies are somewhat clear-cut. For Korea’s foreign currency debt such as bonds, shifting the sources of Korea’s financing beyond the epicenters of the current global financial trouble, such as Europe and the U.S., to emerging economies is recommended. For the stock market, increasing the role of pension managers and other institutional investors is being called for.

However, these remedies have been common knowledge since the 2008 financial crisis, but nobody did much to institute them.

For example, the government has a task force to consider ways of attracting Middle Eastern funds to Korea under orders from President Lee to diversify the source of Korea’s finances.

“Financing is all about networking skills,” said a high-ranking Financial Services Commission official. “Because Korea’s funds mostly came from U.S. and Europe until now, that’s where our networks have concentrated in. The task force is reviewing ways to increase our networks in the Middle East.”

But drawing Middle Eastern oil money to ensure financing when U.S. and European investors pull out from Korea is not a new idea.

Attempts had been made since 2008, when Korea joined the Islamic Financial Services Board and pursued the passage of a bill to allow tax exemptions on Islamic bonds or sukuk in 2009, to level the playing field with foreign currency bond trading, which is already exempted from several taxes. However, passage of the sukuk bill remains stalled due to political opposition led by Christian leaders.

Although experts note that the government’s new focus on securing oil money apart from sukuk is a positive sign, gaining the networks necessary to draw Middle Eastern funds away from established channels will be difficult.

“Middle Eastern sovereign wealth funds already have a long tradition of investing in advanced economies,” said Hong Seong-min, head of the Korea Institute of the Mideast Economies. “Korean banks will have to go head-to-head with Western financial heavyweights to attract funds.”

As for the stock market, the government wants certain institutional investors to act as buffer to foreign selling.

“In order to increase the security of our volatile stock market, pension managers and public funds must increase their stock holdings,” said Kim Seok-dong, FSC chairman.

However, the government has emphasized that the final investment decision is up to pension managers and the funds themselves and has shied away from official intervention to avoid a backlash should pensions and public funds lose money on stocks.

But there are a few positive signs. Although European banks have been selling Korean bonds in August, the effect was offset by hefty purchases from Chinese investors, including the People’s Bank of China, signaling an increasing role comparatively high-growth economies and emerging nations can play in the local economy.

By Lee Ho-jeong, Lee Jung-yoon [ojlee82@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)