Ability of young households to save is eroding

“Out of what my husband and I earn every month, we spend a large portion on paying back the interest of loans we received to live on jeonse [lump sum deposit],” Park said, with a sigh. “On top of that, we spend about 500,000 won ($443) every month on food and groceries and 200,000 won on average on flat maintenance.”

Sounding depressed, Park said over the phone that she isn’t able to put even a penny into a fixed deposit account or installment savings.

She isn’t alone.

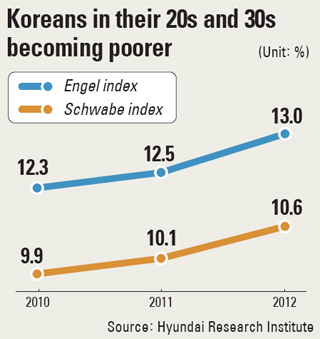

According to a report released yesterday by the Hyundai Research Institute, Korean households led by breadwinners in their 20s and 30s are experiencing increasing hardship as their spending on food, housing and maintenance fees keeps going up. The report showed that the Engel index, which measures the percentage of household income spent on food, for Koreans in their 20s and 30s jumped from 12.3 percent in 2010 to 13 percent in 2012. The Schwabe index, which measures how much households spend on housing and other standing charges like electricity, went from 9.9 percent in 2010 to 10.6 percent in 2012.

For people in their 40s and 50s, the Engel index was 13.2 percent in 2010 and 13.3 percent in 2012, while their Schwabe index in 2010 was 9.4 percent and 9.6 percent in 2012.

The institute’s report noted that the higher increase in indexes for young people is mainly due to the high unemployment rate and rising interest burden.

“The number of double-income households led by Koreans in their 20s and 30s dropped last year because it has become more difficult to find jobs,” said Kim Pil-soo, a senior researcher at the institute. In 2009, 35.4 percent of households in their 20s and 30s were double-income households. In 2012, however, the portion was 32.9 percent.

Kim pointed out that the government plays an important role in providing young families with the opportunity to accumulate assets that are the foundation for future consumption of goods and services.

“For example, the government should expand the target group for those able to sign up for property accumulation savings products [that offer higher interest rates] so they’re able to save up their money,” he said.

Currently, salaried workers with less than 50 million won in annual income are eligible.

By Lee Eun-joo [angie@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)