Government targets debt

From left to right: Choi Soo-hyun, Financial Supervisory Service governor; Shin Je-yoon, Financial Services Commission chairman; Hyun Oh-seok, minister of strategy and finance; and Yeo Hyung-koo, vice minister of land, infrastructure and transport explain initiatives to ease household debt.

“The government in recent years has acted to decelerate household debt growth to reduce potential risks to the overall financial market, as well as the economy,” said Financial Service Commission Chairman Shin Je-yoon during a joint briefing yesterday at government offices in downtown Seoul. “However, it is still pointed to as a major risk factor. The debt size is very large compared to other major economies and our credit rating is vulnerable to external risks as long as debt continues to expand faster than income.

“Under such circumstances, it will be difficult to expect the domestic market to become active.”

The government plans to encourage debtors to switch from variable rate loans to fixed interest loans. In addition, the government will try to get debtors to switch from balloon loans, in which only interest is paid for a set period prior to a single large principal payment, to loans in which interest and principal are amortized monthly over a longer term.

Many people who took out mortgages in the mid-2000s, when the property market was reaching its peak, were on balloon payments with variable rates.

Their low, interest-only payments have been coming to an end and their burden has increased due to high principal payments. The government hopes to ease this burden by spreading out monthly interest plus principal payments.

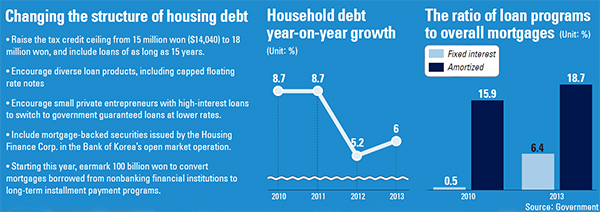

The government said it plans to raise the share of fixed-interest and long-term amortization loans to 40 percent of all mortgages by the end of 2017.

So how to attract people to convert to fixed interest or long-term amortization products?

The government will also boost tax incentives, Currently, the tax credit on fixed-rate mortgages is 15 million won ($14,022). This will be raised to 18 million won.

Other measures feature diversification of debt products, such as capped floating rate notes that limit variable rates, while including mortgage-backed securities in the Bank of Korea’s open market operation that controls money supply and short-term interest rates. It currently includes only government bonds and monetary stabilization bonds.

This includes encouraging owners of small businesses who have taken out loans from nonfinancial companies with interest rates of more than 20 percent, to access government-backed loan programs with rates between 11 and 15 percent.

These loan programs previously were available only for those with small loans with interest. But the government will make them available to those paying interest rates of 15 percent or higher.

For the first time, the government will earmark 100 billion won to convert mortgages borrowed from nonbanking financial companies with higher interest rates to long-term amortization loans.

Although the FSC chairman acknowledged that most of yesterday’s measures were similar to ones issued under the Lee Myung-bak administration in 2011, he said the new measures are largely focused on readjusting the debt burden for homeowners with poor credit ratings.

As of the end of 2013, household debt, including credit card purchases, has reached a record 1,021 trillion won. The overall growth rate has been decelerating, but it also showed that while mortgage loans account for half of household debt, many have borrowed from financial institutions to pay living expenses and regular recurring bills.

The deteriorating quality of Korean household debt has been exacerbated by levels of debt that are rising faster than income.

The disposable income to debt ratio in the United States before the housing crisis in 2007 and 2008 was about 140 percent. Korea’s disposable income to debt ratio currently exceeds 160 percent, which has been raising eyebrows.

The government said that if the measures are executed properly as it hopes they will be, Korea’s income to debt ratio will fall roughly 5 percentage points by 2017.

“From the standpoint of consumers, variable interest rate loans represent a huge risk of a higher burden in the future,” said Shin. “In the long run, fixed rates will not only help a person manage his debt but also his assets.”

BY LEE HO-JEONG [ojlee82@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)