Local banks turning toward fintech

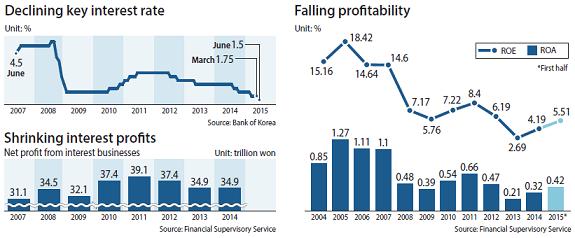

Seven months ago, the central bank lowered the key interest rate to below 2 percent for the first time ever. Four months ago, the rate was cut even further, to 1.5 percent.

The moves are a continuation of the loose monetary policy of recent years aimed at keeping the Korean economy afloat.

But those same moves have dealt devastating blows to local banks’ profitability - and things could get even worse. Although the Bank of orea announced Thursday that the key rate would stay frozen for another month, speculation continues about another rate cut, since the U.S. Fed’s interest-rate hike is unlikely to be seen within the year.

This isn’t the first time the banking industry has found itself in trouble - and in need of reform.

After the Korean financial industry was overhauled in the wake of the Asian financial crisis of the late 1990s, the banking industry sought to adapt to a changing landscape by diversifying revenue sources and expanding overseas.

The industry had ambitions of becoming the financial hub of Asia.

Nearly two decades have passed, and little progress has been made. In fact, there wasn’t a single Korean bank among the world’s top 50 financial institutions as ranked by British financial magazine The Banker. The state-owned Korea Development Bank ranked highest among Korean banks at 62, followed by KB Kookmin Bank at 65 and Shinhan Bank at 69.

China, on the other hand, had four banks in the top 10.

It seems unlikely that the Korean financial industry will see a turnaround soon, as it’s currently faced with its biggest challenges to date: a rapidly aging society, perpetual low growth and an era of interest rates low enough to threaten both its existing profitability and ability to maintain sustainable growth.

The only way out is through innovation, and while many of the strategies being proposed are familiar - namely expanding overseas and diversifying revenue sources - there is a new addition: financial technology, or fintech. Local banks are partnering with tech firms to integrate traditional financial services with IT in ways that could create new markets.

Post-meltdown slowdown

The banking industry enjoyed exceptional growth from the mid-2000s until the global financial meltdown in 2008. This was largely due to overall economic growth and a hot property market that encouraged both households and businesses - particularly those in big-money sectors like construction and shipbuilding - to take out huge loans despite high interest rates.

Before the global crisis, the average interest rate on household loans peaked at 7.19 percent, with corporate loans at 7.17 percent. The rates were the highest in recent years, even though the average household rate was less than half of the 15 percent recorded in the late ’90s.

Since the 2008 crisis, however, the banking industry hasn’t been able to shake a period of low growth. Today’s interest rates are half of what they were before 2008. As of August, the interest rate on household loans was 3.13 percent, while the average for corporate loans was 3.57 percent.

Interest rates have been continuously falling since mid-2014, remaining in the 3 percent range.

Another area of concern has been banks’ assets, which hit a record high of 14.6 trillion won ($13 billion) in 2008. In 2012, overall assets fell to as low as 2.2 trillion won.

Although assets did expand 66 percent year on year in 2014, the growth was largely attributable to the government’s deregulation of property loans, as well as the two interest rate cuts pushed by the central bank in the second half of the year.

Banks have also seen their net revenues decrease.

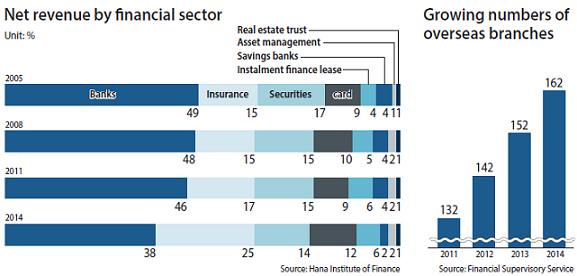

For banks, net revenue consists of the profit made from the difference between earnings on loan interest and payouts on deposit interest, as well as the profits from non-interest related sectors such as service commissions. Ten years ago, banks’ net revenue accounted for 50 percent of all earnings in the financial industry. But last year, it was just 38 percent of total earnings, according to data released by the Hana Institute of Finance.

The fall has been attributed to the low interest rates and the nation’s rapidly aging population, which has triggered clients to shift their investments - particularly retirement funds - to the insurance market, which is more stable and offers larger tax benefits.

Profitability of local banks has also been on the decline. Banks’ return on equity (ROE) in 2005 was 18.4 percent. But in recent years, ROE has been stuck below 2 percent.

As a result, the net profits of Korea’s 17 banks, which hit a five-year high of 14.5 trillion won in 2011, fell as low as 4.49 trillion won in 2013. Net profits recovered slightly last year to 6.84 trillion won.

“The financial industry will continue to defend its profit rate, but without a special opportunity presented, the current trend won’t be easily hanged,” said Sohn Joon-beom, a senior analyst at the Hana Institute of Finance. “Banks’ core profits will have trouble expanding because of the net interest margin … which has decreased due to the two interest rate cuts made by the central bank earlier this year.”

Experts say it is critical for local banks to make changes to their revenue structure, which currently relies on interest income for roughly 90 percent of revenue. The interest-driven business model is becoming out of date, particularly at a time when the key rate is below 2 percent.

Many of the strategies being proposed are familiar, including expansion into overseas markets and the diversification of revenue streams. But the moves that have been making recent headlines have had to do with new partnerships between local banks and tech firms worldwide.

Innovations for the future

Fintech provides opportunities for new markets, but also signals challenges ahead for local banks.

According to a report by consulting firm McKinsey last month, developments in fintech will likely reduce the net profits of the world’s banks by as little as 20 percent to as much as 60 percent, affecting their businesses in mortgages, loans to small and midsize businesses and asset management in the next 10 years. In the case of retail loans, including mortgages, net profits will see a 60 percent cut, while revenue will be down 40 percent.

The shrinking profits will be mostly caused by cuts in service charges, wrote analyst Philipp Harle in the report. Technology companies will be able to offer the same financial services at lower costs, and those tech companies will be targeting banks’ areas of biggest profits.

The banking industry will have to choose whether or not to jump on the fintech wagon within the next three years, “or the choice will be made for them,” Harle wrote.

But local banks are trying to take advantage of the opportunities posed by integrating their existing services with new technologies.

One example is the advent of the so-called Internet bank. The idea is to create banks that offer traditional services like deposits, loans and other financial services, but exist only online. By doing away with physical branches, Internet banks cost much less to operate, and those savings can be passed on to consumers.

Earlier this month, KB Kookmin Bank, Woori Bank and the Industrial Bank of Korea partnered with IT companies like mobile messenger company Kakao, mobile carrier KT and Internet ticket and online shopping mall Interpark to submit applications to create the nation’s first-ever internet bank.

The Financial Services Commission is currently reviewing the applications and will announce one or two Internet banks by the end of this year, with their debuts expected in the first half of next year.

One way Internet banks are expected to change the industry is by further concentrating customers’ financial activities on their smartphones.

According to the Bank of Korea, as of the second quarter, over 57 million people are using their smartphone for their banking - a 6.8 percent increase from the previous quarter and 32 percent increase compared to the same period a year ago.

Hana Financial Group has been one of the leading financial institutions when it comes to integrating mobile technology, as it was the first Korean bank to utilize a smartphone banking app, in 2009.

The group is working on developing new mobile technology that allows clients to accumulate points through spending money at any of its affiliates, which can then be used as cash throughout Korea, China and Japan, according to Chairman Kim Jung-tai last week.

The group is also working on expanding accessibility of its online-only banking services via mobile devices to China, Indonesia and Canada. Hana’s online services are expected to debut in China as early as this fall.

Shinhan Bank is also taking new financial technology abroad.

Last week, the bank signed a strategic alliance with Japan’s biggest mobile messenger company and Korean IT company affiliate Line, which has a mobile payment and wiring service Line Pay, to enter the Southeast Asian market.

Through the platform, users from Japan and parts of Southeast Asia will be able to withdraw cash from Shinhan Bank’s ATMs.

Line is one of the most-used mobile messenger app in Southeast Asia, as it has over 200 million monthly users in Japan and throughout Southeast Asia, including Indonesia and Thailand.

Shinhan has also been working to nurture fintech firms at home. In July, the bank selected seven prominent Korean fintech companies, providing them with financial support and consultations to further develop their designs.

Other local banks are lending a hand to existing tech companies and creating new markets in the process.

Within the same week that Shinhan partnered with Line, KB Kookmin Bank inked an alliance with Mobitle, which operates the popular app Zummaslide. The app lets users earn points by swiping through information about businesses near their apartment, which can then be used to discount their household bills.

Mobitle is currently running a test run on 93 apartment complexes with 43,000 households in Suwon and Hanam in Gyeonggi and Gangdong in southeastern Seoul. The company plans to expand its service to the rest of the greater Seoul area by next year that would cover one million households. By 2017, it hopes to secure over 1.7 million households as subscribers.

The strategic alliance with the bank will be focused on finding a new business model and securing marketing channels, including joint marketing with bank branches.

“This strategic alliance will be a good example of providing a differentiated financial service that is very closely connected to people’s daily lives,” a KB Kookmin Bank official said.

BY LEE HO-JEONG [lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)