A strong yen might be bad news

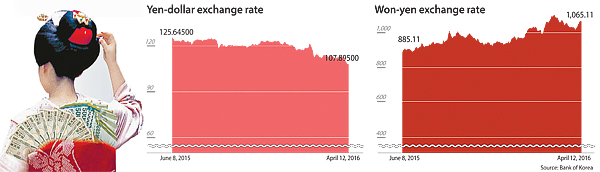

Despite the Bank of Japan’s unprecedented adoption of negative interest rates in January, the Japanese currency, which hovered around 125 yen against the U.S. dollar until last June, recently soared to around 107 yen. A new low for the currency stood at 107.91 on April 7.

Economic experts and market analysts have no disagreement about the fact that the yen has made a turnaround from depreciation to appreciation, largely owing to global funds hunting for safer assets. Slower-than-expected rate hikes by the U.S. Federal Reserve are also adding to the yen’s strengthening, making the dollar weaker.

“Since the Bank of Japan’s adoption of negative interest rates, market trust in Japanese monetary policy has been undermined, and doubts about its effect rose, making the yen appreciate,” said Park Hyung-joong, a researcher at Daishin Securities. “The yen is getting stronger due to increasing preferences for safer assets as investors’ concerns about global recovery are mounting.”

Considering that the monetary policy has lost market trust, the researcher said, additional monetary measures by the Bank of Japan will not improve the situation at all.

“Such strong preference for safe assets will mean that the prices of risky assets, especially financial assets in advanced markets, will be adjusted, and this is not a good sign for the global economy,” Park said.

About two years ago, when the yen began to go down in response to the introduction of Abenomics, there were immense worries about the falling profitability of Korean exporters, who were projected to lose price competitiveness against Japanese rivals in overseas markets.

History teaches us that a strong yen helps increase the profits of Korean exporters, and that this is an important factor for Korea’s overall growth since the Korean economy is highly dependent on exports, leading to an upbeat mood in the stock market. This could also link to a hike in the benchmark interest rate in the long run.

However, some argue that this may no longer apply. Since the strong yen is the result of global investors’ preference for safer assets, which is the exact opposite of what Abenomics aimed to achieve, how it will affect the performance of Korea’s exporters and stock market remains to be seen.

Considering that the U.S. dollar is projected to remain weak while the yen strengthens, Korean firms with Japanese rivals may breathe a sigh of relief. But weak global economic performance, including China’s slowed growth and a slower-than-expected recovery in the United States, are not going to help improve the profitability of Korean exporters.

“Because the weak yen was not a direct cause for the recent falls in Korean exports, the strong yen might not be the single factor that can ramp up Korea’s exports,” said Kim Yong-gu, a researcher at Hana Financial Investment. “So we shouldn’t get too excited about immediate improvements in the performance of exporters.”

On Korea’s monetary policy direction, the strong yen is forecast to have an effect, whether direct or not.

Considering that the yen is now attracting global investors, the Korean central bank is likely most concerned with the possible outflow of foreign capital from the local market, which is the opposite effect that a strong yen has had in the past. In this case, the Korean stock market could go bearish, increasing the need for a rate cut.

According to a report titled “A Different Angle on the Strong Yen,” released by Korea Asset Investment Securities, the probability of the Bank of Korea lowering its key rate in the near future is higher, given that the yen’s appreciation is reflecting investors’ appetite for safer assets.

“If it turns out that the yen is getting stronger because investors want safer assets, the likelihood for a rate cut gets higher,” said Gong Dong-rak, head of macroeconomic analysis at the brokerage.

“The strong yen is having different effects on the Korean stock market compared to the past, for example, when the won-yen exchange rate soared last year and stock prices of transportation equipment makers, one of the most sensitive industrial sector to the yen, declined.”

The researcher believes that the Bank of Korea will lower the benchmark interest rate by 0.25 percentage points at the upcoming monetary policy committee meeting on April 20.

On the other hand, some claim that such an unexpected appreciation of the yen could deter the Korean central bank from a rate cut if the yen’s current move is judged to be out of control of the Japanese monetary policy maker.

“The strong yen, in spite of the Bank of Japan’s negative interest rates policy, may signal that the central bank’s policy is losing market trust,” said an analyst at a securities brokerage firm. “If this perception becomes widespread, it won’t be easy for the Bank of Korea to cut its rate.”

In the March monetary policy committee meeting, the seven committee members agreed that a monetary policy decision has its limits, especially when major causes of slow economic growth are structural problems.

BY SONG SU-HYUN [song.suhyun@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)