Midrate loans gain popularity

Commercial banks, savings banks (which in Korea are more like consumer finance companies catering to low-income, bad-credit borrowers) and even credit card companies have added midrate loans to their business, aided by a government-led initiative to help those with midrange credit scores struggling to find loans.

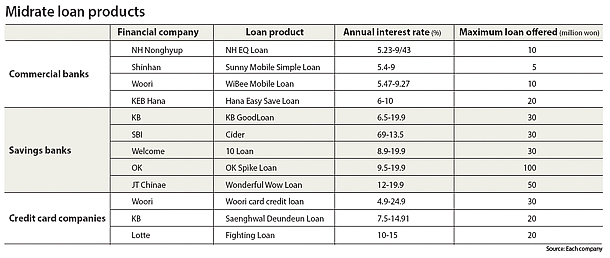

The recent trend in the market started with the country’s leading banks. Market leader Shinhan, Woori and KEB Hana Bank as well as the financial unit of agricultural cooperative NH Nonghyup Bank began offering midrate products late last year.

NH Nonghyup’s NH EQ (Easy and Quick) loan provides a maximum of 10 million won ($9,000) with annual interest between 5.23 percent and 9.43 percent. Shinhan and Woori offer similar products with an interest rate between mid-5 percent and 9 percent.

Savings banks jumped in with higher rates than those offered by commercial banks. Rates typically go from 6.5 percent to as high as 19.9 percent. Some savings banks, though, offer loans with lower rates of around 6 percent, such as the one offered by KB’s savings bank and SBI Savings Bank.

The range of rates offered by credit card issuers is much broader. Woori’s credit card company provides a wide variety of unsecured loans with interest as low as 4.9 percent and as high as 24.9 percent. The maximum interest rate that a loan provider can legally set is 27.9 percent.

Still, the government-run siatdol loan program offers even more variety of options.

The Financial Services Commission introduced the program last month in hopes of easing debt burdens on people with midrange credit scores. Nine commercial banks, including KB, Shinhan, Woori, KEB Hana and Nonghyup, as well as some regional banks, are participating in the government-led loan program. Customers can borrow a maximum of 20 million won and pay the principal within five years.

According to the financial regulator, more than 5,700 people have used the loan program offered by banks as of Tuesday, borrowing a total of 60.7 billion won. The average loan size was 10.5 million won, and most borrowers applied for interest rates between 6 and 8 percent.

Customers with credit scores between 4 and 7 out of 10 (with a higher score indicating poorer credit) accounted for 77.5 percent of those who applied for the loan program.

Starting early next month, four regional banks along with savings banks will be offering siatdol loans.

The interest rates provided by the regional banks are expected to be similar to those of commercial banks, between 6 and 12 percent, while savings bank loans are expected to have a higher rate of around 15 percent.

“We expect siatdol loan access for those with midrange credit scores to improve significantly with the participation of regional banks, thanks to their nationwide network,” said Shin Jin-chang, an official in charge of small and midsize finance at the commission.

Shin advises those seeking midrate loans to carefully compare the products available as each financial institution has its own credit evaluation model. Even if a customer’s credit score remains the same, the maximum loan that a person can take out and the interest rate could differ.

In the case of commercial banks, while they may provide lower rates, the maximum loan size is smaller than at savings banks and credit card companies, and their credit evaluation is stricter.

At card companies, the person’s credit card spending plays a significant role in the evaluation process. Even if customers have low credit scores, depending on their spending, the interest rates offered could be lower.

In the case of savings banks, the maximum loan size is much higher on midrate loans, and the maturity on the loan is relatively long compared to commercial banks.

The siatdol loan is a good option for those struggling to secure a loan because it is guaranteed by Seoul Guarantee Insurance.

BY KIM KYOUNG-JIN [lee.hojeong@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)