[Debriefing] Elliott in Korea: the back story

Elliott’s founder Paul Singer [JOONGANG PHOTO]

What is Elliott?

Elliott is a collective term for the New-York based activist hedge fund Elliott Management, its various units around the world and its funds. Elliott Management is one of the biggest hedge funds in the world. It was founded by American Paul Singer in 1977 and now has $34 billion in assets under its management.

Elliott Management runs two flagship funds: Elliott Associates and Elliott International. The former tried in vain to block the controversial merger of Samsung C&T and Cheil Industries in 2015. Elliott Management operates overseas units in London, Hong Kong and Tokyo under the name Elliott Advisors.

An activist hedge fund is a type of an investment company that uses its capital to buy stakes in companies and exercise its power as a shareholder to increase the stock’s value. It is willing and sometimes eager to challenge the management of the company it holds shares in. There are no legal requirements to be called an activist hedge fund, and there is a wide spectrum of activism practiced from igniting a proxy battle, liquidating assets, requesting changes in the board, objecting to mergers or even putting a company up for sale.

Actions by activist funds like Elliott almost always trigger controversy. On one hand, they are seen forcing companies with opaque corporate governance to become transparent. On the other, they can be seen as preying on vulnerable companies for short-term financial gains.

Are they bad guys or good guys? Against the charge of greed, experts point out that exercising a shareholder’s right to maximize its own benefit is at the very core of capitalism. Activism can help bring to light - and fix - the dark side of a corporate structure. This is why The Economist once called activist funds “capitalism’s unlikely heroes.”

Yet when they attack a company’s most vulnerable spot, force it to do their bidding and then sell its stock to take short-term gains, they earn a different sort of nickname: “financial terrorist” or “vulture.”

What is Korea’s experience with activist hedge funds?

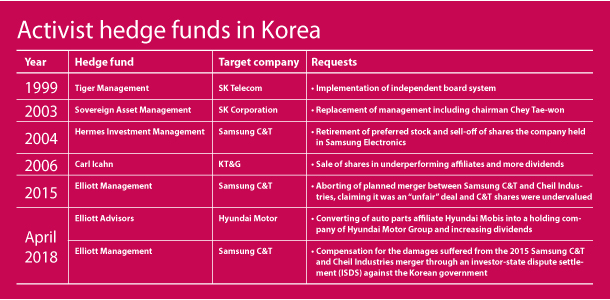

Korea’s experience with foreign activist hedge funds hasn’t been pleasant. Every major intrusion so far by activist hedge funds left the investors with hundreds of billions of won in profit taking - except for Elliott’s objection to the 2015 Samsung group merger. American hedge fund Tiger Management, which purchased a 6.6 percent stake of SK Telecom in 1999, demanded replacement of the management as well as implementation of an independent board system. The following year, it sold its entire stake and made 600 billion won ($ 557 million) in profit. There are many similar cases. In 2003, British activist hedge fund Sovereign Asset Management became the second-biggest shareholder of SK and demanded the ouster of Chairman Chey Tae-won, who was at the time in jail for accounting fraud. Later on, it left Korea with 940 billion won in profit-taking.

No wonder their actions have gained a Korean nickname that translates as “dine and dash.”

Korea’s ambivalent attitude towards foreign investment goes beyond hedge funds. Private equity firm Lone Star made big waves in Korea when it purchased a controlling stake in Korea Exchange Bank for 1.4 trillion won after the Asian financial crisis in 2003, when the domestic economy was highly vulnerable. In 2011, it sold it back to Hana Financial Group for 3.9 trillion won.

Which hedge funds are most involved in Korea?

It is hard to pinpoint which foreign hedge funds have the largest stakes in Korean companies since they tend to keep their holdings confidential. In Korea, if a company holds more than five percent of any publicly-traded stocks, it is required to make the stake public. But foreign hedge funds - especially activist hedge fund operators - typically only go over the 5 percent limit when they are about to make demands on the company. Recently Hong Kong-based activist investor Oasis Management said it is paying attention to Korea because it sees “momentum picking up around corporate governance,” according to Activist Insight, a research firm tracking shareholder activism.

What is Elliott’s newest battle?

Elliott’s latest target is Korea’s biggest automaker, Hyundai Motor, and its many affiliates. Right after the automotive giant announced a long-anticipated plan to overhaul its problematic cross-shareholding governance structure in March, Elliott’s Hong Kong-based unit released a statement saying it holds a $1 billion stake in Hyundai Motor, Kia Motors and Hyundai Mobis and started its tug-of-war with the company. It “welcomed” the company’s proposed plan at first, and then revealed what it really wanted in detail. It demanded the company to change to a holding company structure and increase dividend payments. It also requested the appointment of three independent board members.

How is Hyundai Motor reacting?

Hyundai Motor, which is known as one of the most obstinate corporate cultures in Korea, instantly reacted to Elliott’s surprise announcement by retiring 3 percent of its stock worth $890 million. Cancellation of treasury stock leads to higher shareholder returns. It was an apparent call for a truce or compromise. But Elliott said that was not enough. A few days later, auto parts affiliate Hyundai Mobis - which will act as a de facto holding company of the group if the company’s proposed plan gets approval in May - also announced a plan to retire treasury stock worth $557 million. Both companies deny their shareholder-friendly actions are related to Elliott’s demands. Elliott’s pressure is likely to continue until the general shareholder’s meeting scheduled for May 29 that will decide the fate of Hyundai Motor’s proposed restructuring.

Isn’t Elliott involved in other legal issues in Korea?

Elliott recently initiated a legal dispute with the government saying the Park Geun-hye government enabled the merger between Samsung C&T - Elliott had a 7.12 percent stake in 2015 - and Cheil Industries. The fund sent a notice in mid-April to the Justice Ministry to file an investor-state dispute settlement. With the implementation of the free trade agreement with the United States, U.S. investors have the right to use an international tribunal to resolve investment disputes.

Does it have a case?

In 2015, Elliott made a surprise announcement that it had a sizable stake in Samsung C&T and demanded that Samsung stop the merger with Cheil Industries. Elliott claimed that the merger undervalued Samsung C&T’s stock value and called it a scheme to strengthen Samsung heir Lee Jae-yong’s influence over affiliates. But a majority of shareholders including Samsung C&T’s largest, the National Pension Service (NPS), approved the merger. That merger came into the spotlight again recently after the impeachment and removal of former President Park. Several court rulings have held that Park elicited a bribe from Samsung in exchange for pressuring the NPS to approve the merger.

One court didn’t specifically recognize a bribery charge against Samsung over the merger. But another court convicted those in charge of approving the merger at the NPS and the Ministry of Health and Welfare with abuse of power.

BY JIN EUN-SOO, PARK EUN-JEE, AND ANTHONY SPAETH [jin.eunsoo@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)