Household loan limit scheme delayed by two months

![A notice regarding home mortgage loans is posted at a bank in downtown Seoul. [NEWS1]](https://koreajoongangdaily.joins.com/data/photo/2024/06/28/18a7e3ac-c95b-48ca-a0c9-e8df047d0e89.jpg)

A notice regarding home mortgage loans is posted at a bank in downtown Seoul. [NEWS1]

The scheduled tightening of household loan limits has been postponed by two months to September.

The decision, announced by the Financial Services Commission (FSC) this week, came amid lingering concerns of a sluggish economic rebound and a potential liquidity crunch from project financing loans in the real estate sector.

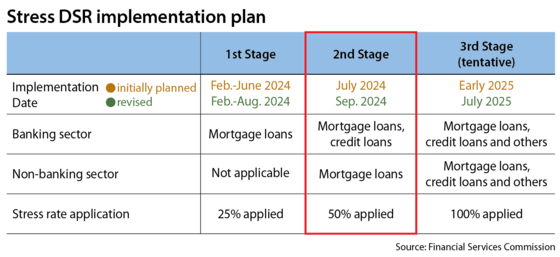

Upon the delay, the second-phase implementation of the so-called stressed debt service ratio (DSR) was moved from July 1 to September 1.

The stressed DSR scheme was designed to reduce loan limits by adding a hypothetical spread when calculating these limits in consideration of potential future rate hikes.

The goal is to adjust loan limits based on expected hikes, considering the potential increase in repayments on floating-rate loans during rate hike cycles. The spread is applied only for calculating loan limits and is not included in the actual interest rate.

"The application of the second-phase stressed DSR on mortgage loans issued by non-bank lenders is estimated to affect about 15 percent of borrowers, resulting in lower loan limits for them," said an FSC official.

"We decided to postpone the implementation considering the ongoing talks on comprehensive government support measures for the self-employed and the upcoming feasibility assessments on real estate projects starting this month."

The stressed rate is capped between 1.5 percent and 3 percent, and is updated every six months.

The government decided to gradually raise the stressed DSR in three phases — 25 percent of the set rate under the first phase, 50 percent under the second phase and 100 percent under the third phase — to minimize the market impact this year, which is the first year of its implementation.

The first-phase stressed DSR took effect in February, with the stressed rate currently standing at 0.38 percent.

Should the second phase be implemented, mortgage loan limits will decrease significantly.

For example, if an individual who is earning an annual salary of 50 million won ($35,995) takes out a 40-year mortgage with a 4 percent interest rate, the person can borrow up to 398.8 million won under the existing DSR of 40 percent.

With the first-phase stressed DSR scheme applying an additional 0.38 percentage points, the person’s loan limit decreases 21.8 million won to 377 million won.

Under the second phase, the stressed rate rises to 0.75 percentage points from 0.38, further reducing the loan limit by another 20 million won.

By the third phase, with a 100 percent stressed rate, the loan limit could decrease by nearly 100 million won.

The second phase will also expand the scope of loans and lenders subject to the program, as the first phase applied only to mortgages from commercial banks. Under the second phase, the program will extend to mortgages and unsecured loans of over 100 million won from banks, as well as mortgages from non-banking financial institutions.

The third phase, which is expected to begin by mid-next year, will apply to all loans from both banks and non-bank lenders.

"With the second phase of the stressed DSR, mortgage loans from banks and non-bank lenders are expected to see a 3 to 9 percent decrease in the limit depending on the loan type, while credit loans will see a 1 to 2 percent reduction depending on the interest rate type and maturity," according to the FSC.

"The proportion of high-DSR borrowers whose loan limits are expected to be constrained by the stressed DSR is estimated to be around 7 to 8 percent."

However, concerns have been raised that the sudden delay in the second-phase implementation could send the wrong signal to the market, as household loans — particularly mortgages — are on the rise. The delay may nudge borrowers to rush for more loans, experts pointed out.

"Delaying the implementation this way can erode market trust and send a misleading signal that loan limits will eventually not be restricted," said Seok Byoung-hoon, economics professor at Ewha Womans University.

BY KIM NAM-JUN, CHOI HAE-JIN [choi.haeijn@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)