No dilly-dallying

The author is chief editor of content production at the JoongAng Ilbo.

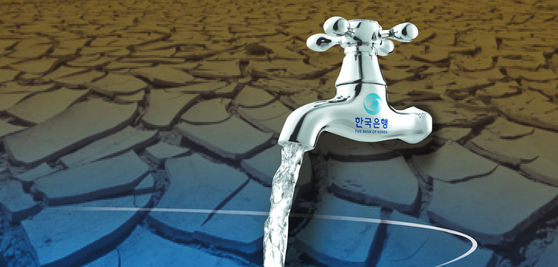

The Bank of Korea (BOK) last week stunned the market with its rate action. It had slashed the policy rate by 50 basis points to a fresh historic low of 0.75 percent in an emergency meeting in March. Since the cut was bigger than the usual 25 basis points, many had expected the central bank to sit out in May.

But the BOK took preemptive action to push the rate to a new low. It did not stop there. It vowed more aggressive bond purchases, or quantitative easing permissible within the law. We had not expected that quantitative easing common in advanced markets like the United States and Japan would arrive in Korea so soon.

On the same day, it announced another extraordinary move, lowering Korea’s growth estimate for this year. It axed its growth estimate for 2020 from the previous 2.1 percent to negative 0.2 percent. It warned that if coronavirus risks persist into the second half, the contraction could be as deep as 1.8 percent. It is rare for the Korean central bank to release the worst-case scenario for the economy.

The central bank is known to be frustratingly prudent and often slow in responding to economic developments. Even after the outbreak of a global financial meltdown in 2008, the central bank moved beyond baby-step cuts only after pressure from the Blue House, and slashed the benchmark rate by a full 1.00 percentage point. As the BOK usually moved in line with the government guidelines in monetary policy, it was said to have become a division of the finance ministry.

The economic fallout from Covid-19 precipitated a transformation in the central bank. It has had past experiences with the crises in 1997-1998 and 2008-2009. It learned that dilly-dallying in policy action only exacerbated the uncertainty during economic turmoil. Bank of Korea Governor Lee Ju-yeol vowed an aggressive response to the pandemic to defend the economy from the early stages of the epidemic.

Compared to central banks in major economies, the central bank’s move could still seem conservative. But it is venturing into uncharted waters to help the government overcome the ramifications of the outbreak. We can draw some lessons from its actions for tackling the challenges of Covid-19 more generally.

First, we must break out of past rules and customs and employ all possible means. We must try everything except for those that cannot be done. In the past, the central bank would not have agreed to supplying funds to financial institutions beyond primary banks. But since March it has offered to provide unlimited liquidity to non-banking financial institutions with their treasury holdings as collateral.

The central bank even changed its loan rules. If rules cannot be broken, they should be fixed in emergency times. The central bank expanded its bond purchase program to beyond treasuries or semi-government bonds to include corporate bonds and commercial paper. It will back the government and state lender Korea Development in the launch of a bond stabilization fund designed to buy corporate bonds and ease the liquidity crises due to business setbacks from the pandemic. It has benchmarked the U.S. Federal Reserve, which set up a special purpose vehicle to absorb corporate bonds. The move is aimed to take risks to save companies against the virus storm.

Second, the central bank has become more communicative with the market and public. It frankly warned of negative growth that could be as bad as 1.8 percent. It chose to raise a solemn alarm instead of sounding unnecessarily sanguine. Under negative 0.2 percent growth, new jobs would only total 30,000.

If growth stumbles further, a job increase could be impossible. People can ready themselves if they are alerted about the arrival of a tsunami. A warning of a job cliff can result in more pain-sharing actions by the society. Politicians agreed that there was no time to waste.

Covid-19 poses unprecedented challenges, demanding unprecedented reactions. The government’s snowballing spending plans have been condoned due to the emergency in spite of the massive dent in the fiscal account. But strangely, the government has left some of the areas that require the most urgent fix.

The Bank of Korea (BOK) last week stunned the market with its rate action. It had slashed the policy rate by 50 basis points to a fresh historic low of 0.75 percent in an emergency meeting in March. Since the cut was bigger than the usual 25 basis points, many had expected the central bank to sit out in May. It has not taken action to freeze the minimum wage, expand flextime or lift regulations on industrial investment around the capital. The government and ruling party have not moved beyond their bias, whereas the central bank has.

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)