Defaults, foreclosures and bankruptcies surge amid Korea's perfect economic storm

Published: 29 Jan. 2024, 18:37

Updated: 30 Jan. 2024, 11:45

-

- SHIN HA-NEE

- shin.hanee@joongang.co.kr

![A pedestrian looks at apartment buildings from Mount Namsan in central Seoul on Sunday. [NEWS1]](https://koreajoongangdaily.joins.com/data/photo/2024/01/30/899383ea-a598-4fe5-95a3-cdcf0e298dd6.jpg)

A pedestrian looks at apartment buildings from Mount Namsan in central Seoul on Sunday. [NEWS1]

High interest rates are squeezing Korea’s economy across the board, with the default rates for commercial papers surging as well as the number of foreclosure filings rising in the country.

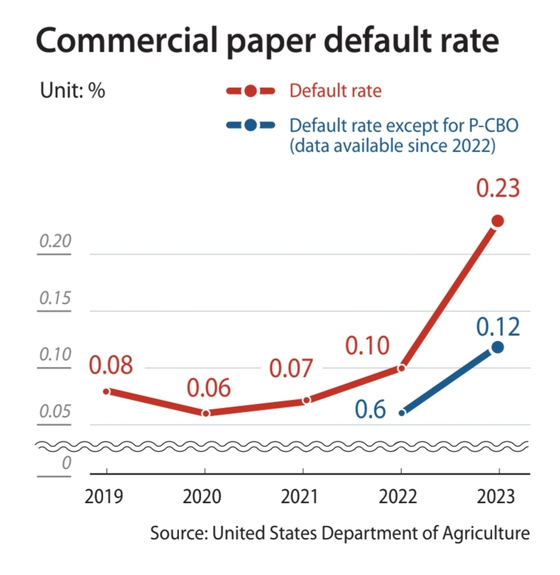

The default rate of commercial papers in Korea came in at 0.23 percent last year, according to the Bank of Korea’s Economic Statistics System, a record since 2001’s 0.38 percent.

The figure has been on a steep rise over in recent years, from 2021’s 0.07 percent to 2022’s 0.1 percent.

The combined value of defaulted commercial papers also doubled to 5.35 trillion won ($4 billion), up 137 percent on year, breaking a nine-year record.

The Bank of Korea cited the increase in “technical defaults” of Korea Credit Guarantee Fund’s Primary collateralized bond obligation (P-CBO) — designed to help companies with low credit ratings raise funds more easily — as, according to the central bank, there has been an increase in the cases of nonpayment of loans caused by technical issues such as partial repayment or inconsistency in the issuance date and the maturity rather than the debtor’s inability to repay the loan.

With the P-CBOs excluded, the default rate stood at 0.13 percent, double the 0.06 percent in the previous year, and similar to the average level through the 2010s.

The steep rate hikes, as well as the general slowdown in the economy, seemed to have taken a toll on the companies. The delinquency rate for commercial loans issued by banks stood at 0.6 percent as of November last year, compared to the previous year’s 0.3 percent.

The interest coverage ratio — a debt and profitability ratio that indicates a company’s ability to repay outstanding debts — plunged in the first half of last year from 2022’s 5.1 to 1.2.

Small- and medium-sized enterprises (SMEs) took the hit harder during the same period, with the interest coverage ratio collapsing from 2 to 0.2. The latest figure, 0.2, means that the companies’ interest expenses are five times their operating incomes.

Bankruptcy is soaring as well. The number of corporate bankruptcy filings last year reached 1,657, up 65 percent on year.

The economic slowdown also had an impact on the property market, with the number of real estate assets repossessed and put up for auctions jumping 61 percent on year to 105,614, according to the Supreme Court of Korea’s data. It marked the highest number since 2014.

Meanwhile, loans from project financing are adding uncertainties in the financial market, with second-tier non-bank lenders and securities firms in particular exposed to the possible risks of a liquidity crunch.

As of September last year, out of 134.3 trillion won of outstanding loan balance in the real estate industry funneled through project financing, bridge loans amounted to 30 trillion won. Bridge loans, issued mostly by second-tier lenders, are hard to repay if the construction does not begin.

High-risk real estate debt-to-equity ratios for major financial firms with a capital of over 3 trillion won stood at 29.2 percent, according to Korea Investors Service, but the figure was 43.3 percent for mid-sized firms with a capital of 1 to 3 trillion won, and 34 percent for smaller companies with less than 1 trillion won in capital.

Many of such loans from project financing are set to reach maturity this year. Korea Ratings expects that financial firms may lose up to 2.8 trillion won due to project loans by this June.

“If a securities company fails to mitigate the risks and raises uncertainties in the market, we will hold such a company and its management accountable in a strict and reasonable manner,” said Financial Supervisory Service Gov. Lee Bok-hyun on Jan. 24.

BY JEONG JONG-HOON, KIM NAM-JUN AND SHIN HA-NEE [shin.hanee@joongang.co.kr]

with the Korea JoongAng Daily

To write comments, please log in to one of the accounts.

Standards Board Policy (0/250자)